Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineSeven stocks for life after coronavirus

There are flickers of light at the end of a very long tunnel. Doctors are learning more about Covid-19 every day; how it spreads, which treatments are showing promise, and how to create effective testing methods.

Inevitably, after being cooped up during many weeks of lockdown, restrictions are slowly being lifted and consumers and businesses are focusing on how they can transition back to normality.

The issue for investors is what the ‘new normal’ life will look like. In this article we consider how some of the key sectors will cope. We also pick seven stocks which could do well in the coming months and years.

POST-CRISIS WINNERS

Stock markets around the world have been staging a comeback in the past month as investors become more optimistic about lockdowns ending, businesses and schools reopening, and severe economic damage being short-lived.

There is a feeling that markets might have been over-optimistic given that a lot of stocks have recovered quite a bit of the losses from the initial sell-off, yet we are still facing economic disruption potentially well into 2021 or even lasting into 2022.

We believe it is better to focus on companies that stand a better chance of surviving a long period of working and living adjustments post-crisis rather than trying to pick any company whose shares might look like they’ve been oversold.

That means prioritising companies which have the ability to keep functioning under social distancing measures and for whom the crisis makes it more likely that people will use their products and services beyond the current lockdown.

THE RISE OF REMOTE WORKING

There is general agreement that the workday patterns, habits and IT systems for remote working established during this lockdown period are unlikely to disappear.

For example, in 2018 it was reported that more than half (56%, according to OWL Labs) of the companies in the world allowed remote working.

‘This figure is now going to be significantly higher as working remotely becomes increasingly the “new normal” in many sectors across the globe,’ says Nigel Green, chief executive of financial adviser deVere.

While we may miss some of the personal interface, many workers, particularly those of us previously office-based, have proved we can be just as efficient and productive working from our homes, with less time wasted and non-essential demands easier to brush aside.

Cutting our carbon footprint from the daily commute and better work/life balance are bonus byproducts of this fairly simple change to our working arrangements.

As a consequence, we would anticipate the world’s leading technology companies to continue to dominate investor returns.

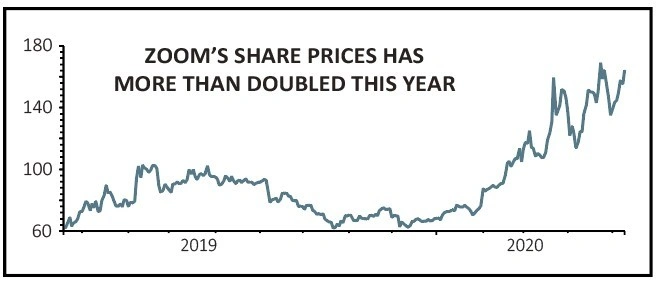

Online communication and collaboration platforms, such as Microsoft Teams, Zoom and others, have become new corporate forums rather than face-to-face meetings or phone calls used previously. The downside of this clear demand hike is that investors will have to pay a premium to own shares in the relevant companies.

‘There are several smaller companies in this space which have already performed well and trade on lofty multiples,’ says Sharon Bentley-Hamlyn, investment manager at Aubrey Capital.

Bentley-Hamlyn highlights Belgium’s Euronext-listed Barco, with its Clickshare product for wireless video conferencing. ‘There will be strong demand in the corporate sector and from universities, who can link over 80 students remotely by video for teaching purposes using Barco’s product, a real benefit when so many universities have had to close their doors.’

This chimes with the positive backcloth for the wider online learning industry, where the UK’s Learning Technologies (LTG:AIM) has been growing rapidly in recent years.

‘Despite likely macro headwinds in the short-run from Covid-19, in the long-term the crisis will only escalate the importance of digital learning solutions for enterprises of all sizes,’ says Patrick Stewart of research group Megabuyte.

‘If the move to remote working was ongoing, the recent scramble to facilitate a fully remote workforce means that companies, on the whole, are now much better placed to support a higher level of remote working,’ Stewart says. ‘As the cost benefits and limited fall in productivity start to be recognised, we expect the remote working trend to accelerate.’

IT services companies that implement this sort of capability will have a tailwind for some time to come, believes Aubrey Capital’s Bentley-Hamlyn.

