Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineBlue Whale goes straight to the top end of the fund chart

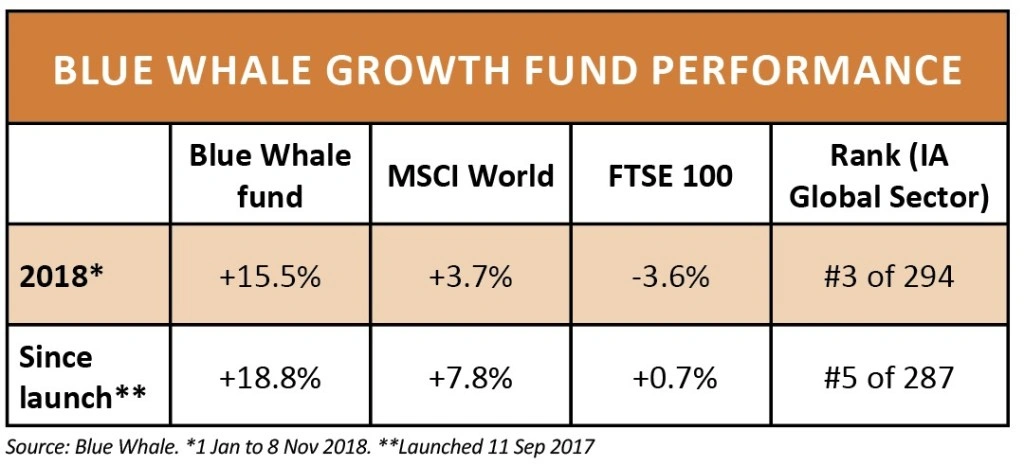

The team behind LF Blue Whale Growth Fund (BD6PG78) have set the bar very high with their debut performance. The product launched in September 2017 and went to the top end of the funds chart.

In its first year, the fund outperformed the MSCI World index by 13.1% and the FTSE 100 index by 22.3%, meaning it ranked in the top 1% in the IA Global Sector.

Delivering such impressive results means that some investors may expect superior returns going forward. That puts a lot of pressure on the five-strong investment team (two fund managers, three analysts) who are not only battling a difficult market backdrop at present, but also trying to live up to investors’ heightened expectations.

THE INVESTMENT PROCESS

The fund’s goal is to deliver outperformance of least 5% per year versus the MSCI World index. Fund manager Stephen Yiu says that is only possible if you run a concentrated portfolio, namely you’ve got to take big bets on specific stocks rather than spread yourself too thinly with countless holdings.

The Blue Whale fund aims to hold 25 to 35 stocks in its portfolio. ‘We are truly active, not buy and hold,’ explains Yiu.

He says the investment process is very different to many other global funds because his team do their own research and do not speak to brokers or read third party analyst notes.

Yiu also claims his team spend more time per company than many other funds, excluding ones run by very large asset managers like Schroders who have considerable resources.

‘There are five of us in the team. We work 10 hours a day, so 250 hours a week combined, or 1,000 hours a month. For a 25-stock portfolio that means we spend 40 hours on research per stock per month. We think our competitors only spend five hours per month per stock.’

LONG-TERM GROWTH FORECASTING

Yiu believes Blue Whale has an edge through its own modelling, in particular taking a strong view on long-term earnings potential.

He says the market is very inefficient with forecasting earnings beyond 18 months to three years. He believes analysts are merely following the pattern of believing what a company’s management predict near-term and then assuming that earnings growth will slow down over time.

‘The market underappreciates long-term growth potential and longevity of growth,’ says the fund manager. Essentially he is saying that while a company may look expensive on current valuation metrics, it could look far more attractive if you look further out.

He gives the example of Amazon. ‘Before the market sell-off it was trading on 50 times earnings with a 7% operating margin forecast in two years’ time. That’s the margin the business said 20 years ago it would achieve over the long-term. But the business has since evolved.

‘Its AWS web server business is growing at 50% a year with 30% operating margin. The advertising side of its business is growing at over 50% a year with 60% to 65% operating margin.

‘If you put everything together our long-term operating margin for Amazon is up to 20%. The timing of hitting those numbers depends on its expansion plans.’

Yiu says that Amazon’s shares are cheap even on a 50-times price-to-earnings multiple. ‘You’ve never had a business like Amazon where anything it does is margin accretive; that’s because it started from such a low base.’

The Blue Whale Fund has a global remit; while 60% of its holdings are listed in the US, many of these businesses are global in nature. Some of the names are stable holdings in other global funds like the aforementioned Amazon and Google-owner Alphabet. Other popular names with global funds are noticeably absent from Blue Whale such as Apple which Yiu criticises for not growing or innovating.

‘We don’t do anything special in terms of investment philosophy,’ says the fund manager, somewhat candidly. ‘There is no magic formula’. This modesty clearly understates the expertise of the team.

PORTFOLIO POSITIONING

Blue Whale sees the biggest short-term risk to markets as the US Federal Reserve raising interest rates too quickly.

The fund says it wouldn’t typically invest in companies with high levels of direct exposure to interest rates, commodity prices or industrial cycles, which explains why the portfolio mainly features technology, consumer and healthcare stocks as it believes they are less impacted by macroeconomic factors. Current names in the portfolios include payments group PayPal, computer software business Adobe and healthcare-focused cloud computing firm Veeva.

A key ingredient behind the team’s success, along with taking a longer-term view with earnings potential, is its awareness of issues that could affect a company and knowing companies inside out.

‘Many analysts are lazy and just put down numbers between 1% above and below those guided by company management in their earnings models.

‘As fund managers we try and understand how the last three years’ earnings for a company were delivered and whether something has changed, plus how macro factors could impact,’ says Yiu. ‘We look at what’s already known in the market and recognise how these issues are relevant to various companies.’

He says many fund managers in the near future will blame disappointing performance on areas such as tariffs, Brexit and currencies. His view is that they should have already factored this issues into their research and stock picking, as that’s their job. (DC)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.