Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineMarket giants

Size matters. The UK’s largest stocks are typically easy to buy and sell, hold dominant market positions, are often diversified across several different areas and typically generate plenty of cash which can be returned to shareholders through generous dividends.

‘Economies of scale’ also make it cheaper for these market giants to buy in goods and services and allow them to manufacture their own products more efficiently. In this article we look at the 10 largest companies by market value from the FTSE 100 – itself made up of the 100 largest firms on the Main Market.

We also look at the top 10 mid cap stocks from the FTSE 250 and AIM’s 10 largest constituents. From each of these lists we pick out one name which warrants further examination.

FTSE 100 TOP TEN

Many of the largest firms from the FTSE 100 will already be familiar to most investors.

Top of the tree is the Anglo Dutch oil company Royal Dutch Shell (RDSB) which is valued by the market at an eye-watering £176bn. Shell is attempting to reduce its reliance on crude oil, shifting at least some of its focus towards natural gas and, as we discussed in last week’s Editor’s View electricity.

Its rival BP (BP.) is number five on the list. Both companies have high dividend yields of around 7%.

If the market starts to believe these dividends can be maintained the yields should fall or, in other words, their share prices should rise.

In second place is Europe’s largest bank HSBC (HSBA) which has seen its shares enjoy a strong run as its overseas earnings are boosted by the weak pound, a robust balance sheet allows it to return cash to shareholders and the business begins to return to growth after years of contraction.

Tobacco manufacturer British American Tobacco (BATS) has recently suffered a hit after plans were unveiled by the US Food & Drug Administration (FDA) to limit the amount of nicotine in cigarettes.

Mining companies BHP Billiton (BLT) and Rio Tinto (RIO) have been working to increase the efficiency of their operations to cope with volatile commodity prices. Activist investor Elliot Partners has ramped up pressure on BHP to sell its US shale operation, recently increasing its stake in the miner to 5% (16 Aug).

The list is rounded off by pharmaceutical business GlaxoSmithKline (GSK), which in July announced plans to sell 130 non-core products in an attempt to reduce costs, spirits maker Diageo (DGE) and mobile telecoms titan Vodafone (VOD). The latter recently reiterated guidance for 2017 earnings growth of 4% to 8%.

FTSE 100 GIANT IN FOCUS

Unilever (ULVR) £44.31

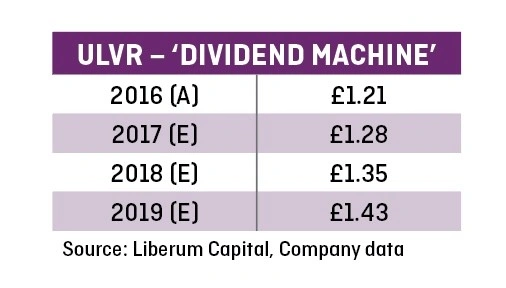

Anglo-Dutch packaged consumer goods giant Unilever (ULVR) is the FTSE 100’s third biggest constituent by market value and while mindful of a demanding rating, we’re staying positive on the PG Tips, Persil, Dove, Hellmann’s, Dollar Shave Club and Ben & Jerry’s brand owner, dubbed a ‘compounding wonder’ and ‘dividend machine’ by revered UK fund manager Nick Train.

Unilever’s share price surged in February following a $143bn takeover offer from Kraft Heinz, the mooted megamerger only serving to highlight the unlocked value in the £56.41bn cap FTSE 100 stalwart.

Paul Polman-led Unilever successfully batted away the bid but was effectively forced into a strategic review (6 Apr). This outlined the acceleration of Unilever’s ‘Connected 4 Growth’ programme and the targeting of a 20% underlying operating margin by 2020, with cost cutting, increased capital returns and fresh acquisition activity of its own also on the menu.

Unilever’s ‘Connected 4 Growth’ programme and review are making the company more agile, both from a cost and organic sales growth perspective.

We’re fans of the fundamentals of Unilever, a unique business on the stockmarket which would leave a gaping hole in portfolios were it to be taken over. Entrenchment in the supply chains of its retailers is the source of Unilever’s wide economic moat, its earnings are reasonably predictable, fantastic brands confer pricing power, while strong cash flows have enabled Unilever to consistently grow its dividend in real terms for decades.

In addition, it has global reach and is at the foothills of its growth in emerging markets with burgeoning ranks of middle class consumers hungry for branded wares.

Following first half results (20 Jul), showing a strong margin performance, growth ahead of its target markets and with management calling a recovery in emerging markets, Berenberg reiterated its ‘buy’ rating on Unilever, upgrading its price target from £48.50 to £50.75.

It is also worth reminding readers that on 9 July, Pablo Zuanic, an analyst at trading firm Susquehanna, argued that a hostile takeover approach from Kraft Heinz is more than 75% likely to happen. He noted the company has made no moves on M&A since its aborted pursuit of Unilever, implying that the FTSE 100 member remains its prime acquisition target.

Zuanic believes Unilever would now cost close to $200bn to buy given the increase in its share price and the likely need for a 20% premium to entice shareholders to sell.

