Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineHow to choose the right investment fund for you

In this latest entry to our first-time investor series we focus on investment funds called unit trusts and open-ended investment companies (OEICs) and explain how a novice investor can kick-start the fund selection process.

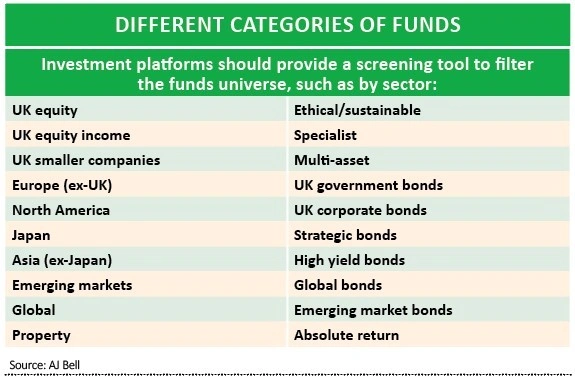

Thousands of funds are marketed to the investing public, providing professionally-managed access to a wide variety of asset classes ranging from equities and bonds to property and commodities. These collectives can give you exposure to many geographic regions and investment styles ranging from growth and value to income.

TAKING YOUR FIRST STEPS

Funds are useful to someone with limited experience of investing because they enable you to entrust the day-to-day investment decisions to a professional money manager.

But before you set out on your fund selection journey, you should ask yourself what it is you want your fund portfolio to achieve? What is your risk appetite and what type of asset exposure do you want? Also, you need to formulate an investment timeframe. These are all important questions for the investment novice to ponder.

One baby step for a first-timer seeking asset diversification is to put money to work with a multi-asset fund – an example is Fidelity Multi-Asset Balanced Income (BJ4L7W2) – which will provide you with a ‘one-stop shop’ solution at a stroke.

These types of funds own shares and bonds, and often give you additional access to property and commodities. They usually avoid ownership of any high-octane assets that could suddenly blow a hole in performance.

As your confidence builds, you could also consider investing in a global fund. These provide access to the acumen of a top money manager and can give you exposure to some of the highest-quality companies from around the world. One example is Fundsmith Equity (B41YBW7), the Terry Smith-steered fund that has proved a consistent outperformer.

Anyone looking to generate an income from their investments should look at equity income funds or bond funds. The former invest in a range of dividend-paying companies and examples of funds in the category include TB Evenlode Global Income (BF1QMV6) and Trojan Global Income (BD82KP3).

KEEPING TRACK OF PERFORMANCE

As the marketing disclaimer so often warns, past performance is no guide to future returns. Novice investors need to heed this advice, as the funds industry has been hit by various ‘star fund managers’ disappointing in recent memory, notably the now-discredited Neil Woodford.

That being said, those funds and managers that do consistently outperform the market and their peers must be doing something right and merit strong consideration for portfolio inclusion.

A good place to start for the novice might be to screen for funds that have delivered ‘top quartile’ performance over one, two, three, five and 10 year time periods, which suggests they have generated healthy returns through both buoyant and depressed economic conditions and in an up and down market.

Very useful sources of performance data include websites such as Trustnet, which is powered by FE fundinfo, and Morningstar. These informative websites allow you to rank funds by sector and performance and can provide a compass for a novice investor bamboozled by the array of funds on offer.

CHOOSING UNIT TYPES

Another thing to consider is fund share class, as picking the right and wrong one can make a significant difference to your portfolio.

The first-time investor will be faced with a confusing array of letters or acronyms after a fund name, which can look like alphabet soup. These make a big difference to how much you will be charged, whether income is paid out or reinvested, and what currency the fund is in.

Watch out for the acronyms ‘inc’ or ‘acc’ after the fund’s name; these simply denote the different classes of funds. So an ‘inc’ or ‘income’ class pays out dividends directly into your investment account as cash, whereas an ‘acc’ or ‘accumulation’ class rolls up dividends and other forms of income and puts them back into your fund with the effect of increasing the value of each unit or share held.

With the accumulation unit, the first-time investor can benefit from compounding of returns (that’s assuming the fund increases in value). This means that the income generated is used to buy additional units of the fund, which then (hopefully) grow and generate more income for the novice investor.

Other things to watch out for are institutional and retail share classes sometimes denoted with I and R after the fund name.

These may come with different charges or minimum investment thresholds, although if you are investing through an investment platform, which will be the case for most people, things will typically be made more straightforward for you.

Many platforms also have lists of top funds to help you narrow down your choice.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Exchange-Traded Funds

Feature

First-time Investor

Great Ideas

- Genus remains well positioned for further growth

- Civitas targets above-inflation dividend growth

- More reasons to be positive on ITV as viewing figures rise

- Buy this ETF to profit from the healthcare revolution

- Boris’ return to work by car message could boost shares in Motorpoint

- Ocado shares hit another new all-time high on surging grocery sales