Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

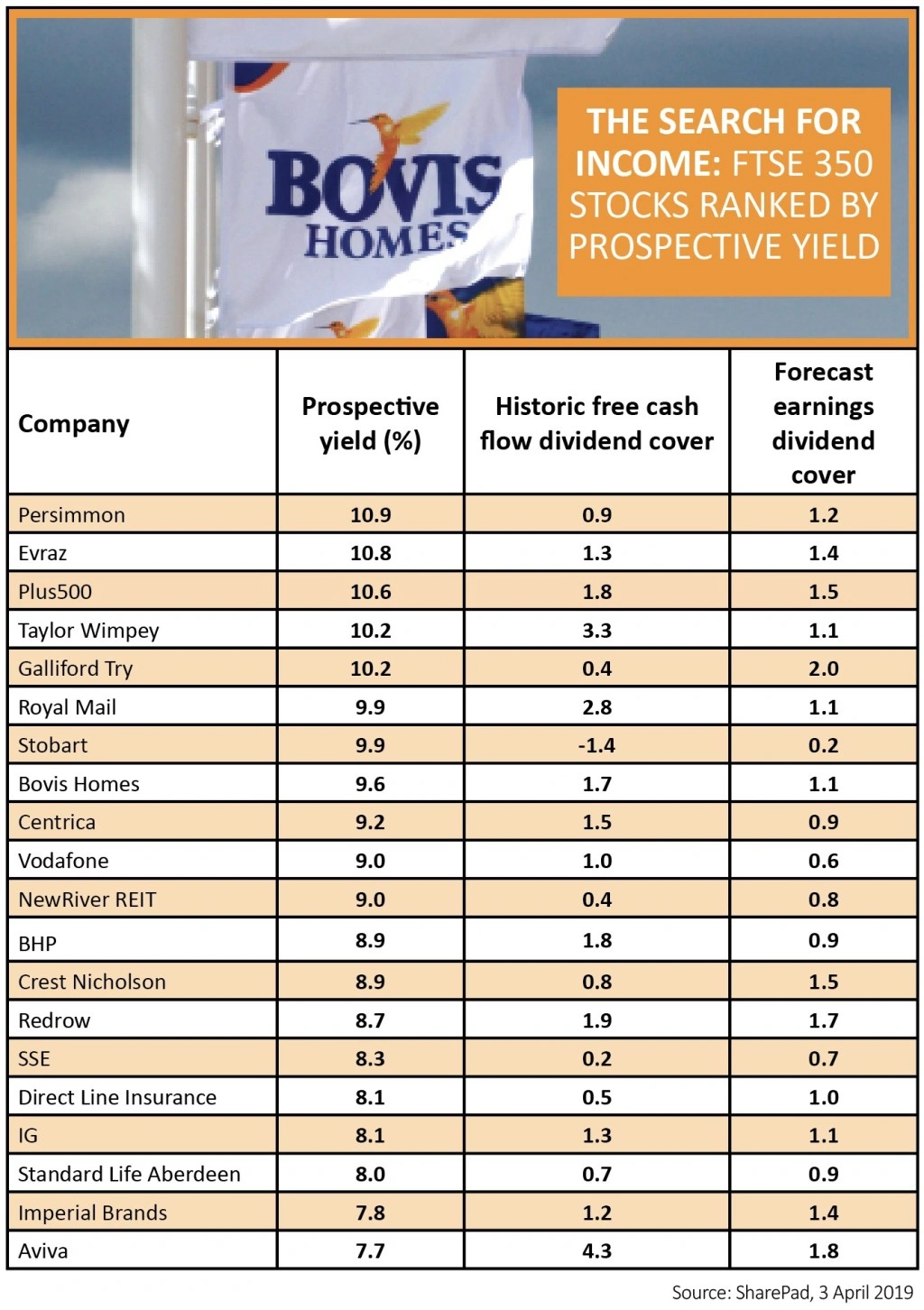

magazineThe biggest dividend yields in the FTSE 350

Dividends are a big reason people invest in shares. The prospect of securing a juicy yield on your money is an appealing one. And with the FTSE 100 paying a prospective dividend yield close to 5%, the income attractions of UK stocks have rarely been more evident.

