Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThe key reasons why Berkshire Hathaway is so successful

Best known as the investment vehicle of legendary value investor Warren Buffett and his business partner Charlie Munger, Berkshire Hathaway has also produced remarkable returns for outside investors since the pair took over running the firm more than 50 years ago.

Berkshire says its total gain in market value from 1964 to 2018 is a staggering 2,472,627%, or an average compound annual growth rate (CAGR) of 20.5%. In comparison, the S&P 500 index of US companies ‘only’ grew by 15,019% over the same period including dividends. This works out as a 9.7% CAGR.

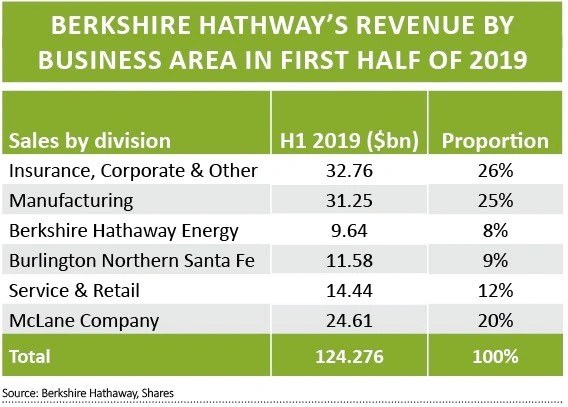

Although officially classed by Standard & Poor’s as an insurance company, only a quarter of Berkshire’s revenue came from insurance in the first half of 2019. A similar amount came from manufacturing, with the rest coming from the group’s significant holdings in energy, road and rail freight, retailing and services.

Over the past five decades Berkshire has gradually morphed from a company whose assets were largely concentrated in stocks to one whose major value is now in the operating companies it owns. When viewed as a whole, Berkshire actually owns a large slice of the American economy and its infrastructure.

However, rather than diving into the detail of each and every business Berkshire owns, which vary enormously in size and profitability, Buffett believes investors should look at them as five distinct groups each with a focus on their operating performance.

OPERATING AND RETAINED EARNINGS

The non-insurance businesses – usually 100% owned and never less than 80% owned – generated earnings of $16.8bn last year after costs, taxes, depreciation, amortisation and interest payments.

By comparison, Berkshire’s portfolio of equities – which were worth c$173bn at the end of 2018 – paid it dividends of $3.8bn last year.

More important than the dividends, in Buffett’s view, are the earnings which these companies retain each year.

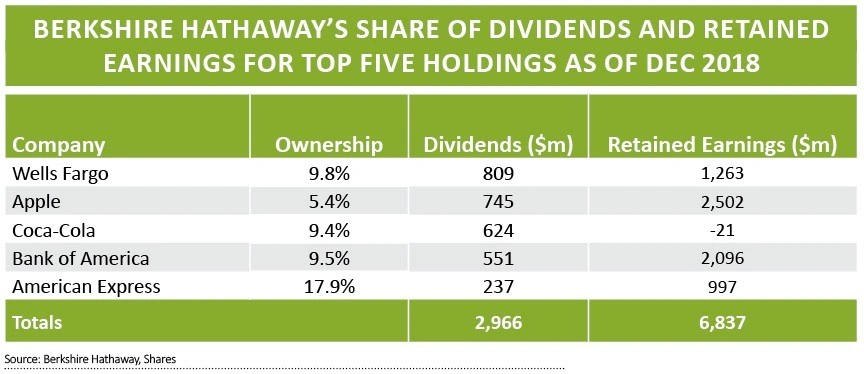

Dividends from Berkshire’s top five equity holdings amounted to just under $3bn last year whereas the firm’s economic share of their ‘retained earnings’ – money that is left after taxes, interest costs and dividends have been paid – was closer to $7bn.

The reason for looking at retained earnings rather than dividends is that among the things which investee companies can do with their money is buy back shares, which increases the economic value of investors’ holdings without them having to do anything.

As an example, Berkshire’s holding in American Express hasn’t changed in the last eight years in terms of number of shares, but thanks to buybacks by the company its ownership of the company has risen from 12.6% to 17.9%.

Last year, Berkshire’s share of American Express’s retained earnings was just under $1bn compared with its purchase price eight years ago of $1.3bn. As Buffett likes to say, when earnings increase and shares outstanding decrease, over time owners usually do well.

A FINANCIAL FORTRESS

The third group of assets are ones where Berkshire owns 50% or less of the shares but jointly manages the businesses.