Digital transformation firm NetCompany recently told the investment manager that long term it will see ‘a big splash’ on new projects as people will see the importance of having devolved infrastructure.

This should mean a golden era for IT specialists capable of acting as a trusted technology partner to organisations, providing vital skills, apps and advice to enable this shift and make it work, such as Computacenter (CCC), Softcat (SCT), Kainos (KNOS) and many others.

THE FURTHER RISE OF ONLINE SHOPPING

Over the coming years, we would expect the landscape of the global economy to change significantly because of major structural changes that were already underway before the coronavirus crisis.

For example, online shopping, or digital commerce, was already booming long before any of us had heard of coronavirus and the crisis will only speed up that switch from stores to clicks.

The lockdown will have encouraged more people to try online shopping and/or become more dependent on it. Just look at how supermarkets have been swamped with demand for their online services – doing the big weekly shop via the internet could become the new norm.

Investors can look at the digital commerce area from many different angles. You can consider a range of retail and electronic payments giants like Amazon, Alibaba, Ebay, Shopify, Visa, MasterCard and PayPal.

You also have fast-growing online retailers such as Boohoo (BOO:AIM) and Ocado (OCDO), the latter playing a dual role in selling groceries online and also providing the systems to help third parties fulfil online food and drink orders.

Despite the world shifting towards the online channel, there are negatives to consider with the internet space short-term. One is the ability for consumers to be able to afford to keep shopping at the same level as before.

Just look at Boohoo whose shares have hit a new all-time high. This seems perplexing given that its target market is likely to experience a surge in unemployment and restrictions on the leisure sector would suggest there is reduced demand for new clothes as we aren’t going nightclubbing or out for a meal with a large group friends, certainly not for some time.

ABLE TO ADAPT TO SOCIAL DISTANCING

As a shorter-term focus, investors would be wise to consider how certain shops might be able to function while lockdown restrictions are still in place.

Some retail chains benefit from having large stores which will make it a lot easier to keep up social distancing measures as there is space to move around or the ability to rework the store layout.

DIY chains like Wickes – owned by Travis Perkins (TPK) – generally have large sized stores and they should see sustained demand going into 2021. The more time spent at home, either through lockdown measures or ongoing remote working, will focus a person’s attention more on their immediate surroundings and perhaps encourage them to make the home look nicer.

SECTORS IN TROUBLE

There are quite a few sectors facing a monumental battle to stay alive, including airlines, hotels and retailers with physical stores.

The airline sector is very high risk from an investment perspective at the moment as companies are burning through cash while their planes are grounded. Hotels are seeing a very large drop in demand and this situation is unlikely to change in the near-term.

Longer-term, oil prices could start to pick up as companies around the world get back to work, although they are unlikely to hit pre-crisis levels for a long time, if at all.

The commercial property sector looks very vulnerable if the remote working trend is sticky post-lockdown. Companies may realise they don’t need as many offices as before, thus leading to a big drop in demand for commercial real estate.

We plan to look at all of these vulnerable sectors in more detail in the coming weeks in Shares.

SEVEN STOCKS TO BUY AS WINNERS IN THE POST- CORONAVIRUS WORLD

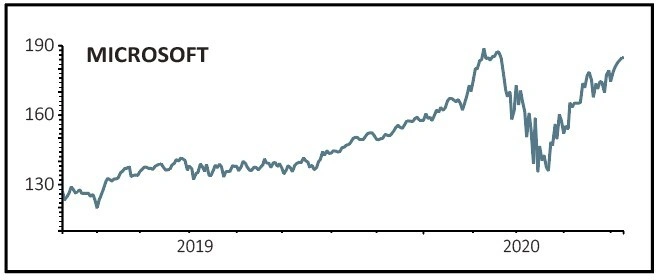

MICROSOFT (MSFT:NDQ) $184.68

The tech giant should have thrived through the crisis and its products and services are likely to remain in demand for years to come.

Its sources of income can be split into as many as nine categories, with roughly three overarching segments: productivity and business processes (Microsoft Office, Dynamics, LinkedIn), personal computing (Windows, Xbox) and the cloud (Azure, SQL).

