Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy BAE Systems’ share price slump might be over

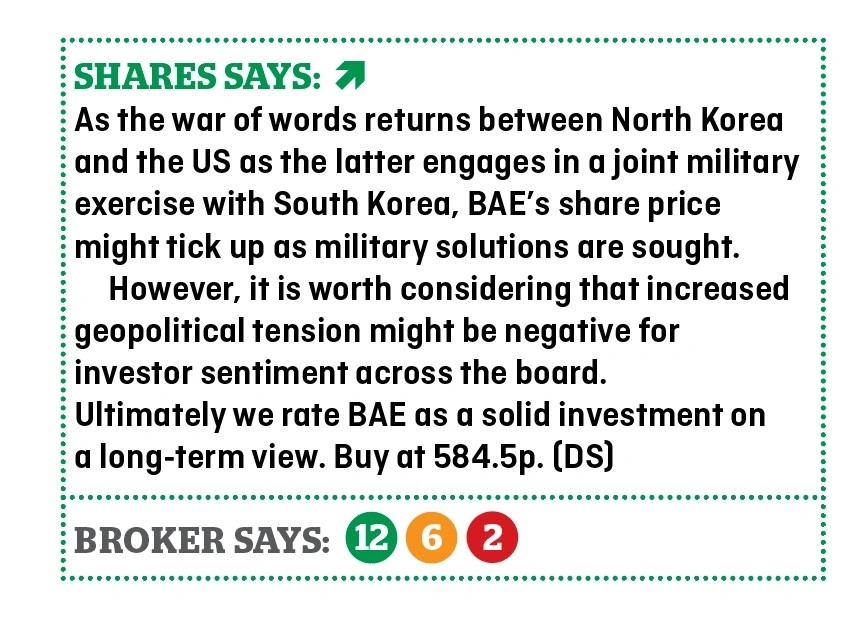

The recent flair up in tensions between North Korea and the US has offered defence company BAE Systems (BA.) some temporary reprieve from its earlier share price slump, helping it to stabilise around the 585p level.

The value of its shares had previously declined from 677p in mid-June to 575p in mid-August, a fall of 15%.

BAE hit a milestone on 17 August, having produced 10% of its production requirement for the fighter jet the F-35 Lightening II.

The F-35 production deal is the world’s largest single defence programme and signals BAE as a true global defence player.

Despite this milestone, BAE is not flavour of the month for everyone. David Perry, analyst at investment bank JP Morgan Cavenove, says ‘(BAE) is not a very interesting stock in our view given lack of growth for at least 18 months’.

Perry is concerned about political and economic uncertainty in the UK and Saudi Arabia as these two markets make up for around 40% of BAE’s sales.

He’s also worried by the company’s £5.9bn pension deficit that requires significant cash funding and impacts any valuation of BAE using enterprise value as a metric.

However, other financial institutions see value in the company. For example, Goldman Sachs added the company to its conviction list on 15 August. The investment bank also raised its target price to 750p from 742p implying 28% upside over the next 12 months.

The company’s first half results (2 Aug) surprised some investors as its free cash flow figure of £70m was much better than expected.

Other analysts see plenty of growth opportunity for BAE and we share this bullish view.

Ben Fidler at Deutsche Bank sees the company’s first half results as a return to earnings growth and believes that the outlook for organic growth remains favourable. This is despite some trail-off in Eurofighter revenues for 2018.

Using Deutsche Bank’s figures, BAE trades on a forecasted 2017 price to earnings ratio of 15.1-times. This is a discount to its peers and also has a dividend yield in the region of 3.7%.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.