But buyer beware, these dividends are not set in stone, and you need to do your homework to ensure you are not caught out by a dividend cut or even worse a payout which is cancelled entirely.

In this article we will show you the highest-yielding stocks in the FTSE 350 according to their forecast dividend payments. We will discuss why some of these yields – several of which run into double-digits – are potentially risky.

Finally we provide a potentially more sensible list for further research to help you identify examples where a strong yield is covered by earnings and cash flow.

WHY A HIGH YIELD CAN SPELL DANGER

A dividend yield is calculated by dividing the dividend per share by the current share price, expressed as a percentage. It makes more sense to focus on the forecast dividend payment so you can work out the yield based on what could be paid, rather than what already has been paid.

There are two important points to understand if you want to get to grips with dividends:

– The dividend yield will rise if the share price falls

– The dividend yield will fall if the share price rises

A very high dividend yield can reflect a big fall in the shares of the relevant company, so you need to find out what the market is thinking. A falling share price may be the result of some investors selling stock following a setback with operational or financial performance – or anticipation this could soon happen.

Persistent operational or financial problems can often lead to a cut in the dividend in the future, so the rising yield in this situation can act as a warning sign.

There are three high-profile names in our table which certainly fall into this category. Mobile telecoms firm Vodafone (VOD) yields a prospective 9%. It has large borrowings, faces significant competitive threats and could need to invest heavily in new radio wave spectrum for 5G services – a fifth generation mobile network which enables faster internet access.

Energy firm Centrica (CNA) has already signalled that energy price caps will constrain cash flow this year. In November the company had explicitly linked dividends to meeting cash generation and debt targets and, despite maintaining its payout at 12p for 2018, it has made no commitment for 2019.

The consensus forecast which underpins Centrica’s forward yield of 9.2% is 10.5p which implies a cut from 2018’s figure. However, some analysts think the dividend cut could be considerably larger. RBC analysts forecast a 2019 dividend of 8p, for example, and the company recently (2 Apr) revealed a downgrade from credit rating agency Standard and Poor’s. Meanwhile its British Gas consumer energy arm continues to haemorrhage customers.

Delivery service Royal Mail (RMG) has a 9.9% prospective yield. It has been hit by industrial relations problems, declining letter volumes amid tighter restrictions on marketing and has struggled to deliver on a series of promised efficiencies. This has implications for cash generation and could ultimately result in a dividend cut.

However, you also have to consider that the market sometimes welcomes dividend cuts, particularly if the share price has already fallen to such an extent that investors are already pricing in such a scenario. A reduced dividend effectively frees up cash for other things, and so markets can treat such news with open arms, particularly if it reduces pressure on a stretched balanced sheet.

Sadly investors who rely on dividends for income may not feel the same way if they’ve grown accustomed to generous payments over the years.

Elsewhere, housebuilders feature prominently on the list of 20 highest yielding stocks.

We wrote in January how many of these dividends were backed by strong net cash positions.

This situation implies, in the short term at least, that these companies could continue to pay generous dividends, even if rising costs and lower average selling prices raise questions about their ability to maintain this dividend generosity in the longer term.

