Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThe big switch: is it time to sell FTSE 100 and buy FTSE 250?

Markets are driven by sentiment and identifying when sentiment is shifting can help you spot investment opportunities.

For the last 10 months four key interlinked factors have held sway: Brexit, sterling weakness, Donald Trump becoming US president and the return of inflation.

The surprise news of a UK general election on 8 June changes the story. We believe there is now the start of a big switch in investor interest from the overseas-focused FTSE 100 into the more domestic names on the FTSE 250.

GAME CHANGER

Prime Minister Theresa May’s shock announcement of a snap election is, in the words of Deutsche Bank’s currency team, a ‘game-changer’ for sterling.

The basic argument runs as follows. The Conservatives’ 21-point lead in the polls could translate into a big increase in their current House of Commons majority of 17 seats once the general election result is published on 9 June.

Some projections suggest May could command a majority of up to 100 seats which would give her a stronger mandate and greater leeway to negotiate a Brexit deal.

Since she made her announcement shortly after 11am on 18 April sterling has gone from around $1.25 against the dollar to more than $1.28 – a big move in currency terms. However, very weak monthly data on UK retail sales on 21 April has subsequently taken some shine off the pound.

This election-driven move in the foreign exchange markets has coincided with a significant reversal for the FTSE 100 which has now wiped out any year-to-date gains from the index.

The recovery in sterling hits the value of profits earned overseas when translated back into pounds, and around 70% of FTSE 100 earnings come from abroad. However, as we discuss later in this article, currency movements are not the only reasons behind the FTSE 100’s recent collapse.

MID CAP COMEBACK

The big question for investors is whether now is the opportune moment to load up on the more domestic-focused names in the FTSE 250.

While mid-caps underperformed in the wake of last June’s Brexit vote, the FTSE 250 index quickly recovered and has been on a strong run so far this year.

ECONOMY NOT AS BAD AS FEARED

Many market commentators inmediately after the Brexit vote expected a big hit to economic growth in the UK. That hasn’t really happened. In fact, we’re actually seeing upgrades. That’s clearly positive for FTSE 250 stocks which principally generate earnings from the UK.

For example, The International Monetary Fund is forecasting the UK economy will grow by 2% in 2017 compared with a previous projection of 1.5% just three months ago.

Observers reckon May could have greater room for compromise on Brexit after June’s vote, thereby reducing any negative impact on economic growth.

Crucially it also pushes the timing of the next election from 2020 to 2022, leaving space for a more orderly transition period as the UK leaves the EU.

As analysts at investment bank Credit Suisse note: ‘If Theresa May wins it would be a powerful mandate for her and her type of Brexit, which in turn would limit the ability of either the pro-EU or furiously anti-EU sects of the Conservative party to derail her Brexit.

‘This could mean that it might be slightly easier for Theresa May to give some concessions in the Brexit negotiations and possibly deliver a softer Brexit than the one she has outlined so far.’

Switching into domestic mid-caps

Between the Brexit vote in June 2016 and the announcement on 18 April 2017 of a UK general election, the FTSE 250 slightly lagged behind the FTSE 100. The mid-caps were up 13% against a 16% advance for their blue chip counterparts.

Since the election news the FTSE 100 has eased back slightly and the FTSE 250 has held firm.

The FTSE 250 has a more domestic bias than the FTSE 100 but does derive around 50% of its earnings from outside the UK.

City Index research director Kathleen Brooks notes the FTSE 250 has actually been outperforming the FTSE 100, particularly since the beginning of February, and that its outperformance may have become ‘stretched’.

However, certain sectors like retail, housebuilding, travel and leisure are tightly focused on the UK and they have been among the key underperformers since the Brexit vote.

This is largely down to a combination of the weak pound pushing up inflation and the wider pressure from a loss of consumer confidence, reflected in retail sales recording the biggest fall in seven years in March. For travel firms, the slump in sterling has also made overseas trips more expensive for British holidaymakers.

UK DOMESTICS ON COMEBACK TRAIL

If the pound reverses the negative trend seen since the EU referendum and the UK’s economic prospects brighten then some of these stocks could be attractive.

