Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineInvestment trusts that pay more and more dividends every year

Investment trusts can be ideal products for anyone seeking to enjoy compounding benefits from reinvesting dividends.

They are allowed to stash away up to 15% of income every year in a pot called ‘revenue reserves’. This rainy-day money can help them to keep paying dividends even if market conditions are bleak and there is temporarily a lower income from their underlying holdings.

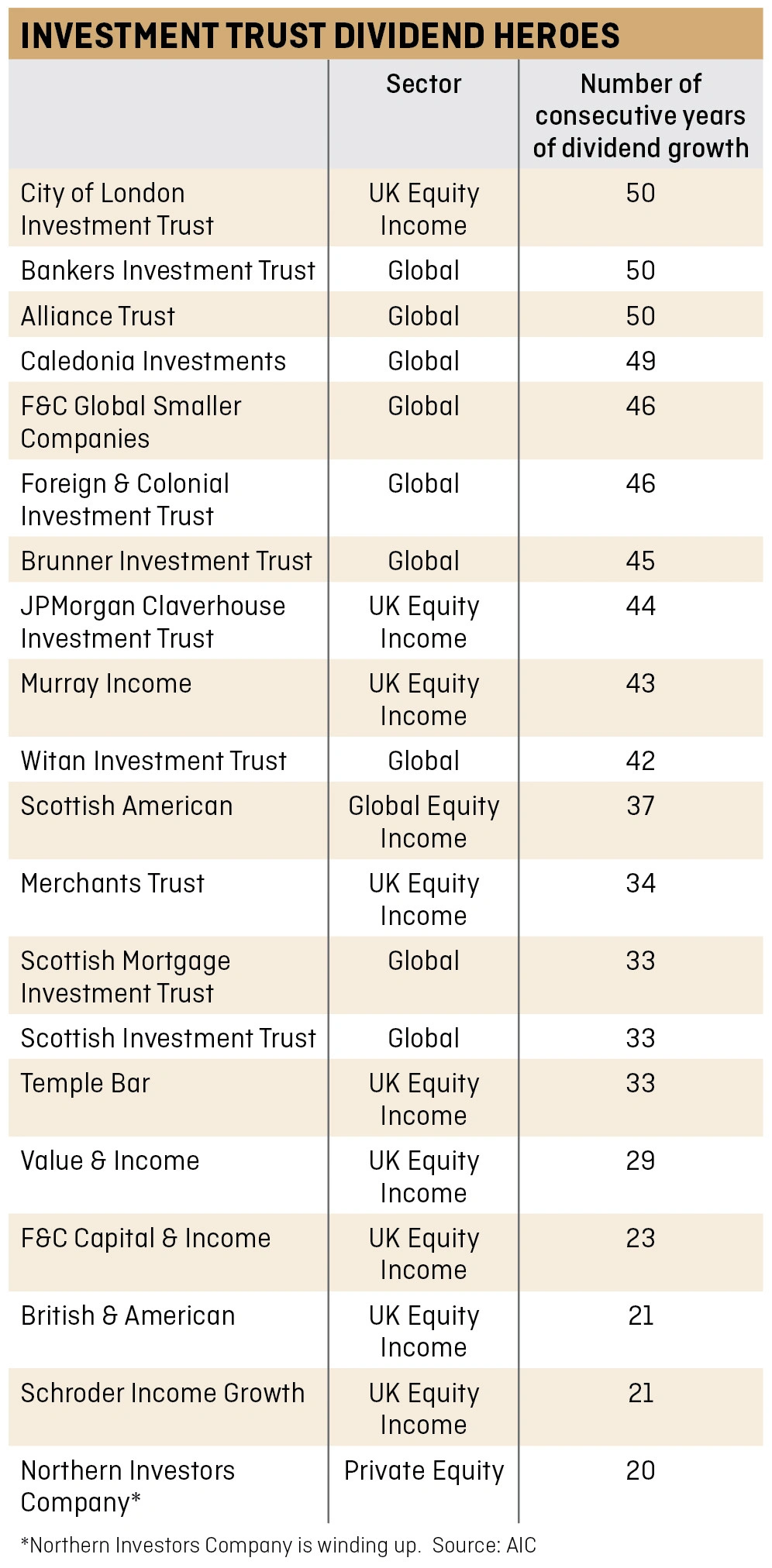

Twenty investment trusts have raised their dividend every year for at least the past 20 years in a row, according to the Association of Investment Companies (AIC) which labels them as ‘dividend heroes’.

Don’t be put off by many of these trusts only having dividend yields in the region of 2% to 3%. The real attraction is their dividend growth, in our view.

Let’s now take a look at seven investment trusts on the AIC’s dividend heroes list.

Bankers Investment Trust (BNKR) 768p

Discount to net asset value: 4.8%

Number of consecutive years of dividend growth: 50

Bankers’ fund manager Alex Crooke says a careful focus on investing in companies capable of growing their dividends over time has meant that even through the market crash in 2008, Bankers Investment Trust has avoided regularly dipping into reserves to keep growing its own dividends to shareholders.

