Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineKeep buying JD Sports for overseas success

Record full year results (11 Apr) from JD Sports Fashion (JD.) confirmed a third consecutive year of double digit store like-for-like growth from the core Sports Fashion business. Can it keep going?

Toughening comparatives suggest this breathless same-store growth rate will be hard to sustain. There are also concerns about high levels of personal debt among UK consumers which could eventually curb retail spending.

We still rate the stock as a ‘buy’ because the branded sportswear retailer’s global growth potential is immense.

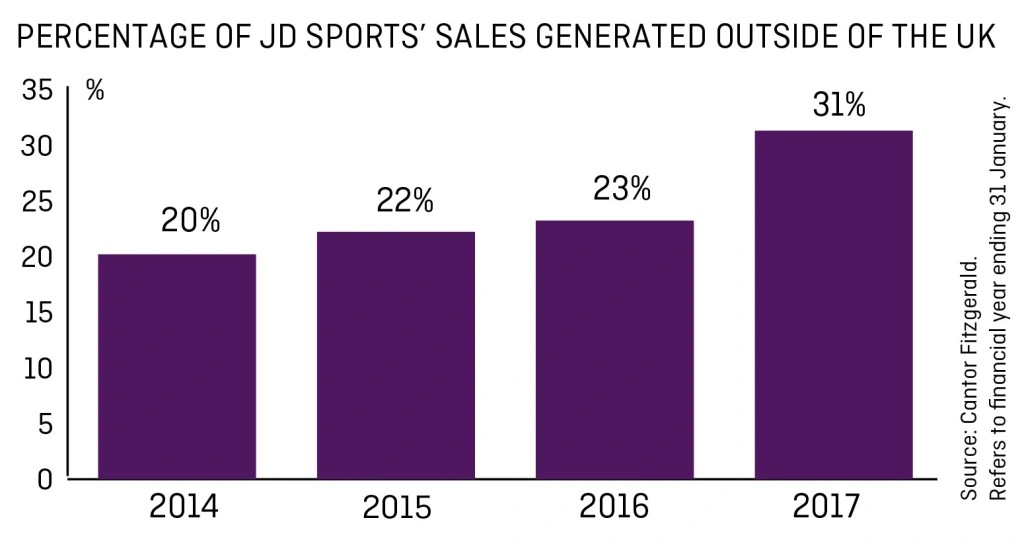

In particular, we believe the market’s focus will increasingly be on its international business which is in excellent health.

JD Sports now generates approximately 30% of its business from outside of the UK, up from 23% a year ago and a mere 5% seven years ago.

‘Whilst the core UK Sports Fashion business remains the engine room of the business we are encouraged to see significant growth in other parts of the group,’ says Cantor Fitzgerald analyst Mark Photiades.

‘JD is now fully recognised by the leading sportswear brands as a major global partner and player and the opportunity for further international growth in Europe and beyond is significant.’

Clearly differentiated from rival Sports Direct International (SPD), executive chairman Peter Cowgill has successfully turned JD Sports into an important retailer for major international brands, principally Nike and Adidas.

Cantor forecasts 21.5p earnings per share for the year to January 2018. Based on the latest share price of 447.9p, JD trades on a price to earnings (PE) multiple of 20.8 times. We believe it deserves such a premium rating, given rapid growth and ongoing expansion potential.

‘The valuation, in our view, still does not reflect the true value of the JD concept, which is trading in a booming segment of the retail market,’ says Photiades.

‘The JD format has a great track record growing operating profits by 44% per year over the last three years. It is clearly differentiated from its closest UK competitor, has the support of the leading sports brands in sports fashion and has significant potential to be developed overseas, where it now has clear momentum.’

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- Energy in a spin over plans for power price cap

- Wincanton joins list of potential takeover targets

- Virgin Money shrugs off unsecured debt concerns

- Sportech easier to swallow after pools sale

- Tritax investors offered cheap shares

- Spanking for Sports Direct

- Robotics stocks could get boost from Trump policies

- Whitbread burnt by Costa sales decline

Editor's View

Feature

Great Ideas Update

Investment Trusts

Larger Companies

Money Matters

Smaller Companies

Story In Numbers

- ZPG could tap £3bn revenue opportunity

- £1,470: Moneysupermarket saves you money but is it a good investment?

- 71 month high: French business activity

- FTSE 350 sectors, best performers

- Commodity prices this year selection

- £150m: Debenhams’ costly to-do list

- $5.4trn: Record ETF flows boost world’s largest asset manager

- £100bn: Search advertising market is booming