Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineMark Slater: the fund manager who keeps on delivering

If you chart Mark Slater’s run as a fund manager back to the start of 2000, you will see a significant outperformance versus his peer group over the subsequent years. According to financial data group FE, collectively across his funds Slater has delivered more

than twice the amount of returns to investors than his peer group (400% versus 145% respectively).

The son of the late Jim Slater, a famous financier and author of best-selling investment book The Zulu Principle, Mark now runs three funds focused on growth and income. His asset management business Slater Investments also manages a hedge fund and portfolios for pension schemes, charities and high net worth individuals.

THE SEARCH FOR GROWTH

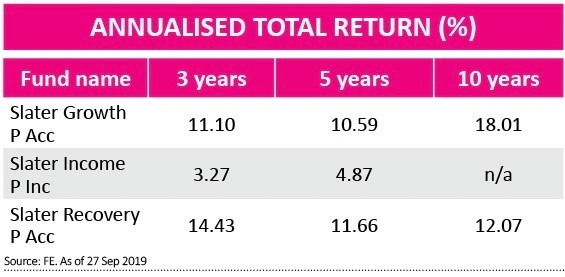

The flagship fund is Slater Growth (B7T0G90) which invests in UK stocks and which has been running since 2005. It adopts the same principles discussed in Slater senior’s book, namely having a tight focus on something rather than trying to do everything.

‘Our tight focus is having a methodology to find growth companies using value filters,’ explains Slater junior.

The PEG valuation metric is used as a starting point to find shares which have a proven track record of earnings growth and which are inexpensive. The metric compares the price-to-earnings ratio with a company’s earnings growth.

‘We use PEG as a screening tool, not as a share selection tool,’ says Slater.

Once the PEG screen has helped to reduce the investable universe, other measures are then overlaid such as cash flow screens. The fund manager also looks for companies with a competitive advantage such as a high market share, as well as positive signs in recent trading updates and directors preferably buying rather than selling stock.

TAKEOVERS GALORE

The growth fund typically has a concentrated portfolio of between 25 and 50 stocks, primarily in UK equities. This year alone has seen six portfolio holdings receive takeover offers including media content specialist Entertainment One (ETO) and insurance services group Charles Taylor (CTR).

A second fund called Slater Recovery (B90KTC7) has approximately 80% of the same holdings as Slater Growth. The name is a bit misleading as the manager isn’t targeting broken businesses which could be fixed, as per the normal definition of a recovery fund. Instead, the name relates to the period in which it launched.

‘It started in 2003 where we hoped for a recovery in share prices in the wake of a bear market. It isn’t about looking for deep value,’ he explains.

Slater Recovery fund differs from Slater Growth in that it also holds very small growth companies, such as £200m fire and safety expert Marlowe (MRL:AIM). Slater Growth tends to hold stocks in the upper end of the small cap space and mid-caps. ‘Since the financial crisis most growth opportunities have been found outside of the FTSE 100. We’re looking for double digit earnings growth, but the large caps may only have single digits.’

The third fund is Slater Income (B905XJ7) which only uses the PEG valuation metric to help construct a small part of its portfolio. The majority of its holdings are dictated by cash flow appeal and yield. Like the other funds, blue chips are rare in this product. ‘Ninety percent of the opportunity set for equity high income is outside of the FTSE 100,’ says Slater.

CONSISTENT PROCESS

The fund manager attributes his long-term outperformance to having a consistent investment process. He says other managers are easily distracted when their style is out of favour and they foolishly change their process to try and catch up.

It is widely appreciated that UK stocks are trading on low valuations relative to history and other parts of the world, and that overseas investors aren’t interested in the country’s stock market opportunities because of Brexit fears.

Slater believes the companies identified by his investment strategy aren’t really talking about Brexit and, like many consumers, ‘they are just getting on with the job’.

He is confident that the UK market will attract more interest once there is a resolution to some of the Brexit issues. ‘Capital will then start to flow back into the market. Valuations are attractive and if you take a three to five year view the outlook is pretty good.’

The fund’s investment committee met at the end of September and had a longer potential ‘buy’ list than stocks it wanted to sell, illustrating confidence despite a difficult market backdrop where the political noise is loud and the economic data (around the world) often disturbing.

Slater believes his approach is very effective and calls it a ‘sleep at night’ strategy, implying that anyone owning his funds shouldn’t have to worry about their money every day.

‘We’re investing in real businesses, we get to know them very well, and we hold for a long time.’

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.