Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineRare chance to buy Shell cheaply and get 11% yield

While this isn’t a trade for the faint-hearted we think the weakness in Royal Dutch Shell (RDSB) following the oil price crash looks overdone and represents a compelling buying opportunity.

As we write, and based on consensus forecasts for 2020, Shell offers an 11% dividend yield. A yield of 7% or more is often seen as a signal that a payout will be slashed but reassuringly Shell has not cut its dividend since the Second World War and we believe this status will be preserved.

For the foreseeable future the company should have the capacity to ride out oil price volatility either by taking on more debt or resorting to scrip dividends as it did in the wake of the 2014-2016 oil crash, giving investors the option of receiving dividends in new shares instead of cash. Having spoken to Shell’s investor relations team UBS analysts believe ‘Shell can and will defend its dividend through this period of cyclical weakness’. They add that avoiding a scrip dividend would be ‘an important input into the quality of the payout’.

The company’s other actions in the wake of the previous oil downturn, namely reducing spending and increasing efficiency, arguably make it better placed to weather the current storm.

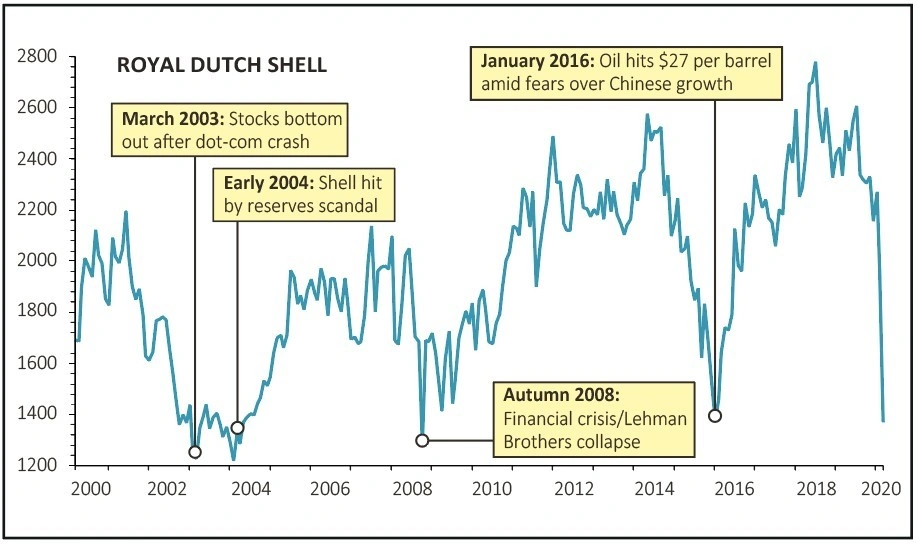

In the immediate aftermath of this latest oil price slump, triggered by Saudi Arabia’s market share grab, Shell’s shares hit £12.4. Looking back over the last 20 years the stock has only traded at these sorts of levels on a handful of occasions.

This includes in 2003 at the tail-end of a bear market for stocks driven by the dotcom crash; in 2004 during a scandal over mis-stated oil reserves; at the height of the global financial crisis; and in 2016 when oil prices last bottomed out.

At $37.50, brent crude is currently trading higher than the $27.67 per barrel it reached in the last oil sell-off.

Shell’s shares delivered a total return (capital gains and all dividends reinvested) of 134% from its mid-January 2016 low to its most recent peak above £28 in May 2018.

While there remains considerable uncertainty over how Saudi Arabia’s actions will play out and just how severe the hit to crude demand from the coronavirus will be, we think so much bad news is already priced in to Shell’s shares.

Concerns over how the company will be affected by the issue of climate change mean this is not necessarily an investment for the long term. However, history suggests that by being brave and investing now you could achieve strong returns over the medium-term.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.