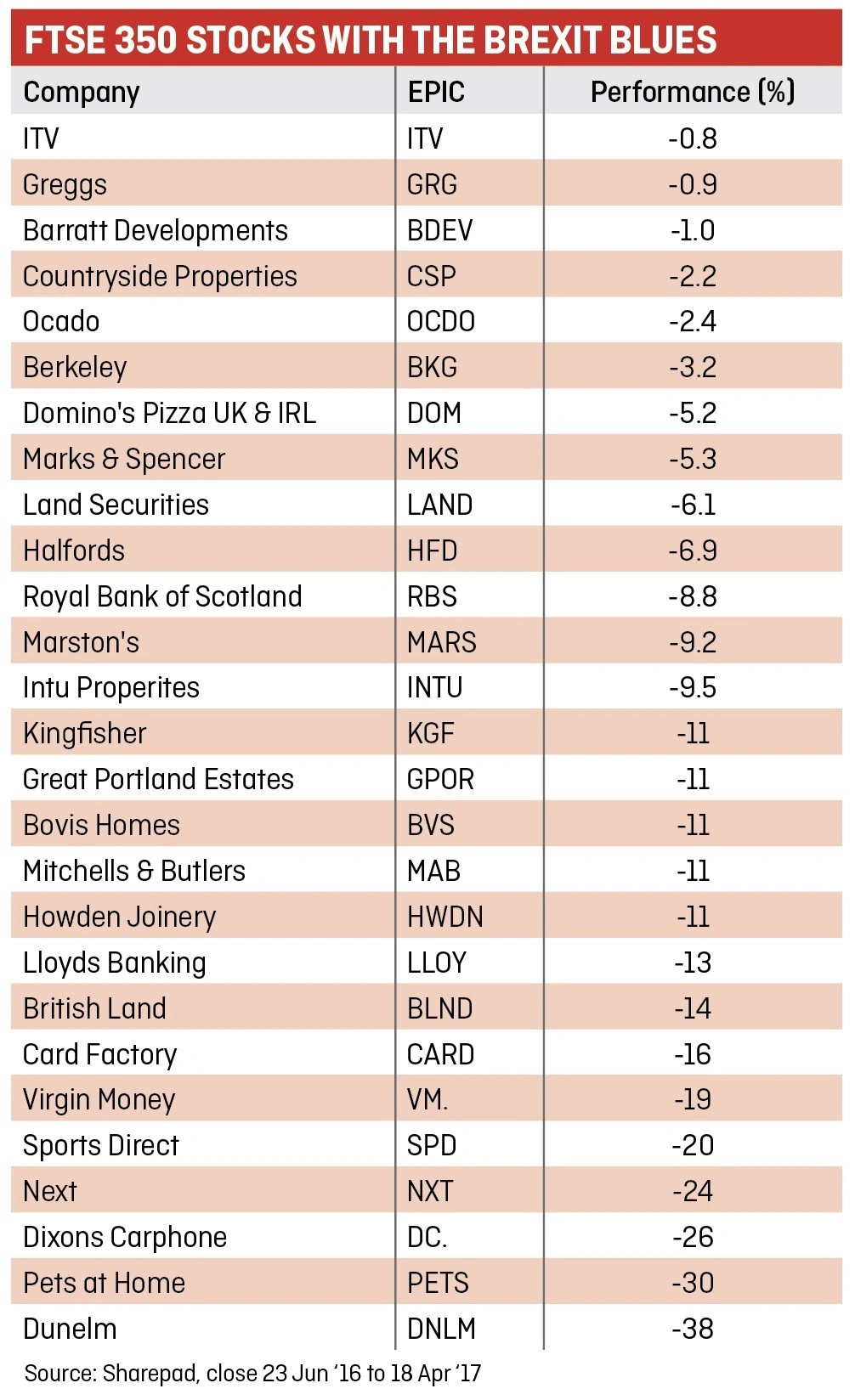

The accompanying table shows domestic-facing companies which were in negative territory for the period covering the Brexit vote and up until Theresa May’s announcement of a snap election.

From this list, we particularly like greetings card retailer Card Factory (CARD) and kitchens seller Howden Joinery (HWDN), both of which are already constituents of our Great Ideas portfolio.

