Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineShining a light on Midwich’s bright future

The world of audio visual (AV) equipment has changed radically since Midwich (MIDW:AIM) started life in the 1970s. At that point, the products it dealt in were mainly overhead projectors. Today the technology has moved on but the company has kept pace.

Midwich’s managing director Stephen Fenby describes the business as sitting ‘between the manufacturer and the customer’ liaising with both to find the right solution for the client’s need.

The company serves a vast range of clientele, from individuals to large corporates. Its job is to supply them with whatever AV equipment they need to present information to their staff, customers or in the case of universities and schools, students.

When asked why doesn’t the manufacturer simply cut out the middle man, Fenby is candid enough to admit they sometimes do. But not often enough to halt the company’s consistent growth.

Midwich’s revenues even grew through the financial crisis years of 2008- 2009, from £173m in 2008 to £184m in 2009. Before joining AIM in May 2016, the company executed six bolt-on acquisitions between 2006 and 2010. This supported entry into the French and Irish markets.

It has since gone into Germany as well as Australia and New Zealand. Across Australasia as a whole, the company enjoyed 42.8% revenue growth from 2015 to 2016. It acquired Wired in New Zealand which helped lay foundations for this rapid growth in revenue from the country.

Big names on its client sheet

Among the list of manufacturers that Midwich works with are top tier names including Samsung, Sony, Panasonic, Philips and LG to name a few of the 300 partners the company has.

There is also plenty of diversification in its business model, serving as it does around 10,000 individual customers, many of which are intermediaries for the eventual end user.

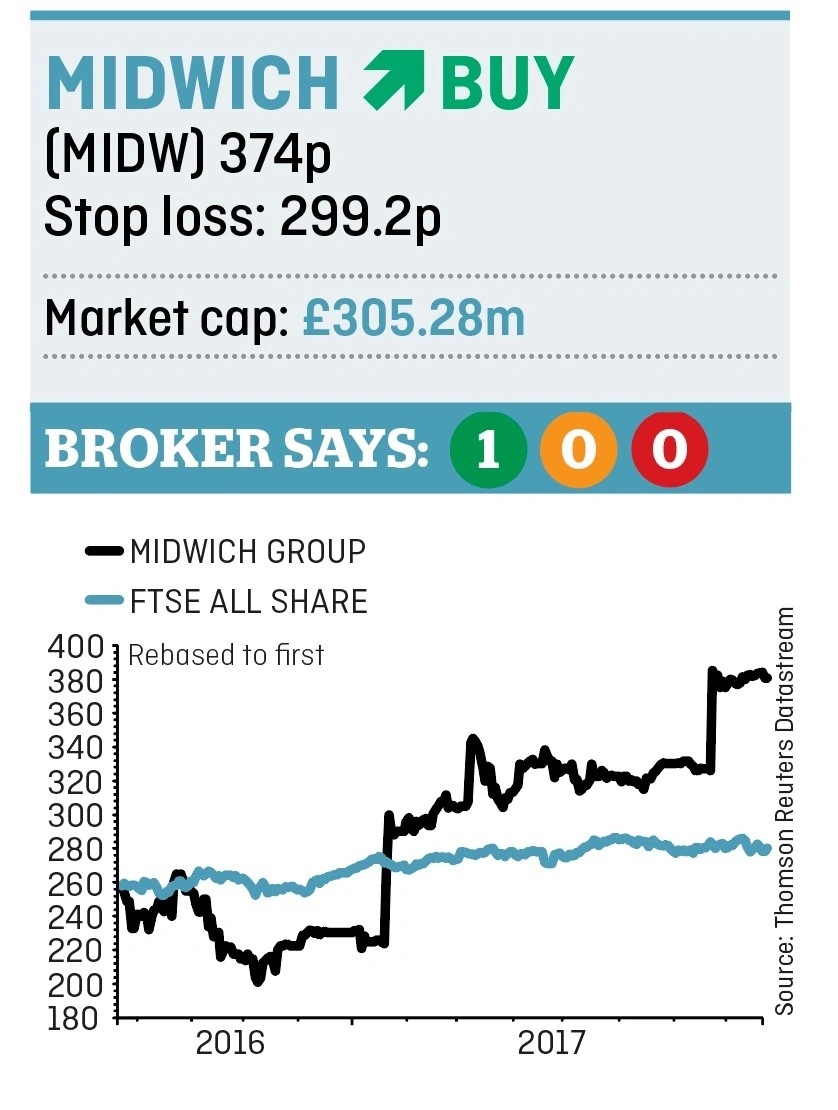

Analysts upgraded their forecasts after Midwich confirmed they will be ‘comfortably ahead’ of expectations in July and research firm Whitman Howard has since increased its target price to 450p implying over a 20% upside.

It also raised its UK revenue forecasts from £270m to £280m. The company is trading on a forecast 2018 price to earnings ratio 16.3-times and pays a dividend yield of 3.3%. This valuation should be more than justified as long as the company can sustain levels

of expansion which have delivered a three year compound annual growth rate in pre-tax profit of 13%.

And with AV technology constantly adapting to serve new purposes, for example fast food outlets allowing you to order a meal using touch screen technology, there should be plenty of scope for growth. First half results are out on 12 September.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.