Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineTurn patience into profit

Compounding is a fundamental force, a bit like gravity. In fact Einstein is said to have called it the most powerful force in the universe.

While gravity pulls a snowball downhill, it’s compounding that makes it grow bigger.

As it rolls downhill the snowball collects more snow: the further it rolls the more snow it collects.

UNDERSTANDING THE COMPOUNDING EFFECT

In the same way, the longer you hold an investment the greater the power of compounding. So how does it work?

Say you invest £1,000 in a stock and the shares go up 10% in a year. At the end of that year you’ll have £1,100, your original £1,000 plus £100 of gains — (see chart A).

If the shares go up 10% the next year you’ll have £1,210 as you’ve generated a gain not just on your original investment of £1,000 but also on the £100 gains you made last year.

If the shares keep going up 10% a year for 10 years, you’ll end up with £2,588 as you keep making gains on your previous year’s gains. You actually double your money after just over seven years.

If you keep the same shares and they go up 10% a year for another 10 years you’ll end up with £6,714 or more than six times your money.

Notice how steep the increase is in the last few years, which means most of the benefit comes from sticking with it.

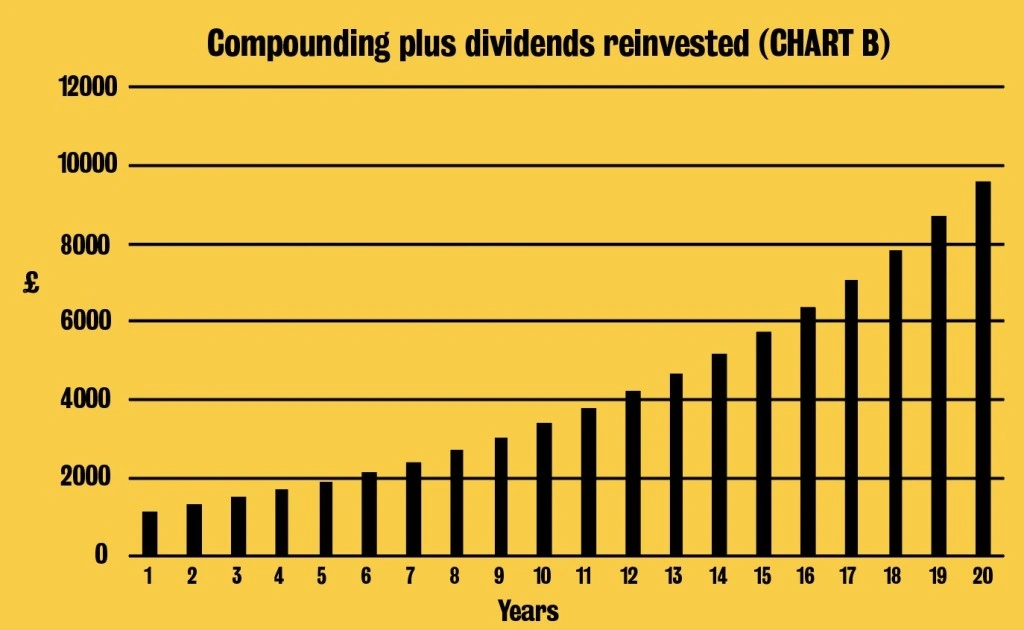

THE POWER OF DIVIDEND REINVESTMENT

If as well as going up 10% a year your shares pay you an annual dividend of £50, re-investing these dividends rather than getting a cheque every three or six months could substantially improve your returns — (see chart B).

In this case, at the end of the first year you have £1,150 – your original £1,000 plus £100 of capital gains plus £50 of dividends.

If you keep reinvesting the dividends then instead of doubling your £1,000 in just over seven years, it doubles in less than six years. In 10 years it turns into £3,390 rather than £2,588, almost a third more.

If you stick with it for the whole 20 years, rather than £6,714 you end up with £9,591 or over 40% more than the return from not re-investing the dividends.

Again, as the chart shows, your returns accelerate towards the end.

Most investment platforms, including AJ Bell Youinvest, allow you to opt for dividends to be reinvested automatically.

For those wanting to let someone else re-invest dividends for them, many investment trust and funds have ‘accumulation’ units which will automatically do this without your having to tell them.

BANKING THE DIVIDEND

On the other hand you could have just banked the £50 of dividends every year instead of re-investing it, in which case you would have £7,714 consisting of £6,714 from your original investment plus £1,000 in dividend cheques.

Or you could have spent the £50 in which case over 20 years you could have bought 400 Big Macs at £2.50 each or 200 pints of strong lager at £5.00 each.

Now imagine that as well as re-investing your dividends you invest another £1,000 at the start of the year, so you start the second year with £2,150 instead of £1,100 — (see chart c).

After five years you’ve invested £5,250 – five lots of £1,000 and

five dividend payments of £50 – and with the same 10% increase a year you will have £7,021 or a third more.