Card Factory offers excellent cash generation, a generous dividend and is a beneficiary of downsizing by its competition – most notably Clintons.

Staying in the retail sector, Liberum sees high street electronics shop Dixons Carphone (DC.) as a structural winner noting that ‘through its leading multi-channel, specialist retail position and deep supplier relationships it is gaining share faster than any competitor’.

Liberum’s 430p price target for Dixons implies upside of more than 30% from the current 325.1p share price.

The investment bank is more negative on another underperformer, Pets at Home (PETS) which it argues faces intensifying competition from online and store-based specialists as well as discounters and supermarkets.

We are unconvinced by the turnaround efforts at department store Debenhams (DEB) and the jury is still out on online groceries business Ocado (OCDO) given the competitive threats it is facing, notably from Amazon’s newly launched rival service.

STANDING ON FIRM FOUNDATIONS

Like the overall economy, previous forecasts for a property crash have so far proved wrong. That has seen investors continue to be supportive of housebuilders.

Investment bank Jefferies comments: ‘In our mind, the stage is set for a golden period for the UK housebuilders with demand outstripping supply (placing upward pressure on the price of homes) and increased land supply where the country most needs homes (placing downward pressure on the price of land).’

On this basis Bovis Homes (BVS), which recently walked away from takeover talks and appointed industry veteran Greg Fitzgerald to lead a turnaround of its fortunes, could be an interesting stock for investors to research.

On the leisure side, analysts at investment bank Berenberg like pubs operator Marston’s (MAR) noting that through disposals and a roll-out of new-build managed pubs, the company has ‘materially improved the quality of its estate’ and the market is yet to price this in.

Marston’s trades on a price-to-earnings ratio of 9.3 times, based on a forecast 15.1p earnings per share for the year to September 2018.

What to think about

Don’t rush in blindly. Investors looking to play a rebound for UK domestic-facing mid-caps should still tread carefully as politics and the currency markets are often volatile.

‘There could be further upside if markets get what they want from this election, namely a strong Conservative majority allowing Theresa May to pursue a softer Brexit with a longer, more market-friendly transitional agreement with the EU post-2019,’ says Neil Wilson at ETX Capital.

As well as being the most ‘market-friendly’ outcome it also seems the most credible one given the Conservative’s dominance in the polls.

But, as Brexit and Donald Trump’s election as US president have demonstrated, polls can be wrong.

There seem to be two other possible ways the election could play out:

Theresa May failing to materially increase her majority after the election would be treated as a disappointment by the market.

The much more remote possibility of May losing office and being replaced by a coalition government would be a severe market shock in the vein of the Brexit vote itself.

Where next for the FTSE 100?

