Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

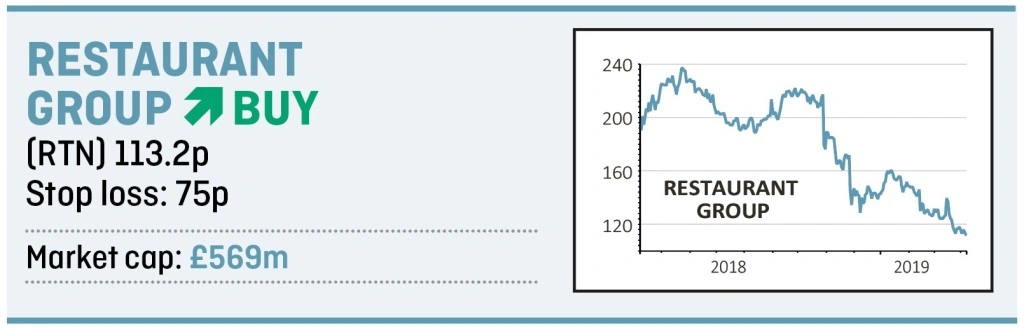

magazineRestaurant Group is too cheap to ignore: buy now ahead of the recovery

With its valuation, share price and arguably sentiment so depressed, now is the time to invest in Restaurant Group (RTN) in hope that the business can be fixed.

You’ll need to be patient as the shares are likely to be volatile until the company can provide enough evidence that its troubles aren’t getting any worse.

The appointment of a new chief executive and progress with the integration of successful franchise Wagamama (acquired last year) could act as catalysts to drive the shares higher. The next news flow is likely to be a trading update in May.

WHAT WENT WRONG?

The company ran into trouble through expanding too quickly in an over-saturated and stuttering casual dining market. Poor service standards and under-investment in existing sites contributed to the diminished appeal of franchises such as Italian-American diner Frankie & Benny’s.

The result was a string of profit warnings, driving the shares down from the highs above 500p in 2015 to a little over 100p today.

WAGAMAMA WORRIES

This share price sell-off hit a new phase in October 2018 when the company announced the £559m takeover of Wagamama and launched a discounted £315m rights issue to help fund the deal.

Many in the City felt the company had overpaid for the Asian food chain.

This was compounded when one of the architects of the deal, chief executive Andy McCue, announced plans to depart for personal reasons in February 2019. He remains in place for now while the company finds a suitable replacement.