After seven years and an investment of £7,350, you amass £10,106, and after 10 years and an investment of £10,500 you end up with a whopping £18,328 or almost 75% more than you’ve invested.

If you keep this exercise going and invest £1,000 of capital plus the £50 of dividends each year for another 10 years, you’ll have turned £21,000 into £65,866 or more than three times your money, assuming a constant 10% annual return.

THE IMPORTANCE OF STAYING THE COURSE

Again note how sharply the curve rises in the last few years. In fact your returns double in the last six years which is why it’s so important to stay the course.

As well as staying the course to allow the power of compounding

to work, another crucial rule is to start early.

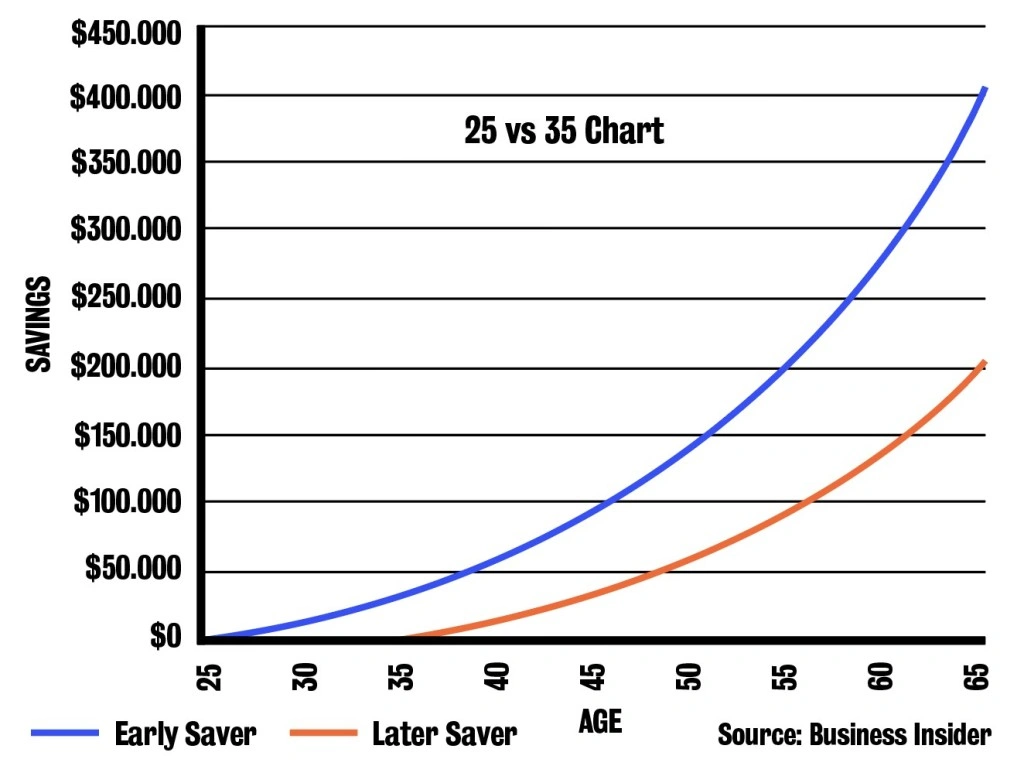

The chart, shows the difference that investing early can make to your retirement pot.

If two people want to retire at 65, with one investing regularly from age 25 and the other investing the same regular amount from age 35, the difference those early years make is staggering.

The early saver (blue line) invests a third more than the later saver (red line) but their retirement pot is almost double as the scale of the gains accelerates in the latter stages.

STARTING EARLY

In fact if you start putting money aside early enough and let it compound you could stop paying in at some point and just let the funds compound themselves.

Research firm CLSA looked at savers who each invested £2,500 a year in a pension growing at 7% per year.

One started at 21 and stopped at 30, while the other started at 31 and didn’t stop until they hit 70.

Remarkably the first saver ended up with the bigger pension pot by age 70 — £533,000 against £534,000 — even though they made no contributions for 40 years.

The early saver pays in £25,000 but the power of compounding means returns are greater than the later saver who pays in £100,000. (IC)

Compounding in action: JPMorgan Chase

US investment bank JPMorgan Chase has a tool on its website which allows you to calculate your return on an investment in its shares from 1972 to the present day.

To create a more realistic timeframe, let’s take a shorter 30-year period which means looking at data from November 1988.

If you’d bought 100 shares 30 years ago at $32.87, your initial investment would have been worth $3,287.

The share price traded below this entry level during several periods including the early 1990s and again around the financial crisis

in 2008.

But by staying invested through the entirety of this period your initial $3,287 investment would be worth $33,387 today.

And if you’d reinvested dividends your investment would be worth $68,681.74.

The chart shows that a significant chunk of this value has been achieved in recent years, underscoring the importance of patience in your investing. (TS)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.