Some of these divisions could be affected by big increases in unemployment, which are already becoming visible particularly in the US, with potentially lower Microsoft Office subscriptions (which had been growing strongly), fewer PC sales and reduced advertising spend on LinkedIn, for example.

But the significant increase in companies telling staff to work from home will require equally significant investment in exactly the solutions that Microsoft provides, such as its Teams communications platform.

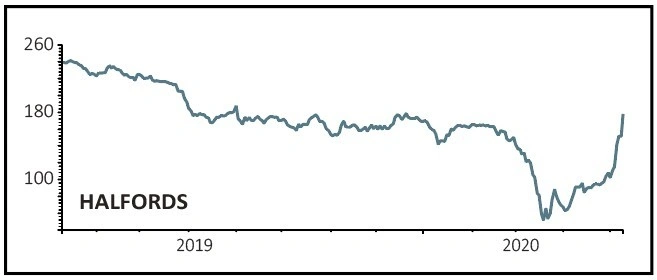

HALFORDS (HFD) 181.4p

The UK Government has designated bicycle and car maintenance company Halfords (HFD) as an essential services provider. Consequently, Halfords has kept open 325 retail stores on a ‘dark basis’ serving customers from the front of stores to ensure the safety of its staff.

Business has been brisk since lockdown as more customers have taken the opportunity to include cycling as part of their daily exercise as roads have become quieter and safer to ride. It was also given impetus by the Government’s ‘cycle to work’ initiative to encourage cycling as a means of commuting.

Advice by Boris Johnson on 10 May to avoid public transport will only fuel more demand for bikes and push more business to Halfords, given it is one of the country’s biggest sellers of two-wheeled pedal power.

In a recent trading update the company upgraded its expectations for pre-tax profit for the year to 29 March 2020 to be at the higher end of the previously guided £50m to £55m range.

Halfords is also well-placed to benefit from growth in electric bikes. These are likely to be in greater demand if more people choose cycling as an alternative way to commute than public transport post-lockdown. It offers some of the best value e-bikes on the market and is a natural place for people to shop.

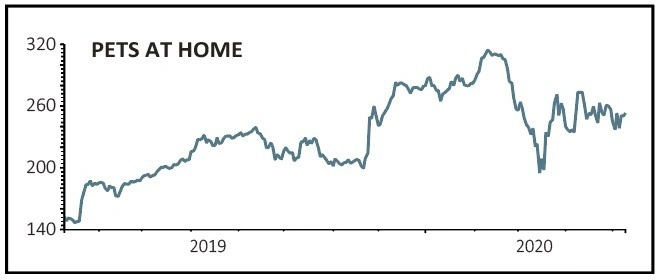

PETS AT HOME (PETS) 234.6p

Throughout the Covid-19 crisis and associated lockdown, the companionship provided by our furry friends has buoyed the spirits of many families and isolated individuals.

People increasingly treat feline and canine companions as one of the family, and they are prepared to spend big on their pets’ health and wellbeing. This ‘humanisation’ trend will play to the strengths of Pets at Home (PETS) even after the pandemic has passed.

The UK’s leading pet care business has been designated an essential retailer by the Government, as the pet products it sells, the in-store advice it provides and health care services it offers are deemed essential at a time when pets are playing an increasingly vital role in our daily lives.

One of a rare breed of retailers with positive momentum at their heels, Pets at Home should continue to see robust bumper demand, particularly online, as channel shift accelerates and animal lovers log on to order pet supply deliveries.

RECKITT BENCKISER (RB.) £70.04

While Reckitt Benckiser (RB.) is known globally for its household cleaning products, such as Cilit Bang, the pandemic has seen demand soar for its other big home hygiene brands, like Harpic and Lysol and for its disinfectant Dettol.

Sales in the first quarter when, barring China, most of the world had yet to feel the devastating impact of the virus and government lockdowns, grew 13% as customers stockpiled Dettol and other cleaning products.

Over-the-counter medicines, such as Mucinex and Nurofen, saw sales jump 33% while revenue from other health products rose 17%, helped by demand for vitamin and mineral supplements. As a dedicated health and home hygiene company, with sales last year of £12.8bn across North and South America, Europe, Africa and Asia, Reckitt is well placed to help millions of people cope with the challenges of life both during and after the pandemic.