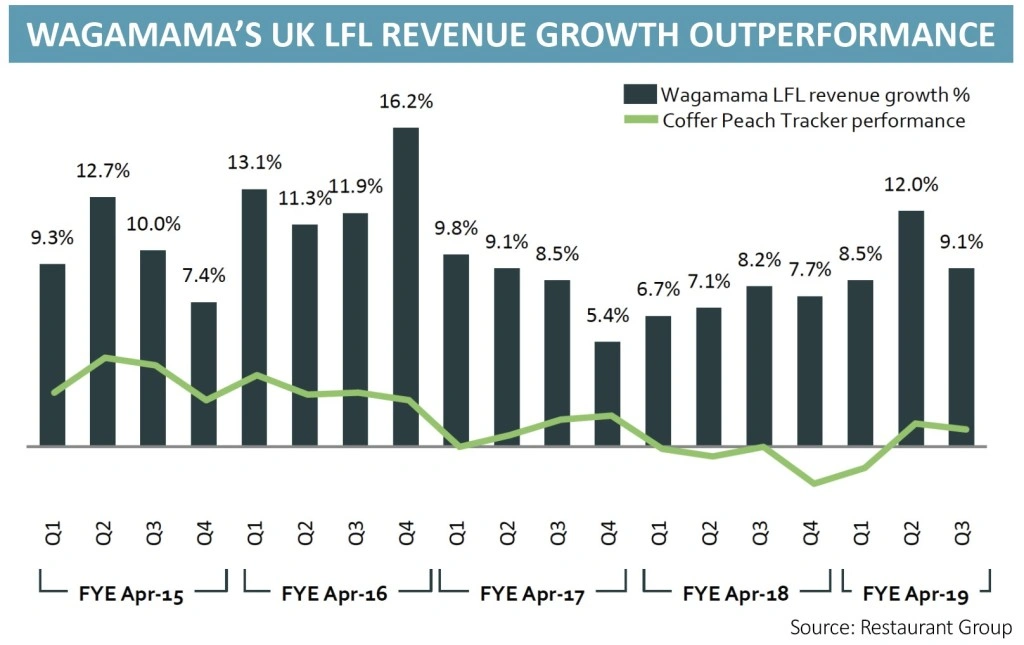

Full year results published last month were accompanied by a reassuring trading update, with like-for-like sales up 2.8% in the 10 weeks to 10 March and Wagamama’s sales up 9.1% in the 12 weeks to 3 February.

This sparked a brief relief share price rally, but it soon fizzled out and the shares have now halved since the Wagamama acquisition was announced.

At the current price they imply a 2019 price-to-earnings ratio

of 8.9-times and a yield of 5.7% based on consensus forecasts. This is a highly attractive entry point into the story, with investment bank Berenberg expecting a 19% compound annual growth rate in earnings between 2019 and 2021.

Whatever the criticisms of the price tag associated with Wagamama, it is now a substantial part of the Restaurant Group stable and the company has big plans for the brand. This includes a £2m investment in delivery and food-to-go offerings and the roll-out of at least six new restaurants in 2019.

WHAT ARE THE NEW PLANS?

In total the company plans to spend between £55m and £60m this year on these new sites, plus at least seven new pubs and between five and 10 new sites in UK travel hubs through its Concessions business. The latter involves running a mixture of its own and third party brands at airports and train stations.

Wagamama has won a place in Heathrow Terminal 3, opening in the second half of the year, and in the redeveloped Manchester Airport for early 2020.

It is also allocating between £30m and £35m to refurbishments and redevelopment sites.

Investment bank Canaccord Genuity believes the Terminal 3 restaurant could generate two or three times the revenue of a typical outlet adding that: ‘Medium-term Restaurant Group could triple the number of “super-sites” at UK airports: longer term, Wagamama should help Concessions grow overseas.’

Outlets in railways stations and airports often do well as they serve a time-poor, captive audience who often have no alternative other than to stomach higher prices.

This driver has been behind the success of airport food seller SSP (SSPG) which has seen its shares more than triple in value since joining the stock market in 2014, as well as for the travel arm of WH Smith (SMWH).

BACKING AWAY FROM LEGACY BRANDS

At the same time as reshaping its portfolio, Restaurant Group has the flexibility to scale back the underperforming parts of its Leisure business, principally made up of Frankie & Benny’s and Mexican eatery Chiquito.

In 2018 on a pro-forma basis, i.e. assuming Restaurant Group had acquired Wagamama at the start of the year, Leisure accounted for 30% of group earnings.

This should reduce over time with 41% of its Leisure sites having a lease end or break option within the next five years and some Frankie & Benny’s sites are being converted to Wagamama restaurants.

On the leadership front, former Wagamama chief Jane Holbrook has been mooted as a possible successor to McCue and the appointment of someone with experience in the restaurant industry would likely be warmly received by the market.

WHAT ARE THE KEY RISKS?

As you might expect, given the discounted equity valuation, there are risks for prospective investors to weigh. For example, the company may not hire someone with the right skills or experience desired by the market. Brexit could have a further negative impact on consumer sentiment, with the result that fewer people eat out.

The group could also run into trouble with its more elevated debt levels after borrowing to fund the Wagamama deal, with net debt of £291.1m running at just over two times earnings.

However, decent cash generation should help to pay down debt fairly rapidly and we are comfortable that these potential issues are being reflected in the share price.

Ultimately we’re turning positive because the stock is very cheap and the business now seems to have a plan how to drive earnings in the future. Tuck into the shares now.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- The week's big news: Saga, Debenhams and more

- Funding Circle income fund to close after performance flop

- Brexit blamed for worst business investment figures since 2008

- Superdry shares still weak despite Dunkerton win

- Jupiter European funds downgraded as star manager set to step down

- Lack of IPOs is bad news for brokers