Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy and how to get exposure to Vietnam

Vietnam has witnessed volatile stock market swings of late, yet risk-tolerant investors seeking exposure to a rapidly growing economy should not rule out putting money to work in Vietnam.

Gross domestic product (GDP) expanded by 7.1% in 2018, powered by positive demographics with a population of around 95m and an emerging middle class.

The market consensus is for GDP to grow between 6.5% and 6.7% in 2019 and 6.3% in 2020, forecasts placing Vietnam well above regional peers.

Significantly, Vietnam is increasingly regarded as an attractive manufacturing hub for foreign capital as labour costs are half those in China.

Furthermore, inflation is under control and despite wider emerging markets turmoil, the Vietnamese dong has been stable against the US dollar.

Bulls insist Vietnam remains one of the most attractive investment destinations in emerging and frontier markets, thanks to a stable political environment and a strong level of domestic consumption as wages and living standards rise.

ENJOY THE (VOLATILE) RIDE

Vietnam’s stock market is on a rapid development curve too, aided by a relaxation of foreign ownership limits and the government’s privatisation push. This frontier market could be promoted to the MSCI Emerging Markets index in the next few years.

According to Dragon Capital, as at 21 March 2019 the market was trading on 14.5 times historic earnings, falling to 13-times on prospective 2019 earnings estimates.

The Vietnamese stock market surged higher in 2017 and into 2018, peaking a year ago (April 2018). But a correction then ensued driven by fears over currency crisis contagion and US/China trade war worries. Year-to-date, the market has rallied with investor sentiment turning positive anew.

HOW TO GET EXPOSURE

There are various funds providing exposure to the country including exchange-traded fund Xtrackers FTSE Vietnam Swap UCITS ETF 1C (XFVT) which tracks the performance of a small group of mid and large-cap companies listed on the Ho Chi Minh Stock Exchange.

Actively-managed funds with Vietnamese assets as part of a broader portfolio include Barings Frontier Markets (B3SS8W4), Schroder International Selection Fund Frontier Markets Equity (BF104Q7), Aberdeen Frontier Markets (AFMC) and BlackRock Frontiers Investment Trust (BRFI).

There is also a trio of specialist Vietnam investment trusts trading on the UK stock market. The biggest by total assets under management is Vietnam Enterprise Investments (VEIL).

Managed by Dragon Capital’s Vu Huu Dien, this fund seeks long-term capital appreciation through holdings in listed and pre-IPO companies, seeking out attractively valued growth companies with good corporate governance and ‘alignment with Vietnam’s underlying growth drivers’.

The smallest trust by assets is VietNam Holding (VNH), attempting to turn around its fortunes under new manager Dynam Capital.

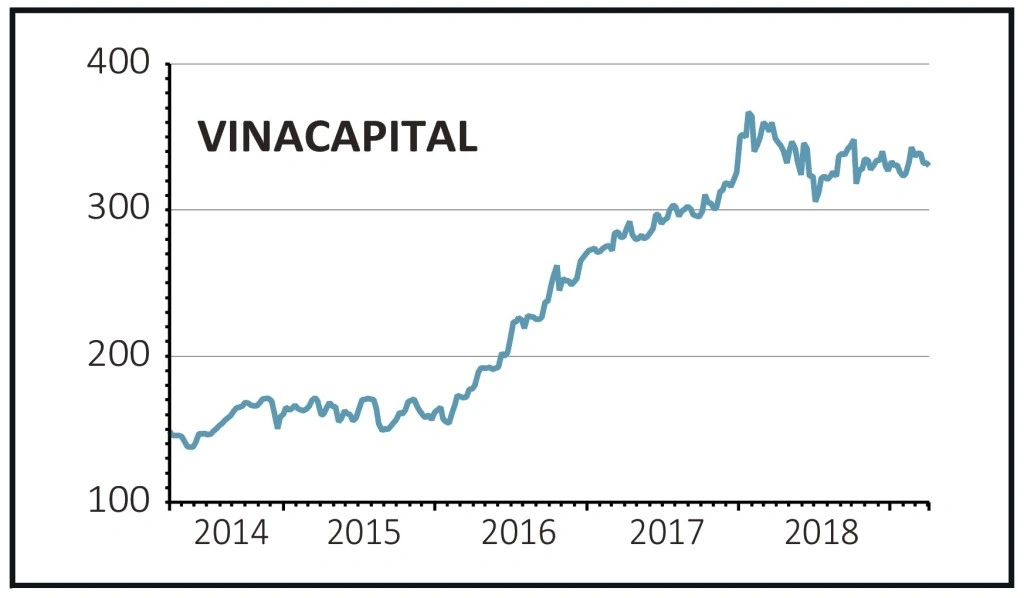

In the middle is VinaCapital Vietnam Opportunity Fund (VOF), a value-oriented portfolio which focuses on private equity and privately negotiated investments, with the fund taking stakes in listed and unlisted companies alike. Vietnamese entrepreneurs require capital and VinaCapital-managed VOF is one example of a partner that can help them to grow.

Addressing the advantages of backing companies when still private, VinaCapital Investment Management’s deputy managing director Khanh Vu informs Shares: ‘We don’t like to be subject to the volatilities of the market. By entering private, you get things that the public investor doesn’t get.

‘One is that you get to do a level of due diligence that you don’t get to do buying a stock. Secondly, when you have a private company, you get to have the optionality to list it and there’s your liquidity event, or you can take that stake and sell it to a strategic investor (trade buyer) at a premium.

‘The final thing is that we negotiate terms that are not available to the public market. And we make sure we get these minority protections. We are targeting between 15% and 20% internal rates of return on our deals – we are getting 23% on average for private equity deals that we have exited.’

VinaCapital Vietnam Opportunity Fund’s portfolio includes exposure to Vietnam’s real estate and construction industries through quoted holdings including real estate developer Khang Dien House and Coteccons, Vietnam’s biggest private construction outfit.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- The week's big news: Saga, Debenhams and more

- Funding Circle income fund to close after performance flop

- Brexit blamed for worst business investment figures since 2008

- Superdry shares still weak despite Dunkerton win

- Jupiter European funds downgraded as star manager set to step down

- Lack of IPOs is bad news for brokers