SCOTTISH MORTGAGE (SMT) 683.5p

Widely seen as manager Baillie Gifford’s flagship investment trust, Scottish Mortgage (SMT) is a way for investors to get in on the world’s most exciting growth companies.

By having stakes in lots of different businesses, Scottish Mortgage is able to provide access to many big themes for the future including video conferencing (Zoom), online shopping and cloud services (Amazon and Google-parent Alphabet), advanced healthcare and the development of vaccines and treatments for infectious disease (Illumina and Vir Biotechnology), and complex microchips (ASML).

Scottish Mortgage is best suited to patient investors who are prepared to hold its shares for a long time.

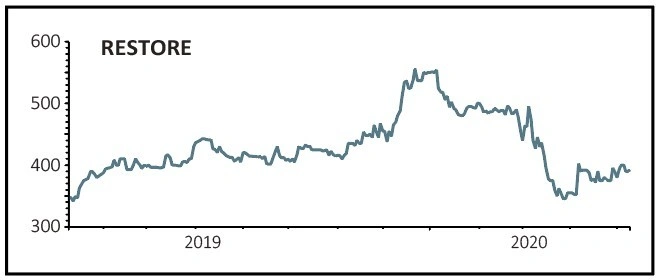

RESTORE (RST:AIM)

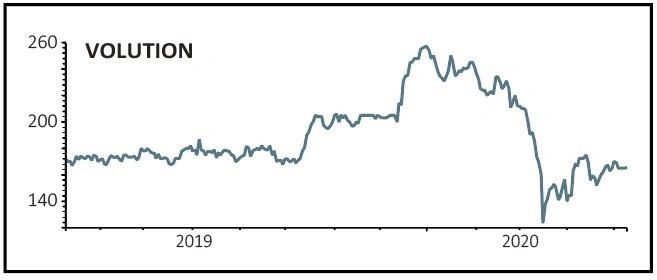

Both Restore and Volution are our ‘wild card’ picks – namely stocks that have the right ingredients to thrive post-crisis, but where there is scope for possible disappoints if our investment thesis doesn’t play out as expected. As such, treat these as higher-risk investment ideas.

Restore (RST:AIM) is the UK market leader in document management and business relocation, as well as being a leading player in other essential services like digital storage, secure data destruction and technology installation.

Revenue last year was £215m, an increase of 10%, while the markets it operates in turned over £1.8bn with growth of between 1% and 5%, meaning Restore is quickly gaining market share.

Its customer base includes public sector organisations like the NHS, central and local government, and blue-chips who need large-scale document storage and data destruction.

The document storage side should be very resilient. We think the removals bit of the business could benefit longer term if companies reduce their office numbers as a result of more home-working, as Restore would be busy helping them to downsize. However, there is a risk that this sales catalyst might not emerge for a while as companies would still have lease agreements to fulfil.

VOLUTION (FAN) 166p

Crawley-headquartered Volution (FAN) designs, assembles and markets ventilation fans, systems and ducting for domestic and commercial buildings. It has leading market positions in the UK, Scandinavia, Germany and now New Zealand. A greater focus on air quality in the wake of the current pandemic, driven both by customer priorities and regulation, should give earnings a boost in a post-coronavirus world.

In the short term the company is being hit by a drop in construction activity but as of 31 March the company had gross cash of £41m and £14m undrawn in a lending facility, with the suspension of dividends giving the business some breathing space. Based on recently reduced forecasts from Canaccord Genuity the shares trade on a 2021 price-to-earnings ratio of 12.3 times, falling to 10.3 times in 2022. The stock looks good value; the only major uncertainty is the pace of new activity.

DISCLAIMER: Steven Frazer owns shares in Scottish Mortgage

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Exchange-Traded Funds

Feature

First-time Investor

Great Ideas

- Genus remains well positioned for further growth

- Civitas targets above-inflation dividend growth

- More reasons to be positive on ITV as viewing figures rise

- Buy this ETF to profit from the healthcare revolution

- Boris’ return to work by car message could boost shares in Motorpoint

- Ocado shares hit another new all-time high on surging grocery sales