The four companies in this category are food producer Kraft Heinz, where Berkshire holds 26.7% of the shares; mortgage and financial services firm Berkadia, where it has a 50% stake; utility firm Electric Transmission Texas, where it also owns 50%; and truck-stop and service centre operator Pilot Flying J, where it owns 38.6% of the shares.

Using operating earnings, Berkshire’s ‘split’ of these firms’ income last year was about $1.3bn.

The fourth part of the business holds cash, Treasury bills and other fixed-maturity securities, which as of June 2019 amounted to $200bn or close to 40% of Berkshire’s current market value, making it ‘a financial fortress’ in Buffett’s words.

At least $20bn of that money is untouchable, ‘to guard against external calamities’, but the hope is that the bulk of it can be put into businesses that Berkshire will permanently own.

The problem is that for now prices for good businesses with decent long-term prospects are ‘sky-high’. Therefore the more likely option is that some of that money will continue to trickle into stocks.

That doesn’t mean that Buffett is making a market call. He says: ‘Charlie and I have no idea as to how stocks will behave next week or next year. Our thinking is focused on calculating whether a portion of an attractive business is worth more than its market price.’

INSURANCE FUNDS ARE A ‘FLOAT’

The fifth part of the business is the insurance companies which Berkshire owns and the considerable funds which they generate.

Buffett refers to these funds as ‘float’, or a source of funding that he calls ‘cost-free, or even better than that, over time’.

Understanding such thinking is crucial to appreciating how Berkshire has achieved such stellar returns for more five decades.

Property and casualty insurers receive premium payments upfront and pay out on claims at a later date, which leaves them holding large sums of money to invest for their own benefit.

While individual policies and claims come and go, the amount of the ‘float’ tends to remain fairly stable in relation to premium volumes. As premiums grow, so does the ‘float’.

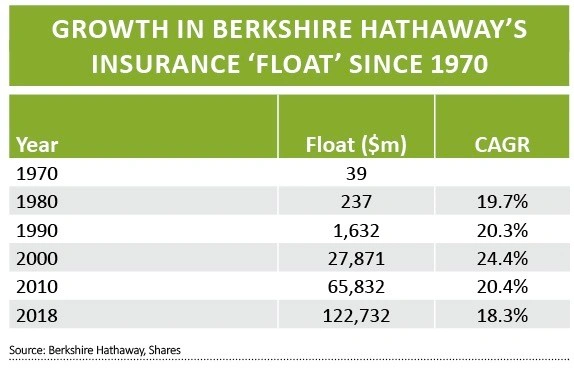

As the table shows, Berkshire’s ‘float’ has increased by roughly 20% a year since 1970 which is quite remarkable. This is partly down to the fact that its insurance businesses have an excellent underwriting record so each year they typically add profits to the investment income which the ‘float’ produces.

Berkshire is now the seventh largest reinsurer by premiums in the world, just behind Lloyd’s of London.

Buffett describes risk evaluation in its insurance businesses as ‘a religion, Old Testament style’, with managers keenly aware that poor underwriting results cannot be allowed to undo the benefit of the ‘float’.

So rather than having to pay for funds to finance its other investments, Berkshire has actually been paid in most years for holding and using other people’s money.

Buffett accepts that big risks can take many years to surface (as in the case of asbestos) or they can be sudden (as in the case of Hurricane Katrina). He is also under no doubt that a major event will come sooner or later, either natural (earthquake or hurricane) or man-made (cyber-attack), and the whole industry will suffer.

The difference is that while Berkshire can expect to take its share of losses, unlike other insurers it ‘will be looking to add business the next day’ while others are constrained.

HOW DO YOU INVEST IN BERKSHIRE?

Shares in Berkshire Hathaway trade on the New York Stock Exchange and can be easily bought on most UK investment platforms. There are two classes of shares. The ‘A’ shares currently cost $310,250 each which is probably beyond most investors’ means. That is why Berkshire has also issued ‘B’ class shares which are cheaper but have lower voting rights. These currently trade at $206.90 each.

We think this is a great business and its shares are well worth buying. The valuation isn’t as high as you might think – the price-to-book ratio is 1.2 and the price-to-earnings ratio is 19.2, based on consensus forecasts for the next 12 months published by Refinitiv.

An alternative way of getting exposure is through investment funds which have a stake in Berkshire. However, you would have to appreciate Buffett’s company would only represent a small part of a much larger portfolio.

Fidelity American Special Situations (B89ST70) has 5.8% of its assets in Berkshire. Among investment trusts, Personal Assets Trust (PNL) has 1.9% of its assets in the company and Berkshire represents 1.6% of Bankers Investment Trust’s (BNKR) assets.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.