Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineReinventing BP: is the FTSE 100 giant going to turn its back on oil and gas?

Oil major BP (BP.) is the fourth largest company on the FTSE 100, representing 5% of the total market cap of the index. According to Link Market Services, BP and Royal Dutch Shell (RDSB) combined paid 20% of all dividends served up by UK-listed firms over the last decade. It is unsurprisingly a very popular holding in UK income funds owned by thousands of investors across the country.

Ultimately BP is one of the most significant companies on the UK stock market and investors should therefore take note of how the business might evolve in the coming years.

On 12 February it announced potentially the biggest shakeup in its 111-year history as it pledged to be net zero on its emissions by 2050. This news really matters as Link’s chief operating officer Michael Kempe observes: ‘Compared to other major countries, investors in UK equities are unusually reliant on oil to provide income on their shares.

‘As pressure builds on all firms to show environmental strategies, investors will be looking for clear direction, such as this announcement from BP’s CEO and from all the oil majors regarding their plans to decarbonise their operations when they are making future investment decisions.’

BP’s new chief executive Bernard Looney arguably had little choice but to lay down transformational plans given the growing clamour for the oil and gas industry to address its contribution to climate change, not only from environmental campaigners but from institutional investors and politicians.

Restructuring the business

For the first time in its history BP is abandoning the traditional upstream (oil and gas exploration and production) and downstream (refining and marketing operations) structure.

The new corporate structure splits the business into production and operations, customers and products, gas and low carbon energy, and innovation and engineering.

However, at this stage it is unclear whether BP’s net zero plan is ‘greenwashing’, a phrase to describe addressing environmental concerns but not following up with real action, or a genuine commitment to change.

That question may be answered more fully when the company hosts an investor day in September but in this article we will discuss the potential implications of the net zero pledge, in particular what it might mean for the company’s dividend, how the pledge might be achieved and where the company is starting from.

WHAT DOES IT ALL MEAN?

So what did BP mean when it said it wanted to be ‘net zero’ by 2050? In plain English it hopes to make no addition to the amount of greenhouse gases in the world’s atmosphere through either its operations or the oil and gas it produces. It is also aiming to halve the carbon intensity of its products by the same date (or sooner).

The ‘or sooner’ bit may become increasingly relevant as BP could face pressure to move more quickly on this issue.

BP’s pledge to cancel out the emissions from the oil and gas it produces is perhaps most eye-catching. In a Q&A session in front of campaigners, journalists and investors, Looney said the ‘tools in the toolbox’ for achieving this aim would include carbon capture, hydrogen and natural climate solutions.

Carbon capture and storage (CCS) involves trapping carbon in caverns or porous spaces underground and then transporting to locations where it can be stored or used.

A case of déjà vu? rehashing ‘Beyond Petroleum’

In July 2000 BP announced a PR campaign entitled ‘Beyond Petroleum’ ditching its traditional shield-based logo and replacing it

with a new sunburst design.

Tangible investment in genuinely moving beyond oil and gas was subsequently limited. It fulfilled a 2005 pledge to spend $8bn on renewables by 2013 but failed to set a new target and notably scrapped ‘Alternative Energy’ as a standalone business in 2009.

Hydrogen refers to the use of a variety of technologies, including the electrolysis of water and chemical synthesis of natural gas, to produce hydrogen-based zero-emissions liquid fuel.

Natural climate solutions involve tapping into natural carbon sinks, including oceans, plants, forests, and soil; these remove greenhouse gases from the atmosphere and reduce their concentration in the air.

However, these approaches and technologies have not yet been proved up on any significant scale.

A January 2020 report from think-tank the Atlantic Council noted: ‘The core argument held by many environmentalists against hydrogen and CCS is that they are too risky—meaning that continuing oil and gas production in the hopes that these and other future decarbonisation technologies will emerge could lead to a climate disaster should the technologies fail to materialise, and the population is consuming business-as-usual levels of oil and gas.’

Why should BP lead the renewables charge?

Given the toxic legacy of BP’s fossil fuel assets, why should it, rather than a company unencumbered by such a legacy, be part of the transition towards renewables?

According to Nick Boyle, the founder of solar business Lightsource, the answer is that oil and gas companies have been powering the world for 100 years. BP recently increased its stake in Lightsource to 50%.

