Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineAre insurers braced for another change to compensation payments?

An update on major legislative changes to the insurance sector has failed to emerge, leaving investors wondering what’s going on.

An announcement had been expected on 3 August regarding industry consultation over how compensation claims are calculated, known as the Ogden discount rate.

Various insurance trade media now report the consultation response won’t come out until later in the year. We now explain what this means for insurance companies and their shareholders.

What is the Ogden rate?

A highly controversial change to the legislation was announced by the Ministry of Justice in February whereby the Ogden rate would move from 2.5% to -0.75% from March.

In simple terms, if a claimant won £1,000 in compensation from an insurer under the old rate, they would receive £975. Under the new rate they would receive £1007.50 as the rate takes into account the investment return the claimant would make on the compensation.

At the time of the original announcement, the Ministry of Justice said it would undertake a consultation to consider whether there was a ‘better or fairer framework’ for claimants and defendants.

It added: ‘The consultation will consider options for reform – including whether the rate should in future be set by an independent body; whether more frequent reviews would improve predictability and certainty for all parties; and whether the methodology is appropriate for the future.’

What do the insurers think?

The Association of British Insurers (ABI) earlier this year warned the rate change would lead to increased costs for insurers. These companies may have to pass the price increases on to consumers in the form of higher premiums.

The ABI in July calculated the average motor premium had subsequently gone up by £48 to £484. ‘Worryingly these increases are unlikely to be the end of the road if reinsurance premiums go up at the end of the year, adding further costs to insurers,’ said ABI director general Huw Evans.

Unfair rate?

The ABI said in May that the rate was unfair as it is tied to index-linked government bonds (aka gilts) which are low yielding at present. ‘It fails to recognise the investment options open to claimants and how they invest their compensation,’ it added.

Talking to Shares last week, Mohammad Khan, head of insurance at PwC, says it’s wrong to assume a risk adverse person (as someone with life-changing injuries may understandably be) would only invest in index-linked gilts.

He believes the insurance industry’s view is that investing in a basket of assets could produce a return much better than -0.75%.

Have insurers started to feel the pain?

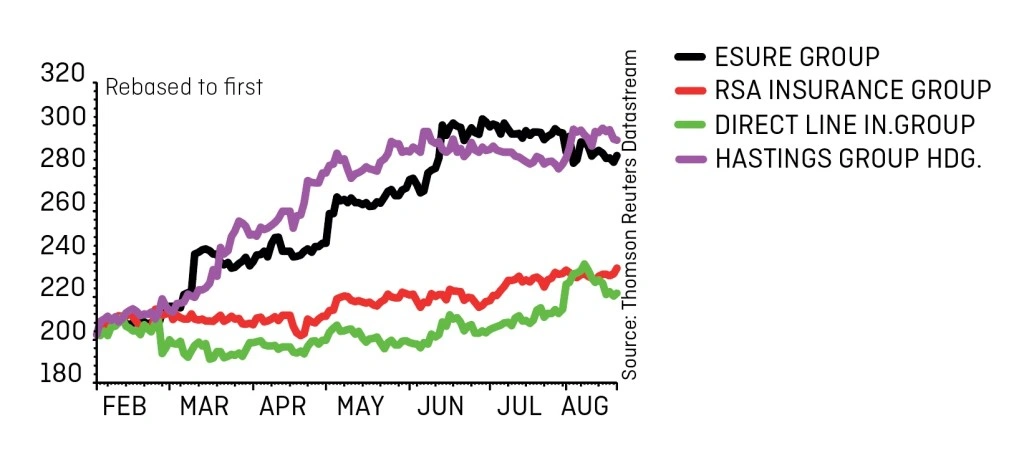

Companies are now starting to report the impact of the Ogden rate change including motor insurer Admiral (ADM), whose share price fell by 8% on releasing its first half results on 16 August. It revealed the rate change would cost the business £150m.

Chief executive David Stevens says ‘most of the adverse impact from the increase in the costs of large injury claims, resulting from the change in the Ogden discount rate, was captured in our 2016 second half result. However, some extra costs carry into 2017’.

Understanding the figures

Consultant EY says that while the adjustment was announced in February, most insurers have already reflected the impact on outstanding claims in their 2016 figures – causing the motor insurance market to report significant underwriting losses.

But PwC’s Khan says there’s a difference between the level at which companies settle a claim and provisions in their accounts. ‘Claims are being settled at an Ogden discount rate of between 0.5% and 1% at the moment. The reason is that as people are waiting for the Government to come out with something, you don’t want to settle too high,’ says Khan.

This may explain some of the discrepancies with first half results among non-life insurers. Some like Direct line (DLG) says the lowering of the Ogden discount rate ‘indicated a lower than expected increase to claims costs’.

However, the company’s gross written premiums are up 9.9% on a year on year basis which it says is a reaction ‘to ongoing claims inflation including the response to the Ogden discount rate change’.

Not as bad as some think?

Esure (ESUR) also played down the impact of the rate change, saying it was ‘not material’. However its reinsurance costs increased by 33% as a result of the rate increase. Esure uses reinsurance to mitigate risk outside of the company’s appetite for claims.

A reinsurer is an insurance company that agrees with another to cover part of the latter’s claims liability. Esure estimates the additional cost of reinsurance equates to £10 per vehicle on a like-for-like basis.

The company has increased its prices across its motor division to mitigate the extra cost of reinsurance.

FTSE 100 heavyweight RSA (RSA) says in their first half results the Ogden discount rate change brought its reserve margin down from 5.5% to 5% which, although lower, is still within its target range.

Positive impact for Hastings

Motor and home insurer Hastings (HSTG) goes as far to say that the change to the rate has benefited the company. Consumers went to price comparison sites to look for better deals on car insurance due to premium increases and it saw a pick-up in new business sales.

Again, this is not to suggest that Hastings emerged totally unscathed from the change in rate. The firm believes that it added between 1% and 1.5% to its loss ratio which is immediate. An increase in pricing takes 12 months to earn through so Ogden’s impact on claims should be negated by the second half of the year.

EY has estimated the overall cost of the Ogden rate change to the insurance industry to be £3.5bn across all lines of business. Khan at PwC says if the Government does do something about the rate, the build-up of reserves could prove very useful for insurance companies’ full year results. The extra capital could be returned to shareholders or used to boost their capital ratios.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.