Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineCan gold miners help to dig income seekers out of a hole?

Whatever investors think of the quality and accuracy of the data coming out of China, on either the extent of the Covid-19 outbreak or the economy, they may be intrigued to note how the country is behaving, as that is much harder to obfuscate.

Zijin Mining acquired Canada’s Continental Gold for C$1.4bn in cash in March and last week Shandong Gold agreed to acquire junior Canadian gold digger TMAC Resources for $149m.

At a time when gold prices are holding firm at around $1,700 an ounce, this is intriguing, especially as leading Western precious metal miners had already begun to jockey to position and snap up assets which they clearly felt offered value.

Canadian firms Endeavour Mining and Silvercorp Metals swooped for Semafo and Guyana Goldfields respectively back in spring – the former having been rebuffed in its efforts to snap up FTSE 250 constituent Centamin (CEY) – while 2019 saw the consummation of two huge deals, as Barrick Gold merged with Randgold Resources and Newmont Mining bought Goldcorp.

Investors could just dismiss this as necessary consolidation within an industry that failed to shine from an investment perspective for much of the last decade. But they could take note and at least ask themselves why gold executives in both the West and China are moving to acquire assets in such a hurry.

Bubbling up

Governments and central banks, already running lofty deficits or swollen balance sheets, are going ‘all in’ as they try to keep economies going during the lockdowns that are being imposed as part of the fight against the viral outbreak. The US Federal Reserve’s balance sheet has grown by $2.5trn, or 62%, since February while the US Government has begun to talk of adding to the $3trn in fiscal stimulus already provided.

On this side of the pond, the UK Government’s discussion about phasing out the payment scheme for those unlucky enough to be furloughed is already encountering pushback from unions and those who are concerned about going back to work.

That is perfectly understandable on safety grounds. It is also easy to understand in the context of Ronald Reagan’s maxim that ‘nothing lasts longer than a temporary government programme’. The Government now has a tricky balancing act between providing consumers with support when it is needed and weaning the nation off helicopter money – the longer that money is supplied, the greater the pressure will be to keep on creating it out of thin air.

Governments and central banks had not got around to withdrawing the stimulus doled out in the wake of the financial crisis a decade ago before they had to start reapplying it. The chances of this latest round of fiscal and monetary largesse being sterilised feel slim, even once the viral outbreak is finally contained.

This could be one reason why the gold price is holding firm within touching distance of its 2011 all-time high of $1,900 an ounce.

Flowing freely

Strength in the gold price is bringing benefits to those firms who explore and drill for the stuff. In its first-quarter results last week (5 May), Newmont Mining revealed a 43% year-on-year increase in sales, a 59% increase in operating profit and a three-fold increase in free cash flow (after interest, tax, working capital and capital spending) as higher gold prices supplemented increased metal production.

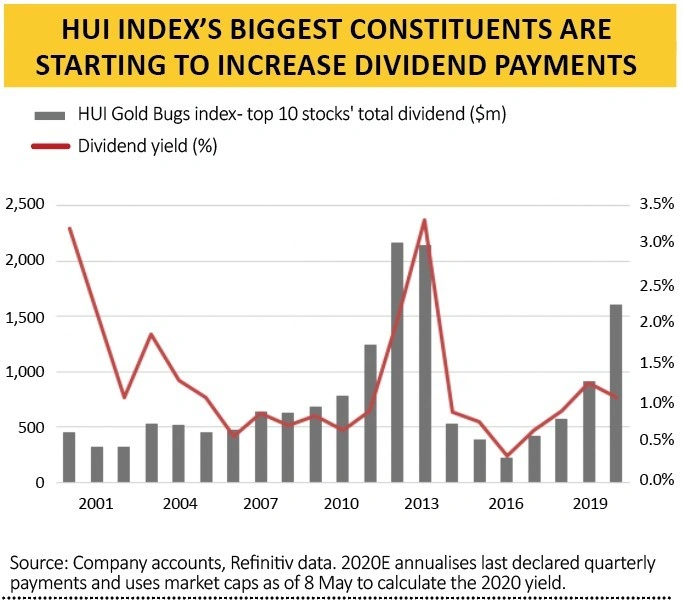

This continued a pattern across the 10 biggest members by weighting in the NYSE HUI Gold Bugs index. Since 2015, when gold bottomed at barely $1,050 an ounce and miners were writing down the value of their assets, aggregate annual free cash flow has surged from $341m to $5.6bn.

Better still, that surge in free cash flow – after taxes, interest, working capital and capital expenditure needs had all been met – prompted a 78% increase in Newmont’s quarterly dividend to $0.25 a share.

At a time when over 40 FTSE 100 firms have cut, cancelled or deferred their dividends, this may catch the eye of income-seekers. The bad news is that the aggregate dividend yield across the 10 biggest members of the HUI index was only 1.1% in 2019.

The good news is that 2019’s aggregate payments were less than half of 2012’s peak and if gold stays firm or goes higher still that latter sum could be soon within reach, given that the production weighted all-in sustained cost (AISC) of production across those 10 names was $949 last year.

Any further surge in gold prices thanks to money creation or deficit accumulation could turn gold miners into cash machines and the source of income that many investors crave.

Equally, if Covid-19 can be contained (and then eradicated) quickly and the global economy starts to rebound sharply, investors may not need gold’s perceived defensive qualities and any drop in the metal’s price would erode miners’ cash flow and ability to pay dividends.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Exchange-Traded Funds

Feature

First-time Investor

Great Ideas

- Genus remains well positioned for further growth

- Civitas targets above-inflation dividend growth

- More reasons to be positive on ITV as viewing figures rise

- Buy this ETF to profit from the healthcare revolution

- Boris’ return to work by car message could boost shares in Motorpoint

- Ocado shares hit another new all-time high on surging grocery sales