Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhat is behind Bitcoin's latest comeback?

At a time when a FTSE 100 member’s shareholder list looks flaky and shares in a fake meat company’s shares are sizzling again in the US it may come as no surprise to some investors that an alternative currency (or a fake one, depending on your viewpoint) seems to be coming back into vogue. Bitcoin is once more nearing the $10,000 mark.

Some may view this as another reason to view markets as worryingly frothy, as a plentiful supply of liquidity from central banks keeps them bubbling along. Others will argue the cryptocurrency’s return to favour affirms their view that central banks’ continued provision of cheap cash is only serving to debase existing currencies and open the way to major reset.

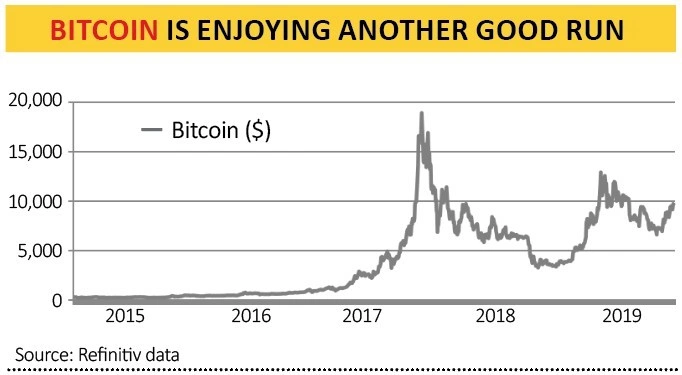

Bitcoin first reached $10,000 in December 2017, briefly recapturing that level in summer 2019 and the cryptocurrency is now trying again, as it trades near $9,800. That is still a long way below its all-time high of $18,941 from late 2017 but it represents a stunning recovery from the December 2018 low of $3,196.

Show me the money

According to the website www.coinmarketcap.com, the total value of Bitcoins in circulation is $178bn.

That represents almost two-thirds of total crypto market valuations and means Bitcoin is valued more highly than Royal Dutch Shell (RDSB), the largest company in the FTSE 100. It also means Bitcoin is bigger than all but luxury goods giant LVMH in Europe’s Eurofirst 100 index and would rank 32nd by market cap within America’s S&P 500 equity benchmark for good measure.

If Bitcoin keeps going, this could well rekindle the debates as to whether Bitcoin is ‘money’. That in turn fuels discussion over whether it is worthy of consideration as investment as part of a balanced portfolio.

The case for considering Bitcoin to be ‘money’ is that cryptocurrencies are money, as they facilitate transactions over time and distance and represent a trusted medium (at least by some), just as cowrie shells, cows, metal, slips of paper and plastic cards have since time immemorial.

So long as someone believes in cryptocurrencies they and their network have a value – and the more people there are in the network then the more value they may have.

Sceptics have three specific counter-arguments to this. First, the Bitcoin mining process is inefficient and energy intensive. Second, Bitcoin miners’ and transaction fees can make using the cryptocurrency inconvenient or even expensive, especially for micropayments.

Finally, Bitcoin is not a particularly efficient payment system. It can handle a maximum of around seven transactions per second. Visa

deals with around 1,700.

When it comes to seeing Bitcoin as an investment, believers will point to the crypto’s resurgent price.

Fans will also point to how Bitcoin supply is limited to 21m, a stark contrast to central bank-controlled fiat currency and an era of record-low interest rates, quantitative easing and spiralling government spending plans and budget deficits – and that is even before we get to Modern Monetary Theory.

In sum, Bitcoin is viewed by supporters as a store of wealth and protection against central bank and governmental monetary profligacy.

Value versus price

So-called ‘no-coiners’ will dismiss such arguments on three counts. First, they say, there is a theoretical limit to the supply of Bitcoins but the proliferation of initial coin offerings (ICO) suggests that crypto-currencies are no better at managing supply and providing sound money than the central banks.

The coinmarketcap website lists over 2,300 different cryptocurrencies Second, the Mt. Gox disaster, 2017’s enforced shutdown of the Silk Road website and 2019’s Bulgarian OneCoin scandal show that cryptos are subject to fraud (not that this admittedly unduly distinguishes them from other forms of remote payment or investment).

Finally, non-believers will assert that cryptos’ biggest alleged strength – they are not authorised or regulated or subject to ‘official’ control – is their biggest weakness.

Unless Bitcoin can be used to buy groceries or pay taxes, they have limited use and thus value, no matter how many you have, goes the argument, while there is always the risk that the authorities do get involved.

US president Franklin Roosevelt’s Executive Order 6102 criminalised the possession of gold in 1933 and Facebook’s Libra payments project has quickly encountered substantial central bank opposition.

As banking dynasty founder Mayer Amschel Rothschild once said: ‘Permit me to issue and control the money of a nation and I care not

who makes its laws.’ It seems unlikely that central banks will cede control, although Bitcoin believers will argue they could lose it.

It may be no coincidence that Bitcoin and cryptocurrencies are finding fresh support in the wake of 2019’s central bank policy U-turn which saw a shift to cutting interest rates rather than raising them and even fresh US Federal Reserve intervention in the US interbank funding markets.

Gold has rallied, too, perhaps for the same reasons. Although looking at the recent share price performance of meat-alternative provider Beyond Meat and next-generation car maker Tesla, older heads may just be tempted to dismiss Bitcoin’s renaissance in this context as the latest in a long line of bubbles fuelled by central bank-provided liquidity.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.