Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

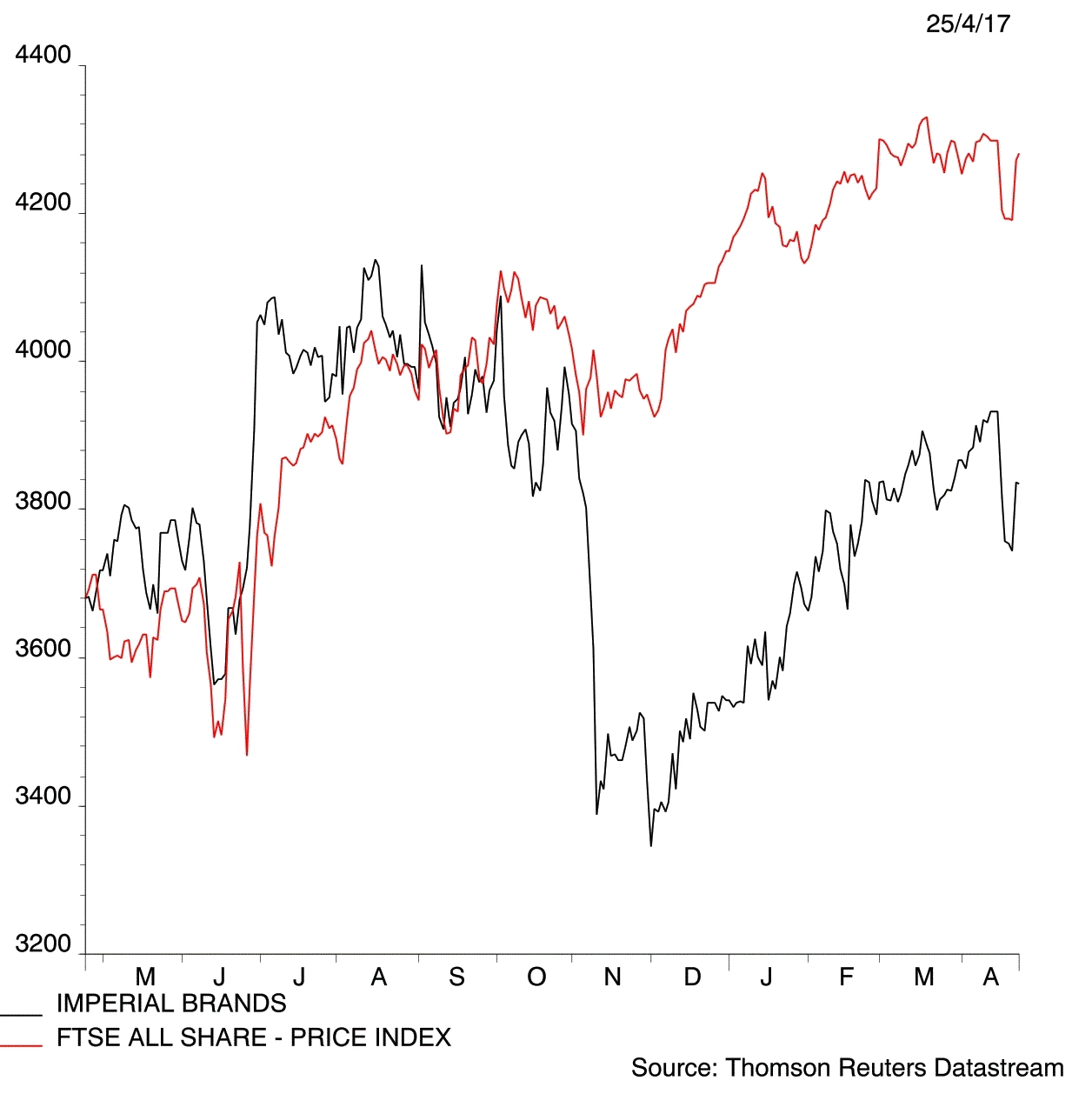

magazineImperial Brands won’t run out of puff

Troubled by the potential for market correction? Then consider investing in high quality mega cap Imperial Brands (IMB) which is committed to growing dividends by at least 10% a year. Shares believes the FTSE 100 company is worth buying ahead of first half results (3 May), which should provide reassurance through yet another dependable dividend increase.

Brand power

The tobacco multinational’s resilient earnings and robust cash flows stem from a strong portfolio of brands which confer pricing power upon the business. These include Davidoff, Gauloises Blondes, West and JPS cigarettes, Rizla papers and Cohiba and Montecristo cigars.

Negatives hanging over the global industry include demand, duties and regulation. The decline in tobacco volumes is expected to continue as smoking rates fall across the world, yet global population growth means smoker numbers won’t be much changed by 2025, according to the World Health Organisation.

Guided by CEO Alison Cooper, Imperial continues to bear down on costs and is investing an extra £300m behind its brands and key markets in 2017 to drive medium term sales growth.

Imperial has guided (30 Mar) towards a strong uptick in sales and earnings per share for the half to 31 March despite a deterioration in industry volumes. These results will show a boost as overseas earnings are translated into weak sterling.

Growth puff?

Imperial Brands recently inked (11 Jan) a joint venture to drive the growth of West and Davidoff in China, the world’s biggest tobacco market. This builds on 2015’s acquisition of a number of US cigarette brands, including Winston and Kool and the international rights to the blu e-vapour brand, in a deal which transformed Imperial’s presence in the world’s most profitable tobacco market outside China.

M&A optionality

For the financial year to September 2017, consensus earnings and dividend per share estimates are currently pitched at 272.91p (2016: 249.6p) and 171.1p (2016: 155.2p) respectively, rising to 284.83p of earnings and a 188.28p shareholder reward for 2018. Based on these latter forecasts, Imperial Brands trades on a prospective PE ratio of 13.5 times and offers an attractive 4.9% dividend yield.

We view this as reasonably undemanding for such a high quality stock. The merger between British American Tobacco (BATS) and Reynolds American has reignited speculation about further industry consolidation. Imperial Brands is the outstanding industry bid target, with Japan Tobacco International considered the logical acquirer. (JC)

IMPERIAL BRANDS (IMB) £38.33

Stop loss: £30.66

Market value: £35.9bn

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- Energy in a spin over plans for power price cap

- Wincanton joins list of potential takeover targets

- Virgin Money shrugs off unsecured debt concerns

- Sportech easier to swallow after pools sale

- Tritax investors offered cheap shares

- Spanking for Sports Direct

- Robotics stocks could get boost from Trump policies

- Whitbread burnt by Costa sales decline

Editor's View

Feature

Great Ideas Update

Investment Trusts

Larger Companies

Money Matters

Smaller Companies

Story In Numbers

- ZPG could tap £3bn revenue opportunity

- £1,470: Moneysupermarket saves you money but is it a good investment?

- 71 month high: French business activity

- FTSE 350 sectors, best performers

- Commodity prices this year selection

- £150m: Debenhams’ costly to-do list

- $5.4trn: Record ETF flows boost world’s largest asset manager

- £100bn: Search advertising market is booming