Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

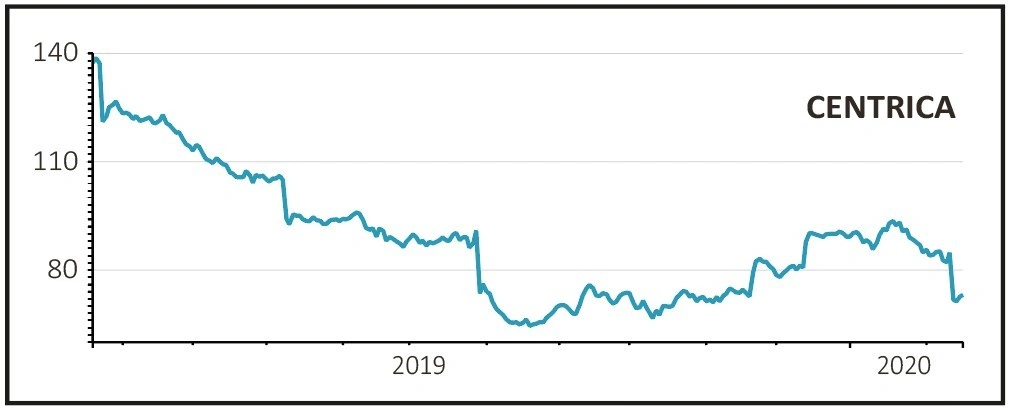

magazineWe remain positive on Centrica despite commodity price setback

Centrica (CNA) 73p

Loss to date: 19.2%

Original entry point: Buy at 90.42p, 19 December 2019

Our value-driven ‘buy’ call on energy firm Centrica (CNA) is off to an underpowered start thanks to a disappointing set of full year results (13 Feb).

The company reported adjusted profit down 35% to £901m and was forced to book a £1.1bn one-off charge linked to falling commodity prices and issues in its nuclear business.

There is an argument that weak natural gas prices, the nuclear outages it experienced and the new caps on energy tariffs were arguably outside of management’s control.

While operational issues might delay the disposal of its nuclear arm, the divestment of the 69% interest in oil and gas producer Spirit Energy remains on track with offers for the business expected around the end of the first quarter.

However, the sale price is likely to have been affected by the write-down and ongoing weakness in commodity markets.

On a brighter note the company is making progress with its core consumer energy arm, customer accounts were up 722,000

in 2019 and the company is ahead of target with planned cost savings.

SHARES SAYS: An undoubted blow, but as the business is reshaped we expect the market to respond to the value on offer. Be patient and aware of the risks to the investment case.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.