‘Over the last 10 years Bankers has only had to dip into reserves once, in 2011, when it was decided to increase investment into Japanese equities,’ says Crooke. ‘It was judged that the potential total return meant a short term reduction in dividends would be offset by higher capital returns. A year later dividends were once again covered by earnings.’

One of Crooke’s favourite stocks is Cranswick (CWK), a supplier of pork and meat products to UK food retailers. ‘They have increased their dividend every year since 1991 and have a great record of using internally generated cash to fund growth and acquisitions.’

Brunner Investment Trust (BUT) 671p

Discount to net asset value: 14.5%

Number of consecutive years of dividend growth: 45

Allianz-managed dividend hero Brunner Investment Trust is a concentrated global equity portfolio with a focus on high quality growth and attractive valuations. Manager Lucy Macdonald has reduced the trust’s UK exposure to have a greater portion of income derived overseas.

‘I look for a company with good growth potential, favourable industry structure and profitability, management with proven ability to allocate capital effectively and, preferably, a valuation opportunity,’ says Macdonald.

‘The technology sector has growth and an increasing willingness to distribute via dividends, such as Microsoft and Apple. The financial sector, after a period of enforced restraint by regulators post financial crisis, is now a recovering source of income, particularly in the US,’ she adds.

‘Geographically Europe, Asia and emerging markets have good yield potential. We have exposure to income from all regions via stocks like Schneider, Jiangsu Expressway and Brazilian infrastructure company CCR.’

City of London Investment Trust (CTY) 417.5p

Premium to net asset value: 1.4%

Number of consecutive years of dividend growth: 50

Managed by Job Curtis since 1991, the trust has dipped into its revenue reserves in seven out of the last 25 years to grow the dividend, demonstrating the advantages of the closed-ended structure over open-ended funds in terms of income.

Curtis looks for a combination of an above average yield and growth in his investments. The fund manager likes strong balance sheets which he believes are key to ‘avoiding the disasters’ during a downturn.

Favoured picks include classic defensive British American Tobacco (BATS), the cash-generative, dividend paying tobacco titan being ‘the most successful stock in my career’. The trust has stakes in such stocks as GlaxoSmithKline (GSK), Royal Dutch Shell (RDSB). Curtis is also keen to highlight the dividend growth prospects for the UK housebuilding sector, owning both Taylor Wimpey (TW.) and Persimmon (PSN).

JPMorgan Claverhouse (JCH) 674.5p

Discount to net asset value: 5.3%

Number of consecutive years of dividend growth: 44

Dividend-paying stalwart JPMorgan Claverhouse has a focused portfolio of 62 stocks and looks for value, momentum

and quality in the UK equities space.

Co-manager William Meadon says the ideal stock would have all three characteristics. ‘It would be cheap, have good momentum of both earnings (profit) and share price, and have a strong balance sheet. There are very few of these stocks, so when we find them we buy a lot.’

He says Ashtead (AHT), Micro Focus (MCRO) and Imperial Brands (IMB) currently meet all three criteria.

Meadon cites Fevertree Drinks (FEVR:AIM) as ‘an out and out momentum stock with great share and earnings momentum’. He points to Taylor Wimpey and other quality UK housebuilders having cash rich balance sheets and says insurer Aviva (AV.) looks very cheap.