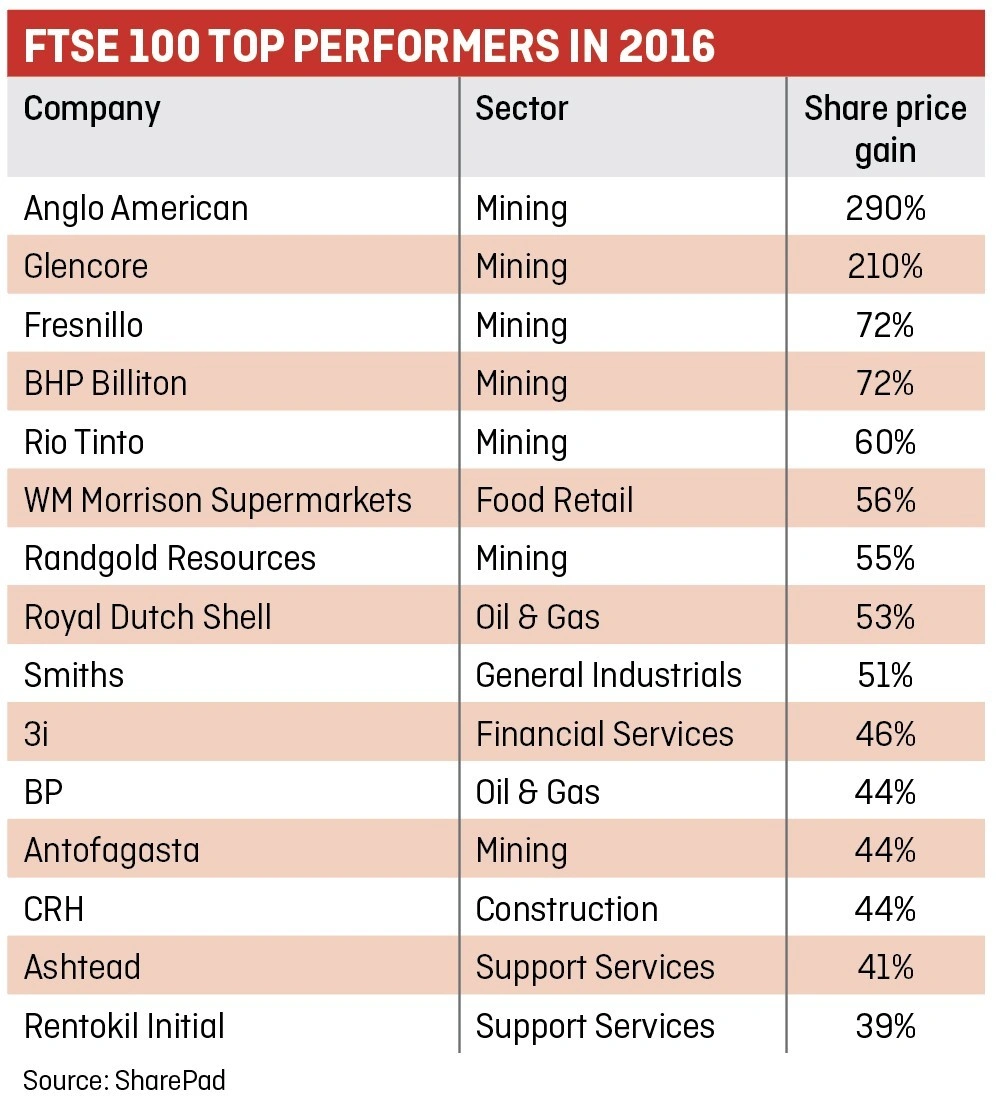

The FTSE 100 had a very good year in 2016, rising by 14% in value. That is nearly four times higher than the 3.7% gain from the FTSE 250 index, according to data from SharePad.

Currencies are the principle reason behind this disparity. The dollar appreciated by 19% versus sterling in 2016. It also strengthened against many other major currencies including the euro (+3.3%).

TAILWINDS… BUT FOR HOW LONG?

Nearly all the top performing FTSE 100 stocks in 2016 generated a large chunk of their revenue in dollars. They’ve enjoyed a significant tailwind from favourable foreign exchange rates.

Apart from the miners, most of these companies report their financial results in sterling, so there has been a translation boost to their earnings. That’s naturally boosted their share price, too.

The miners have still benefited, nonetheless; all their shares are priced in sterling – so there has also been a translational boost when comparing their market value against earnings strength.

TREND REVERSAL

The dollar has fallen approximately 4% against sterling so far in 2017, implying that the translational boost is fading away.

As mentioned earlier in this article, news of the snap general election in the UK has helped to further strengthen the pound. That’s why many of last year’s top performers (boosted by the stronger dollar) have seen this year their share prices grind to a halt (restrained by the weaker dollar).

DON’T AUTOMATICALLY SELL ALL YOUR FTSE 100 STOCKS

The big question now is whether you should take profit in all stocks that have enjoyed a translational boost over the past year.

To answer that question you need to consider the following:

1. A strong dollar isn’t the only reason why certain stocks rallied in 2016

2. Some of the companies who enjoyed a dollar boost could also benefit from a stronger pound

3. How are these companies performing if you look at constant currency rates, not actual rates?

Let’s address those points one by one.

1. OTHER FACTORS AT PLAY

The FTSE 100 hit the headlines last week when the pound rallied on the election news (18 April). Most people attributed the blue chip index’s decline to the currency movement.

What most commentators failed to explain was that the FTSE 100 was already trading down that day BEFORE the election news was out – principally as a result of commodity price weakness.

You have to remember that the FTSE 100 is a market cap weighted index. A stock that accounts for 10% of the index, for example, will have a more pronounced influence on the FTSE 100’s pricing than something that only accounts for 0.1%.