‘Oil and gas companies have the experience of building large engineering projects in remote places, knowledge of the energy markets and huge trading capability as well as the necessary financial wherewithal,’ he says.

Steve Wreford, portfolio manager of Lazard Global Thematic (B241MZ1), also believes BP is a natural fit for the renewables space and doesn’t believe its current structure will hinder efforts to transform into a business fit for the next generation.

‘I look for companies with a solution to emissions rather than part of the problem,’ he says. ‘There are a select number of companies who can manage the transition from a world of fossil fuels to a world of renewables and emissions-light, which is about 20 to 25 years away. Some of them are renewable companies but not all of them.

‘We invest in BP which is busy rolling out its renewables platform. It still owns lots of oil fields but it can manage the transition.

‘People think of BP as an oil company but the life span of its proven reserves is 10 years. In other words, BP could be a totally different company by 2030 – it could be ‘Beyond Petroleum’ finally.’

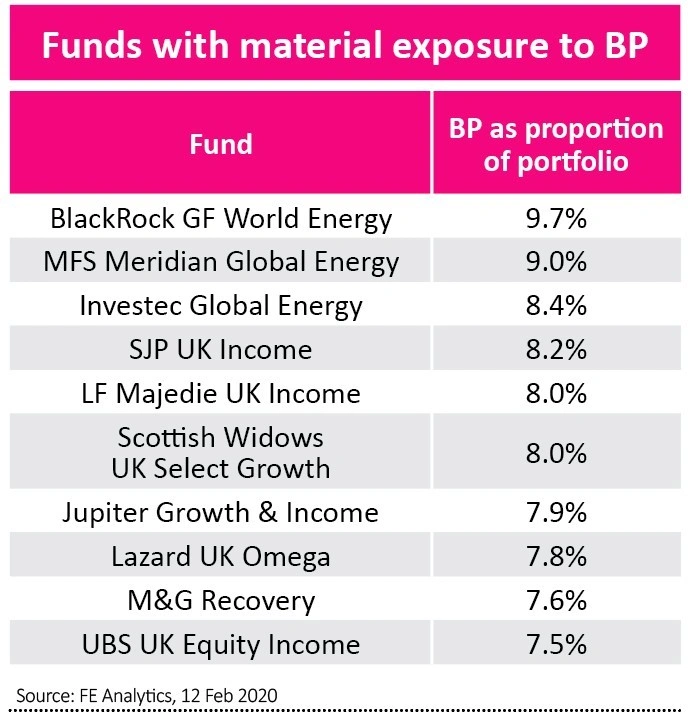

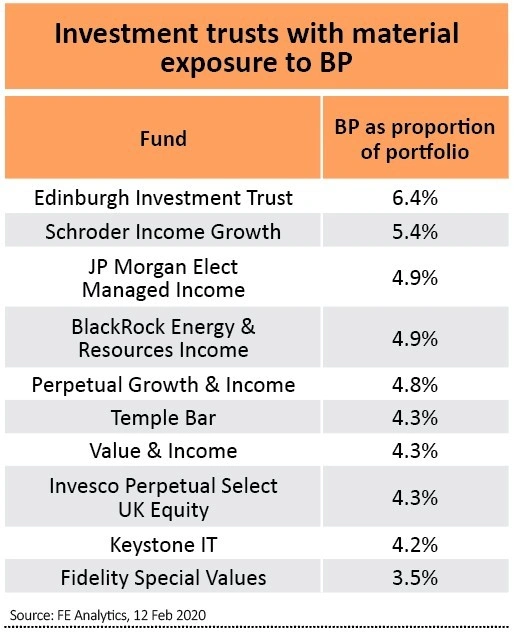

WHICH FUNDS ARE MOST EXPOSED TO BP?

The table shows the funds and investment trusts with the most significant exposure to BP in their respective portfolios. According to data from FE Fundinfo, 246 funds out of an Investment Association universe of 4,051 have 1% or more of their portfolio in BP; 67 have an interest in excess of 5%. The FE data also shows 20 investment trusts with more than 1% of their portfolios in the oil company.

WHAT ARE THE IMPLICATIONS OF BP'S PLAN?

Looney says nothing to be announced in September will compromise the principles of growing cash flow and distributions to shareholders, maintaining a strong balance sheet through capital discipline, and driving down costs.

