Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineCan Japan tackle global trade concerns?

Investors with exposure to Japanese equities are enjoying the ‘Abenomics’ area, which dates back to Prime Minster Shinzō Abe’s general election victory in December 2012. Since then, the Nikkei 225 index has soared by 125% in local currency terms and 126% in sterling, compared to a 30% gain in the FTSE All-Share over the same period.

Yet the same Nikkei 225 still trades 44% below its all-time high of 38,916, reached on 29 December 1989. The Japanese banks sector is also down by 90% from the peak attained on the same day.

Economic growth remains patchy and inflation continues to run way below the 2% target laid down by the Bank of Japan, despite more than two decades of zero or negative interest rate policies and multiple rounds of quantitative easing.

Huge bouts of fiscal stimulus and government spending have yet to make more than a temporary difference. Any spurts in growth and inflation have quickly receded after the central bank or the government tried to throttle back on any monetary or fiscal stimulus, let alone withdraw it.

So if investors are wondering why the policy pivot by the Federal Reserve, in the form of fresh interest rate cuts, and the European Central Bank, via a return to quantitative easing, are receiving such a quizzical response from global equity markets now they know why.

Japan has been here before. And its failure to fuel either growth or inflation on a sustainable basis means that Japan remains the place where, metaphorically speaking at least, no Western central banker wishes to go.

Three-point plan

That said, the Abenomics programme of monetary stimulus, fiscal stimulus and social, economic and corporate reform has boosted the Nikkei.

It is also possible to argue that Japan’s economy is doing very well, given the number of obstacles that it faces, including the loss of the bulk of its supply of cheap nuclear fuel; a currency which has rallied by 15% against the dollar from its low of almost ¥126 to dollar in 2015; a string of natural disasters, including earthquakes and typhoons; and global trade tensions, which are seemingly starting to hit the world’s economy and therefore Japanese exports.

Global trade tensions are still a potential challenge for Japan, especially as relations with South Korea remain frosty, even if there are signs of an agreement with the US.

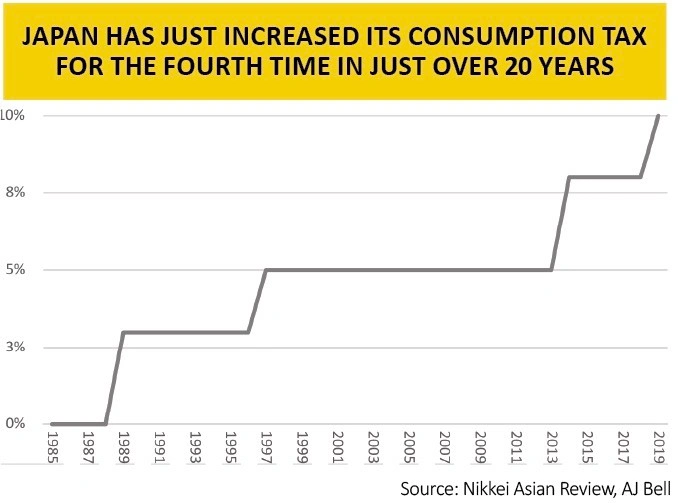

On 1 October, Japan increased consumption tax (its version of VAT) to 10% from 8%, after two delays. The postponements reflected worries over the impact on Japanese consumers and the broader economy. Japan fell into a recession after 2014’s increase from 5% to 8% and after 1997’s hike from 3% to 5%.

Abe’s time in office is drawing to an end. The Prime Minister has already bent his Liberal Democratic Party’s rules once, when a change permitted him to stand for the party presidency for a third, three-year spell in 2018. He will not stand for a fourth time in September 2021 and the next general election is due shortly afterwards for good measure.

Foreign invasion

The darkest hour comes before the dawn and on 15.5 times forward earnings with a yield of 2.1% Japan does not look particularly expensive relative to its 20-year history, according to consensus analyst forecasts.

It may not look knock-down cheap but real bulls of Japanese stocks will point out how foreign private equity firms are swarming to the Tokyo market.

For example, KKR is flagging how Japan is its favourite arena right now when it came to looking for assets to buy and this reflects what could be a strong internal dynamic to the Nikkei and Topix indices, as corporate governance improves and shareholder returns become an area of much greater focus for management teams.

In 2018 Japan overhauled its corporate governance code and in 2019 the Ministry for Economy, Trade and Industry made the first changes to the rules that pertained to mergers and acquisitions for over a decade.

As a result, takeover activity is picking up, as evidenced by a bid battle for hotel group Unizo. Activist investors are also starting to get traction. Sony sold its 5% shareholding in Olympus in the face of pressure to do so from American activist Third Point. Another US activist, Value Act, had already managed to force a change of chairman at the accounting-scandal-scarred Olympus and get three independent (and foreign) directors elected to the board.

Someone clearly thinks there is value to be had and bulls will argue that Japanese equities may be poised for further gains, especially if global trade relations settle down and global growth expectations start to surprise on the upside once more.

Equally, if global fixed-income markets are right and a global downturn or recession is due in 2020, then equities could struggle, even relative to Japanese government bonds, where yields may be nugatory but there is a guaranteed buyer of last resort, in the form of the Bank of Japan.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.