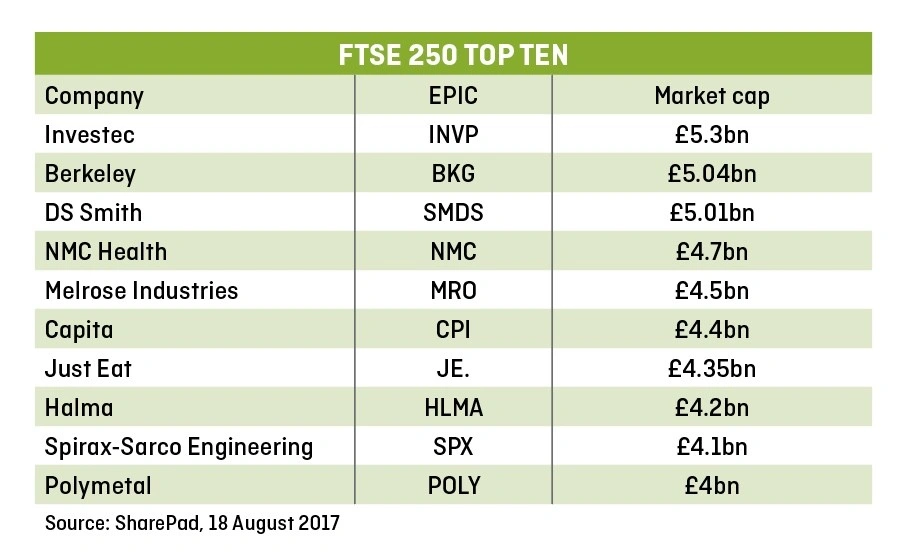

MID CAP TOP TEN

London’s FTSE 250 ‘second liners’ are headed up by Investec (INVP), the £5.3bn specialist bank and asset manager, with London high-end housebuilder Berkeley (BKG) in second spot, a reflection of founder and chairman Tony Pidgley’s legendary ability to call the housing market and reward shareholders with profits growth and copious capital returns.

Third place in the market cap rankings goes to a perhaps less familiar name to investors, recycled packaging supplier DS Smith (SMDS), which has risen through the market cap ranks by delivering strong organic growth with customers across Europe as well as strategically canny acquisitions and consistently strong dividend growth under the stewardship of CEO Miles Roberts since 2010.

‘Although economic conditions remain uncertain, our innovation-led offering, the scale of our operations, and the momentum in the business gives us confidence in further growth and sustainable returns in the years ahead,’ assured Roberts at the time of the display packaging play and progressive dividend payer’s full year results (29 Jun).

Other top 10 constituents of the FTSE 250 include Halma (HLMA), the resilient global maker and seller of equipment demanded by health, safety and environmental rules, as well as valves, pumps and control systems star turn Spirax-Sarco (SPX). NMC Health (NMC), the largest private healthcare provider in the United Arab Emirates (UAE), floated at 210p in 2012 and this Great Ideas selection is now knocking on the door of the FTSE 100, while another high-flying mid cap marvel is the online takeaway ordering system Just Eat (JE.)

MID CAP GIANT IN FOCUS

Just Eat ( JE.) 631.5p

Just Eat operates an online and mobile marketplace for takeaway food, sporting operations in 13 regions and more than 64,000 takeaway restaurants.

Floated on the Main Market in April 2014 at an offer price of 260p, Just Eat’s share price rise reflects stellar growth in an expanding takeaway market, the beating of top-line growth expectations and excitement surrounding scale-building acquisitions. These include France’s ALLORESTO, Menulog, SkipTheDishes and hungryhouse from Delivery Hero, a deal under investigation by the CMA.

Bulls argue Just Eat has years of strong sales growth and strong free cash flow generation to come and UBS has upgraded (17 Aug) the stock from ‘neutral’ to ‘buy’ with a 740p price target, seeing a share price pullback as an attractive entry point for investors.

First half results (27 Jul) triggered a de-rating, investors focusing on an earnings miss, concerns over the margin impact of higher than expected costs from delivery investments and competition from the likes of Deliveroo and UberEATS. Yet full year revenue guidance was upgraded to a £500m-to-£515m range and pre-tax profit before tax powered 46% higher to £49.5m.