However, there are three main areas which will almost certainly be affected by a plan to realign BP on this scale and have a greater reliance on renewable energy.

1. Dividends

Investment bank Morgan Stanley characterises the situation facing the big oil and gas companies, including BP, as an ‘impossible trinity’ of investing to maintain oil and gas production, building out what it calls ‘new energies’ businesses, and maintaining their current substantial dividends.

Referencing this challenge Morgan Stanley says: ‘In almost any scenario, this raises important uncertainties over the majors’ long-term dividend capacity. If they transition too slowly, what will underpin their earnings when oil demand plateaus and eventually peaks? Can the majors find new businesses that can match the historical profitability of oil?

‘On the other hand, if they transition too fast, will their new energies businesses be sufficiently profitable to underpin current dividends? So far, new energies returns appear a lot lower than oil and gas returns.

‘Even if the majors transition at precisely the right pace, and the returns in new energies are indeed sufficient, it will take many years before this becomes clear. For the next several years, investors are simply faced with considerable uncertainty.’

2. Growth

Looney says BP may still be producing oil and gas in 2050, although probably less than it does now. In the wake of the Gulf of Mexico oil spill the company has already streamlined itself, divesting billions of dollars’ worth of assets.

The company has signalled it will focus on the highest quality barrels. In practice that will to mean avoiding projects which involve more intensive work to get the oil and gas out of the ground. This includes assets in very deep water or oil which is particularly heavy or viscous as well as developments which involve dealing with high pressures and temperatures.

The company’s main growth initiative in the last decade was the acquisition of shale assets from BHP (BHP). This seems at odds with a ‘highest quality barrels’ approach given shale operations have a significant environmental footprint thanks to their land use and associated levels of water and air pollution.

3. Debt

BP is under pressure to reduce its borrowings. Gearing, which represents the ratio of net debt to total equity, hit 30.3% in the fourth quarter of 2019. Indebtedness has increased since 2018 as a result of the BHP deal.

This gearing ratio is just above the company’s 20% to 30% targeted range and was up from 27.4% a year earlier. The company plans to sell off more assets to get gearing down, yet investing in more capitally intensive alternative energy assets could put the balance sheet under strain.

SHOULD YOU BUY OR SELL BP SHARES?

The announcement of the net zero plan is only likely to ramp up the pressure on the business and this could be damaging to the share price.

Recent pressure on oil prices linked to the coronavirus outbreak is another headwind. Income is the main attraction of the stock – the company has a 6.8% prospective dividend yield based on consensus forecasts – and we do think it’s unlikely that the dividend will be cut in the foreseeable future.

However, this has to be balanced against the risk of further capital losses. September, when the company’s investor day should provide more meat on the bones of these new targets, looks like a potential negative catalyst.

What could happen? Either the company won’t go far enough to appease shareholders who want it to take decisive action on climate change or it goes too far and alienates investors who prize a dividend underpinned by cash flow from its oil and gas related businesses.

There are just too many unknowns and headwinds to warrant owning the shares now. Existing shareholders should sell and prospective investors should look elsewhere for opportunities.

What do the experts think?

One fund manager who wished to remain anonymous and who attended Looney’s presentation of the net zero plan told Shares

that the BP boss ‘walked a fine tightrope’ but reckons he carried it off. They note the retail investor perception that fossil fuels are bad therefore BP should get rid of them but point out this would just pass the problem to someone else and it would still be a problem for society.

Consultancy Lux Research’s Holly Havel says BP’s announcement references methane detection and low carbon investments, but highlights that BP’s broader decarbonisation strategy is centered around completely restructuring the organisation. ‘BP has struggled to reinvent itself in the past but may find more success as the industry reaches a turning point in the evolving energy transition.’

Berenberg analysts Henry Tarr and Ilkin Karimli see a risk from the whole oil and gas sector investing in this transition at once. ‘With substantial regulatory and technological uncertainty, not to mention increasing competition, it remains to be seen how fast and successfully such a transition can be made. We have already seen that crowding of industry investment into “growth” areas can drive overcapacity and weak returns (eg in gas and petrochemicals), although industry players will hope that such overcapacity is cyclical in nature and eventually reverts back to healthier levels.’

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.