Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy Warren Buffett seems to be running scared of bonds

The decision by Warren Buffett to spend some of his Berkshire Hathaway investment vehicle’s enormous cash pile on a share buyback is grabbing the headlines, as it suggests the legendary investor is struggling to find a company that he wants to acquire at a price he wants to pay.

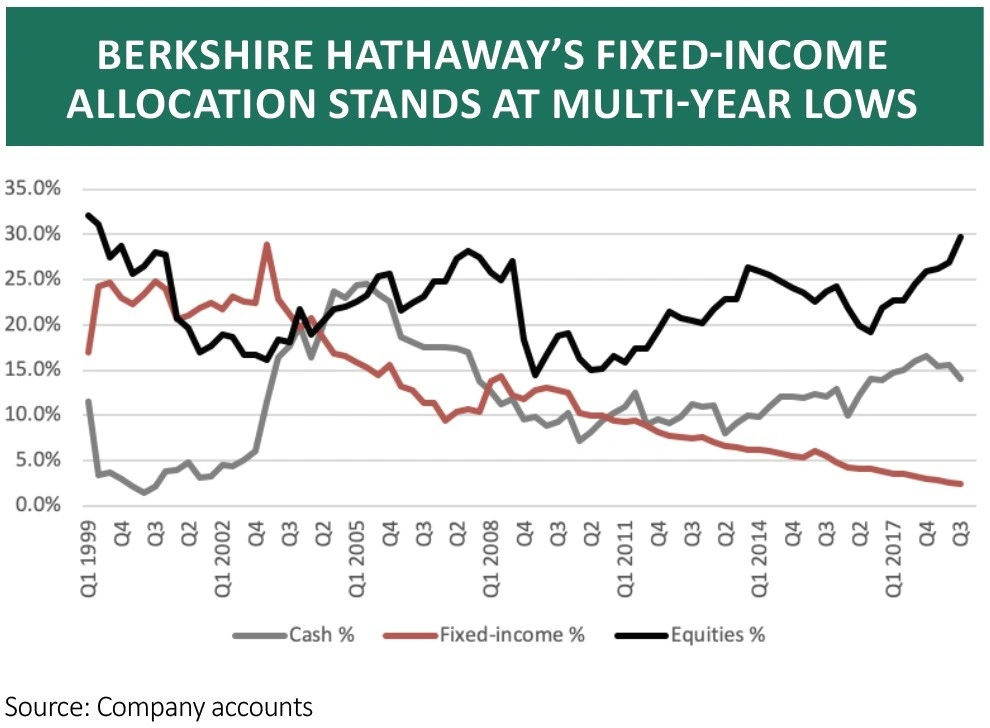

But a deeper look at how Berkshire’s balance sheet breaks down by asset mix, rather than in just absolute dollars, suggests that the Sage of Omaha is a lot more concerned about fixed income than he is about stock markets. At $18.7bn, US Government bonds represent just 2.5% of Berkshire’s assets, continuing a downward trend that has been in evidence since 2003.

It is not Buffett’s style to make macroeconomic calls. He instead prefers to focus on company fundamentals and particularly valuation, so perhaps the gradual decline in the fixed income allocation reflects a view that bonds represent relatively poor value.

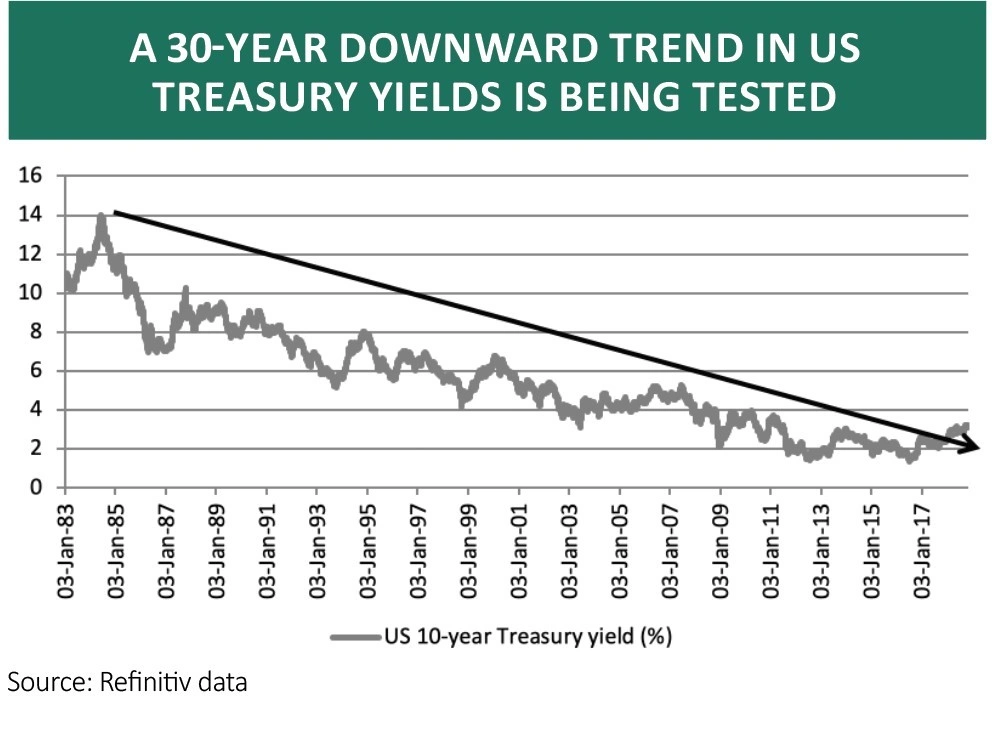

US wages grew 3.1% in October, a figure which suggests a summer drop in the headline overall inflation rate to 2.3% may not last long, a trend which could mean that even a 3.2% yield on the US 10-year Treasury, for example, may not offer as much wealth protection as investors would like.