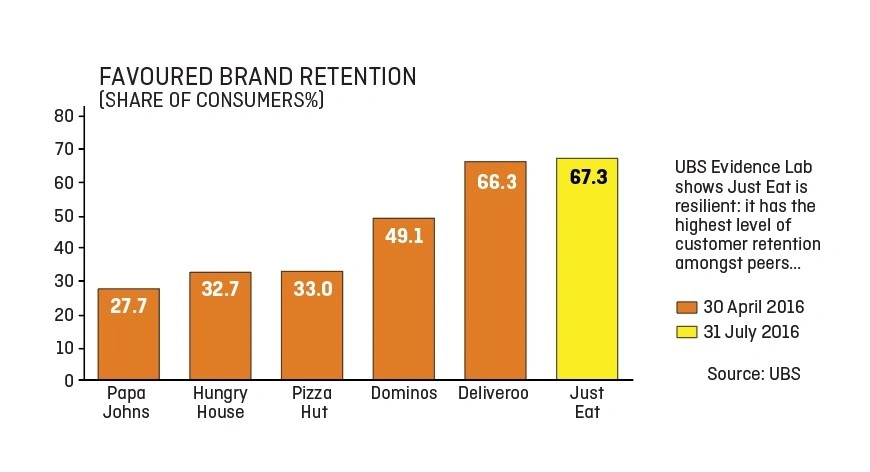

UBS notes Just Eat has been resilient to the emergence of new delivery players and has ‘by far the largest share of loyal customers’. UBS writes: ‘We are not too concerned about delivery investments in the UK, which will remain limited in our view (in the £10- 20m/annum range) and should be more than compensated by operating leverage from 2019 onwards.’

Analysts Chris Grundberg and Hubert Jeaneau argue Just Eat has the highest consumer loyalty amongst competing brands such as Deliveroo and Domino’s, a good base for new CEO Peter Plumb to work with. ‘We see Just Eat’s business model as attractive, with strong network effects, a winner-takes-most market structure and potential for high margins,’ adds UBS.

Berenberg has a ‘buy’ rating and 700p price target for Just Eat, forecasting a top line surge from £376m to £517m for 2017, ahead of £649m and £759m in 2018 and 2019 respectively.

AIM TOP TEN

Our screen of the big beasts of AIM reveals online fashion phenomenon ASOS (ASC:AIM) continues to bestride the junior market like a colossus, despite shares in the fast-fashion seller falling back from January 2014’s £70 peak. Amid Brexit uncertainties and with UK shoppers reining in spend, investors continue to warm to the increasingly international dimensions of this outstanding growth stock and beneficiary of the structural shift to the web.

Potential risks to ASOS’ eye-watering equity rating range from the potential for weakening spend in key markets, adverse moves in currency rates and expansion by competitors. Yet Shares sees ASOS positive sales momentum continuing for a long while supported by ongoing investment in prices and customer proposition as well as a currency tailwind from bowed sterling.

The £4.94bn cap is increasing its differentiation in the rapidly growing online retail channel and has huge potential in an array of overseas markets including North America, investment in a new e-commerce fulfilment centre near Atlanta in the US signalling the scale of its ambitions.

Hot on ASOS’ heels in terms of burgeoning market value are two relative newcomers to AIM’s upper echelons, namely rival online fashion star turn Boohoo.com (BOO:AIM) and premium mixers marvel Fevertree Drinks (FEVR:AIM), the latter having rewarded backers with a meteoric share price rise since its late 2014 IPO, now worth a staggering £2.8bn versus £154m at float.

AIM’s top 10 titans also include litigation finance provider Burford Capital (BUR:AIM), disruptive online estate agent Purplebricks (PURP:AIM) and high-growth construction materials group Breedon (BREE:AIM), whose executive chairman Peter Tom is reassured by the government’s seeming shift from continued austerity towards fiscal stimulus.

Other AIM giants include pharmaceutical and services concern Clinigen (CLIN:AIM) and Hutchison China Meditech (HCM:AIM). Known as ‘Chi-Med’, the China-based biopharmaceutical company focuses on oncology and immunological diseases, has a strong and growing clinical pipeline and is backed by billionaire Li Ka-shing’s CK Hutchison group. (JC)

AIM GIANT IN FOCUS

Phoenix Global Resources (PGR:AIM) 49p

This is a new addition to the list of AIM giants. Commencing trading on 10 August, Phoenix Global Resources (PGR) is a combination of an existing junior market business Andes Energia and PETSA, a vehicle for privately-held Swiss commodities trader Mercuria.

The deal creates an Argentinian oil and gas operation with production of 11,300 barrels of oil equivalent per day (boepd) and total proved and probable reserves of 63m barrels. Andes shareholders have been left with around a quarter of the larger entity.

Notably, Phoenix is chaired by BT (BT.A) and WorldPay (WPG) chairman Michael Rake. Mercuria is likely to have been attracted to a tie-up with Andes due to its material acreage position in the Vaca Muerta shale formation which compliments PETSA’s own interests here.

Located in the Neuquén basin in west Argentina the formation known as Vaca Muerta, or ‘Dead Cow’ in Spanish, is potentially one of the largest shale plays in the world. It is currently one of the few economically producing shale oil formations outside of North America with production of more than 65,000 boepd.

Mercuria is extending borrowing facilities to Phoenix of $160m. These funds will help underpin a work programme aimed at doubling current output by 2021. There are also plans to drill several wells in the Vaca Muerta by the end of 2018. This activity could act as a catalyst for the stock.

The major sticking point is the lack of material free float with Mercuria owning three quarters of the firm and existing Andes shareholders the remainder. This may have contributed to a slow start for the shares.

Other risks include a change in administration from the current business-friendly government in Buenos Aires and the technical challenges associated with shale assets.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.