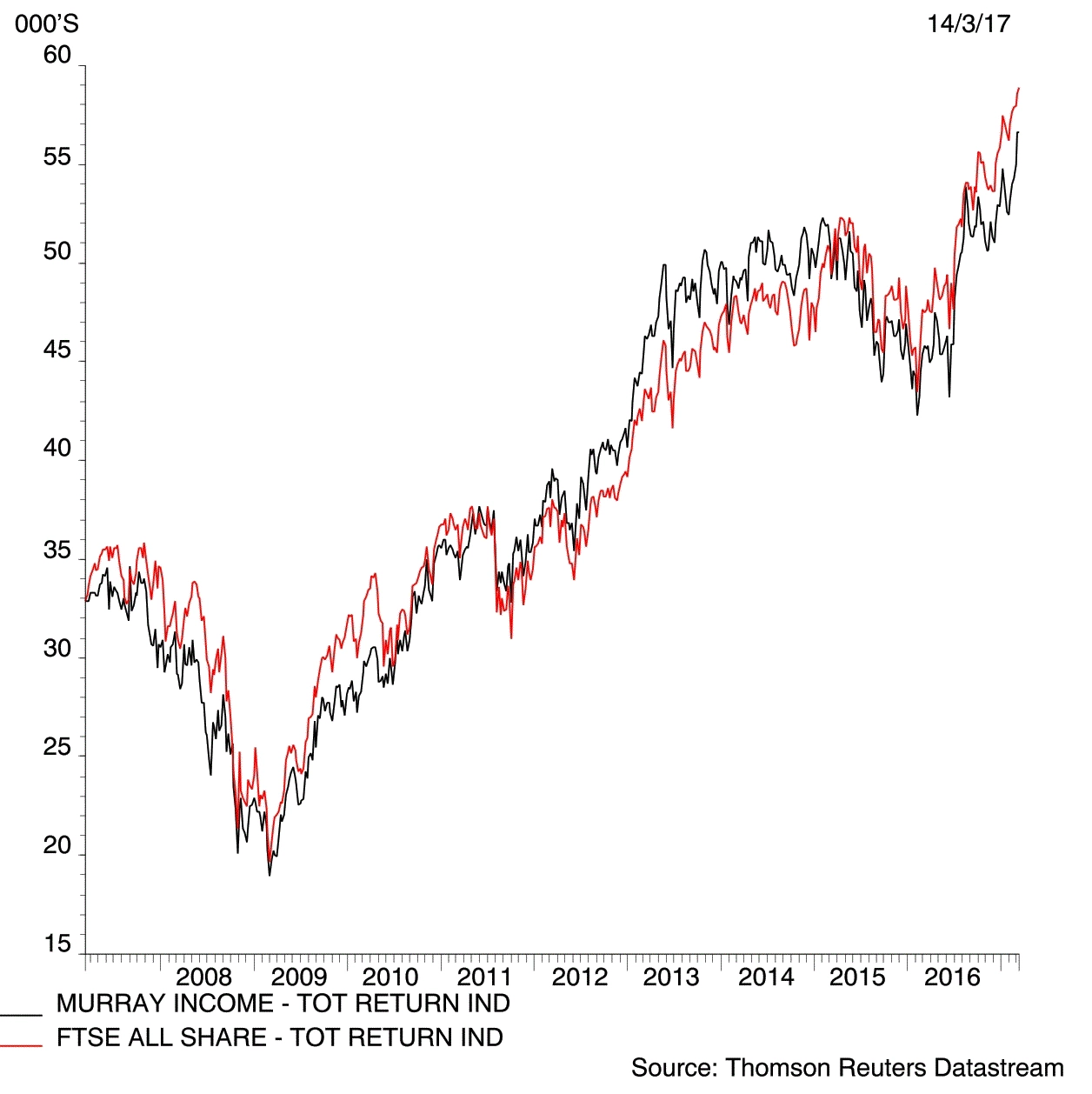

Murray Income Trust (MUT) 771.5p

Discount to net asset value: 8.4%

Number of consecutive years of dividend growth: 43

Murray Income focuses on fundamentals such as a strong business model, experienced management team and conservative balance sheet. ‘It aims to invest in good quality companies with attractive dividend yields that are capable of growing their earnings and dividends over the long term,’ says manager Charles Luke.

Over the last decade, the trust has accessed its revenue reserve only twice. Its favourite source of income is the pharmaceutical sector with holdings including GlaxoSmithKline, AstraZeneca (AZN) and Roche.

Scottish American Investment Company (SCAM) 342p

Premium to net asset value: 3.6%

Number of consecutive years of dividend growth: 37

Baillie Gifford-managed Scottish American Investment Company – also known as ‘SAINTS’ – aims to grow the dividend at a faster rate than inflation.

Global equities are its focus, although investments are also made in bonds, property and other asset types.

‘We focus on identifying exceptional companies which will persistently deliver both robust cash flow growth and dependable dividends,’ says manager Dominic Neary.

Neary’s favoured stocks include TSMC, ‘the Taiwanese semiconductor manufacturer, which has built up the leading position in making chips for a huge range of end-markets.

‘We can see demand for silicon rising enormously over the next five to 10 years as the number of devices proliferates – and TSMC is now one of the only businesses who have the scale and skills to meet this growth in demand.’

A recent portfolio addition is cash-generative dividend payer Kering, a luxury goods business which owns Gucci and many other brands. ‘We see two big drivers of growth; an improvement in the performance of Gucci and Puma under revitalised creative teams, and continued growth from the collection of smaller luxury brands the group has incubated over many years.’

Witan Investment Trust (WTAN) 953.5p

Discount to net asset value: 4.8%

Number of consecutive years of dividend growth: 42

Witan Investment Trust uses a multi-manager approach to deliver long-term growth in income and capital for shareholders. Chief executive Andrew Bell comments: ‘Over the past 25 years, we have only twice paid dividends that were higher than the earnings for that year.

‘The first was 1999, when the dividend was 7.6p and revenue earnings 7.54p. The second was 2010, when the dividend was 10.9p and revenue earnings 9.6p. That was the year when BP (BP.) cut its dividend and a number of manager changes meant we were less fully invested than normal.

‘Since 1974, the dividend has risen from 0.38p to 19p in 2016, an annual growth rate of 9.8% over the 42 years, during which UK consumer prices rose by 5.7% per annum, so our dividend has on average risen 4% faster than inflation.’ (JC/LMJ)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

Editor's View

Funds

Great Ideas

Great Ideas Update

Investment Trusts

Larger Companies

Main Feature

Smaller Companies

Story In Numbers

- AIM Stocks Ranking

- UK Pharma & Biotech Stocks

- Esure escapes Ogden damage

- 3-month low: Oil slips as US activity ramps up

- 7.9%: Investment trust’s big bet on Sports Direct

- 76%: Percentage of money going into European tech firms by US and Asian investors

- 25%: Ramsdens on the rise

- 500 tonnes: Morrisons is in good shape