In such an environment it is easy to understand why the US Federal Reserve seems intent on pushing through further interest rate increases, with one more planned for December and possibly for 2019. If it executes that plan, the American central bank will have overseen a dozen interest rate hikes of a quarter-point apiece by next Christmas, to 3.25%

Such a trend could well drag US 10-year bond yields higher still and, as we all know, bond prices move inversely to their yield.

SEISMIC SHIFT

It does seem that Mr Buffett is taking evasive action on the fixed-income front and this chart of the US 10-year Treasury bond yield suggests he may be right. It can be argued that a long bull run is ending.

Whether that is down to the end of QE, higher US Budget deficits (which would mean America needs to issue more bonds to fund itself just as the Fed stops buying) or inflation remains to be seen. But if Treasury yields do go higher that would leave investors with an environment we have not seen since the 1970s, especially if inflation does start to motor.

The logical conclusion of this is that the investment strategies that have served advisers and clients well since the early 1980s may not work so well going forward. This could beg a reassessment of fixed-income exposure, especially at the very long end where yields are traditionally the highest and a cold look at growth and momentum strategies, as cash flow would become more highly valued than profitless revenue growth or customer land-grabs.

In the 1970s, the best performers were gold and, from an equity perspective, consumer staples firms and the providers of life essentials - anything you could eat or and drink or pour down the sink to keep your house clean. A return to inflation could therefore mean it might be time to reassess precious metals and also stocks with pricing power. Firms with it will be able to defend their margins, profits, cash flow and thus dividends. Those without it will be poor selections indeed an in inflationary world.

FEEL THE POWER

Pricing power is a key requirement for Buffett before he invests in any stock, which takes us back to where we started. He seems to be shunning bonds but may also be having difficulties in finding companies that he likes at a valuation he likes.

Remember that he railed against the latest wave of merger and acquisition activity in this year’s Letter to Shareholders (not that chief executives have listened, judging by this year’s bumper takeover activity around the globe).

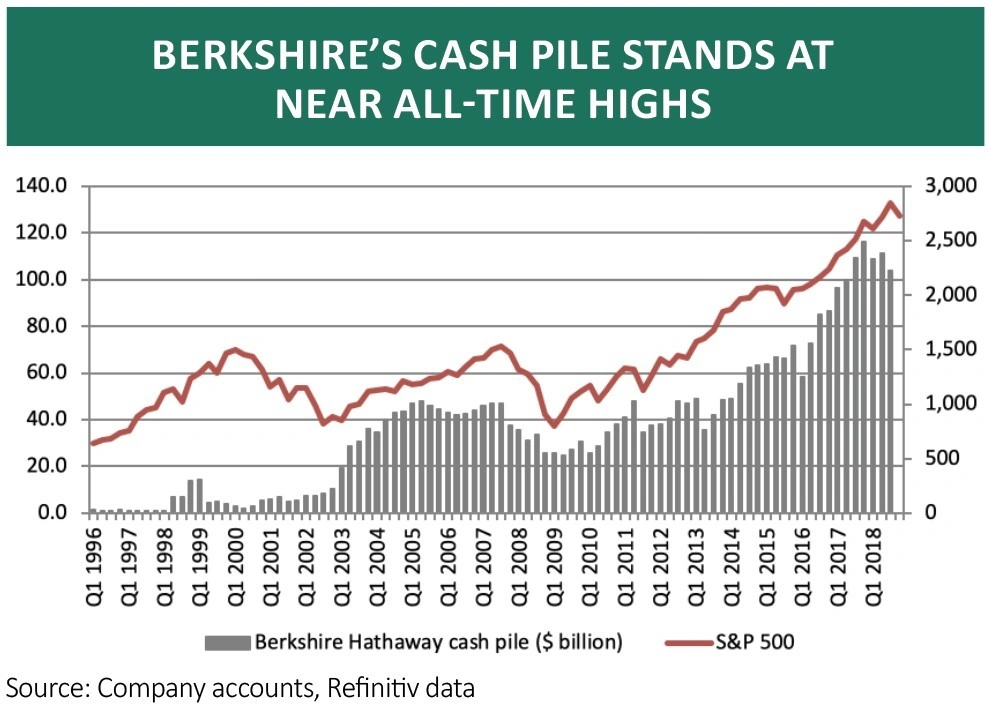

Berkshire’s cash pile, including short-term Treasury bills, stands at a near-record high $103.6bn. That represents 14.1% of Berkshire’s assets although that figure is way down, from the 24.5% high of 2005, when Buffett had clearly begun to develop doubts about the bull market that began in 2003, ran out of puff in 2007 and cratered in 2008-09.

It is also noticeable how equities, including a $17.5bn stake in Kraft-Heinz, now represent 29.7% of Berkshire’s assets, up toward the levels seen at the last two US stock market peaks.

It will therefore be interesting to see how Buffett and business partner Charlie Munger husband their cash from here, given their patient, long-term approach.

Russ Mould, investment director, AJ Bell

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.