Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineIs the latest sell-off history repeating itself, and if so what can we expect next?

They say that history doesn’t repeat, but it certainly rhymes because this year’s large market sell-off has seen most sectors perform bang in line with their performance in previous sharp sell-offs.

As we previously explained, the past decade has seen three sharp in declines in stocks – in mid-2011, mid-2015 and the final quarter of 2018 – which all happened for different reasons but which all caused markets to fall by more than 10%.

Markets this year have experienced another sharp jolt downwards, caused by economic fears around the coronavirus and the sudden collapse of the oil price.

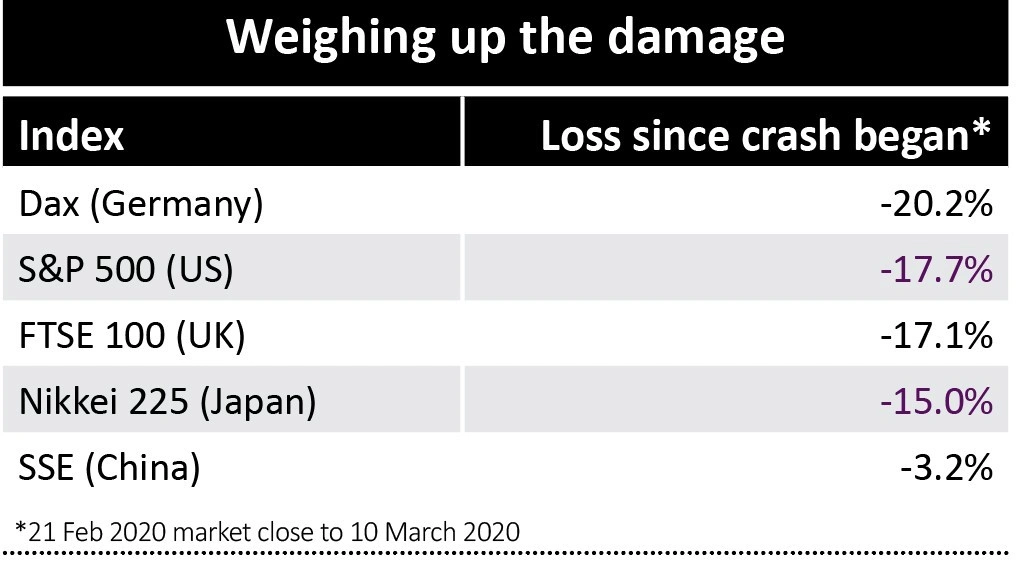

Since 21 February just before coronavirus went global and the market closing level on 9 March, the FTSE 350 index fell by 18.6%.

Individually, the internationally-exposed FTSE 100 lost approximately 17% while the more domestically-focused FTSE 250 lost 16%.

Bottom of the pile this time – completely in keeping with their performance in each of the three previous sell-offs – are automobiles and parts, oil equipment and services, and industrial metals, which have all racked up losses of 30% or more.

Meanwhile the best-performing sectors – utilities, pharmaceuticals, personal goods and tobacco – are also entirely consistent with past sell-offs.

SPOT THE DIFFERENCE

As always there are a few sectors which have bucked the trend for obvious reasons, but in other cases the moves look overdone.

No-one will be surprised that travel and leisure stocks such as airlines and hotels have performed much worse than usual as the coronavirus has directly impacted global travel.

Similarly, oil stocks have performed much worse than usual, first on fears of a global slowdown and more recently on the risk of a global glut of crude as Russia and Saudi Arabia tear up their production agreement.

On the other hand food and drug retailers, which typically lose as much if not more than the market during sell-offs, have barely missed a beat this time as investors have reacted to stories of shoppers stockpiling.

BIG OUTLIERS

Forestry and paper stocks, which are usually dumped by investors along with other commodity sectors during big sell-offs, have held up as demand for toilet roll sees supermarket shelves stripped.

In contrast, defensive sectors such as food and beverages have performed much worse than usual this time round, presumably as a read-across from the fall-out in travel and leisure stocks.

Fixed-line and mobile telecoms have also performed far worse than usual in this sell-off, possibly due to concerns over their high levels of financial leverage and the need to refinance their debt at some point.

WHAT HAPPENS NEXT?

We aren’t soothsayers, but typically when the market falls this much the rebound is at least as strong with many of the worst-hit sectors gaining the most over the next six months.

Industrial metals, the biggest faller this time round, is also typically the biggest gainer during the recovery, according to how markets behaved following the last three sell-offs. The sector includes miners Anglo American (AAL), Antofagasta (ANTO), BHP (BHP) and Rio Tinto (RIO).

Construction and materials is typically another big gainer following a crash, according to history. This sector includes names such as Balfour Beatty (BBY), CRH (CRH), Ibstock (IBST) and Marshalls (MSLH).

There is no guarantee these sectors will rebound as predicted and investors must understand that what’s happened in the past may not necessarily follow the same pattern in the future.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.