Oil, gas and mining companies mostly sit at the top end of the FTSE 100 – so commodity price movements can cause the overall index to move as these relate to products being sold by the resource firms.

A large fall in the price of iron ore was the principal cause of the FTSE 100’s initial decline on the day of the election announcement. Glencore (GLEN), BHP Billiton (BLT) and Rio Tinto (RIO) all generate earnings from that commodity and they are all in the top 15 largest stocks by weighting in the blue chip index.

2. LOOK FOR CURRENCY CUSHION

A few stocks which benefited from US dollar tailwinds last year also do business in the UK – so you could argue that dollar weakness this year could be cushioned by gains in sterling and potential movements in other currencies.

Construction equipment firm Ashtead (AHT) only generates about 10% of its earnings from the UK, so we don’t think any sterling recovery will really make a difference to its share price. Investors pretty much assume it is a pure play on US infrastructure activity.

In contrast, distributor Bunzl (BNZL) generates about 40% of sales from outside North America. It says currency movements helped to boost group revenue by 10% in 2016.

About 15% of Bunzl’s revenue comes from the UK and a further 18% from mainland Europe. That should be big enough to provide a meaningful cushion to offset some of the translational weakness should the dollar (and the euro) continue to fall against sterling.

3. LOOK AT THE CONSTANT CURRENCY NUMBERS

Over the past few months we’ve tried to focus on constant currency numbers when reporting on corporate accounts in order to measure the true health of a business.

Currency movements tend to iron themselves out over time, so you should never expect one year’s exceptional forex-led uplift in earnings to be repeated year in, year out.

Although not a FTSE 100 stock, British manufacturing company Rotork (ROR) is a great example of why it pays to study the numbers.

It reported an 8% rise in revenue in 2016 to £590.1m and a 10.6% decline in pre-tax profit to £91.1m. That’s based on actual exchange rates. Take a closer look and you’ll see currency tailwinds inflated its results by 10%.

The outcome is very different when you strip out an acquisition and run the numbers on a constant currency basis. Rotork’s revenue actually fell 8% and it suffered a 20.5% drop in pre-tax profit. The business is therefore not as healthy as the headline figures would suggest.

WHAT SHOULD I DO NEXT?

We’d take profit on FTSE 100 companies considered to be ‘obvious’ beneficiaries of increased US infrastructure investment such as Ashtead and CRH (CRH).

Investors have been over-optimistic with regards to the opportunity with many people assuming an immediate boost to earnings. The reality is that Trump’s spending plan will take time to realise… if at all.

As for the miners, you’d have to look at valuations and take a view on individual commodities. Analysts say Rio Tinto is among the miners most at risk near-term given its dominance in iron ore where the outlook is negative.

Silver and gold producer Fresnillo (FRES) at £15.18 is trading on 1.8 times net asset value, as based on forecasts for 2018 by stockbroker Numis. That’s at the upper end of where we would expect decent gold miners to trade in a bullish commodity price environment.

We’re only in the early stages of a commodity price recovery, certainly nowhere near prime conditions where you could justify gold miners trading on up to 2.0 times NAV.

If you don’t want to sell any of your FTSE 100 holdings, you may wish to consider hedging your position through buying a short ETF on the index. It would profit from any decline in the value of the FTSE 100. (TS/DC)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- Energy in a spin over plans for power price cap

- Virgin Money shrugs off unsecured debt concerns

- Wincanton joins list of potential takeover targets

- Sportech easier to swallow after pools sale

- Tritax investors offered cheap shares

- Spanking for Sports Direct

- Robotics stocks could get boost from Trump policies

- Whitbread burnt by Costa sales decline

Editor's View

Feature

Great Ideas Update

Investment Trusts

Larger Companies

Money Matters

Smaller Companies

Story In Numbers

- ZPG could tap £3bn revenue opportunity

- £1,470: Moneysupermarket saves you money but is it a good investment?

- 71 month high: French business activity

- FTSE 350 sectors, best performers

- Commodity prices this year selection

- £150m: Debenhams’ costly to-do list

- $5.4trn: Record ETF flows boost world’s largest asset manager

- £100bn: Search advertising market is booming