LOOKING FOR SUSTAINABLE DIVIDENDS

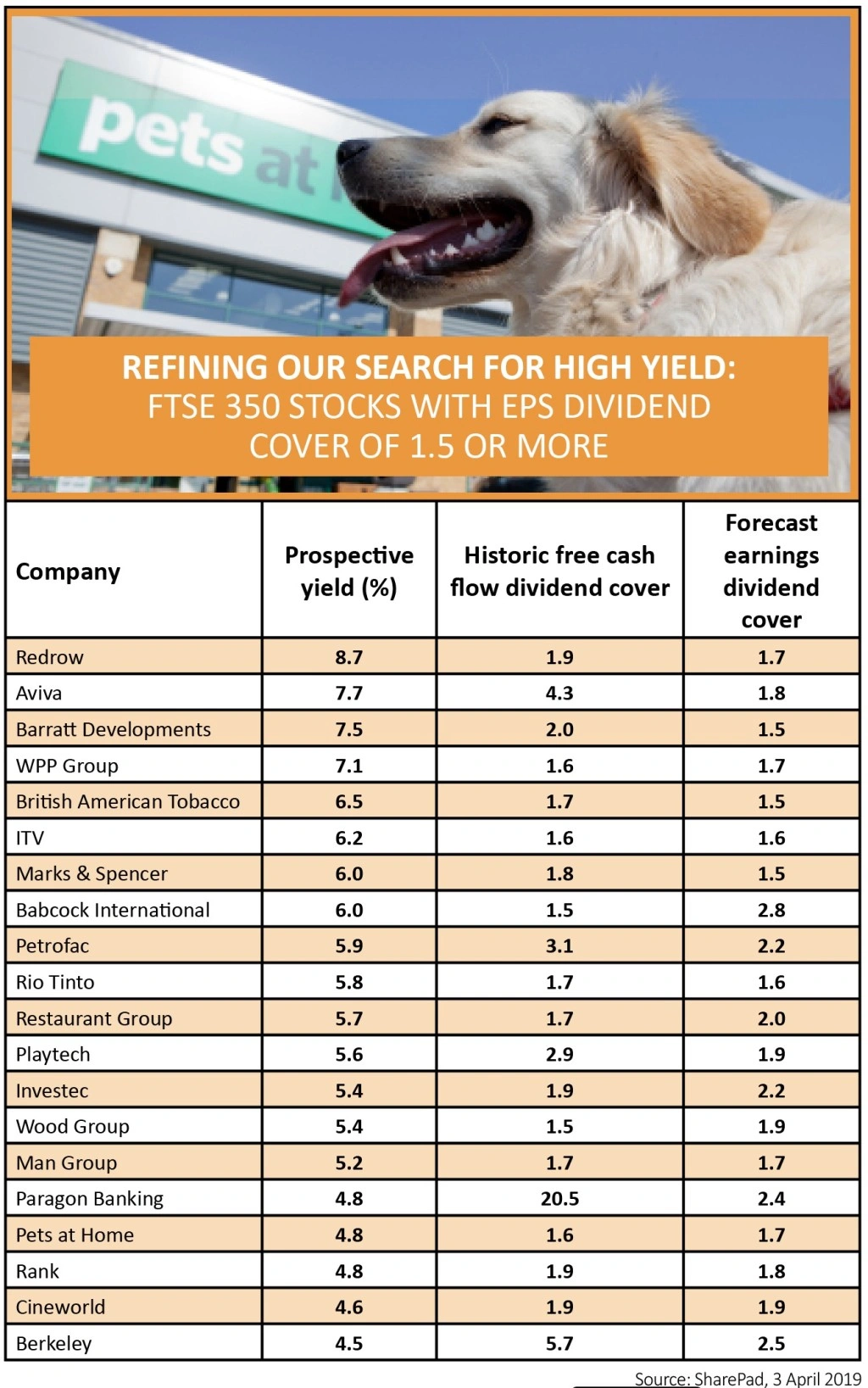

The second table shows the highest yielding FTSE 350 constituents which have their dividends covered at least 1.5 times by forecast earnings. This means that even if said earnings were to take a hit then there should still be capacity to maintain the dividend.

That said, it is important to note that dividends are paid from cash flow rather than earnings per share. The latter metric can be easily massaged to present a company’s performance in a better light.

Although we don’t have forecast free cash flow per share dividend cover, we have used historic figures and have only included firms which were able to cover their most recent dividend by at least 1.5-times from free cash flow.

Home construction outfit Redrow (RDW) is the only name which appears on both tables.

Ultimately no dividend is 100% guaranteed and investors need to consider building a diversified portfolio or invest in income funds rather than relying on the dividends from one or two stocks.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- The week's big news: Saga, Debenhams and more

- Funding Circle income fund to close after performance flop

- Brexit blamed for worst business investment figures since 2008

- Superdry shares still weak despite Dunkerton win

- Jupiter European funds downgraded as star manager set to step down

- Lack of IPOs is bad news for brokers