Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineHow to find the right shares if you want to reinvest dividends

Would you like some help in spotting individual companies that could be interesting candidates for a dividend reinvestment strategy? This article discusses a way to find stocks that are highly cash generative and so have the potential to pay more and more dividends each year.

We also run through some stocks that have been suggested by stock screening systems, based on criteria meant to find good dividend growth stories. More on that later.

Where do I start?

The combination of dividend growth and dividend reinvestment can be very powerful in terms of powering up the value of your portfolio.

A quick and straightforward way of checking a company’s ability to grow the dividend and provide plenty of income that you can reinvest is to look at how many times the dividend per share is covered by earnings per share.

However, to be really sure you need to go further as dividends are not paid out of earnings but from a company’s free cash flow. Essentially this is all the cash left after a company has paid tax, the cost of borrowing and put money back into the business for areas like new equipment – also known as capital expenditure or capex.

Here’s how you calculate free cash flow. Find net cash from operations in a company’s results statement, add dividends received from joint venture companies (if there are any), take away capex, interest paid to lenders, dividends paid to any preferred or minority shareholders and add back any income from interest payments.

To work out a per share number, take the free cash flow and divide it by the number of shares in issue – which you can find in recent stock market announcements or the latest set of financial results (it will be buried in the numbers near the end).

How can I tell if a dividend is sustainable?

Dividing free cash flow per share by the dividend per share would help determine the sustainability of a payout. Any figure less than one would imply the company is funding its dividend through debt or retained earnings.

For example, BP’s (BP.) free cash flow per share of 8.7 cents in 2016 failed to come close to covering a full year dividend of 40 cents. The stock currently yields 6.8%. A high yield generally in excess of 5% can be a signal from the market that a dividend is risky and potentially unsustainable.

On the other side of the coin, Bunzl’s (BNZL) free cash flow per share of 93.8p in 2016 comfortably covers a dividend per share of 42p. A prospective yield of 1.5% may look pretty skinny but the consistent growth in the dividend makes Bunzl very interesting from a dividend reinvestment perspective.

The company says its dividend has gone up every year for the past 24 years, at a rate of more than 10% compound annual growth.

By putting money into an investment that delivers a consistent return – and then reinvesting that cash in to buying more shares – you capture the future returns on your reinvested profits as well as from your original investment.

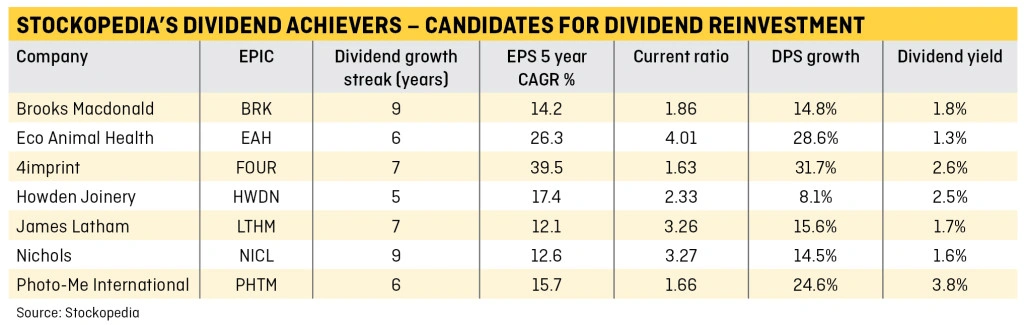

Dividend Reinvestment Candidates

Stockopedia has a system that identifies stocks which could potentially fit a dividend reinvestment strategy.

Let’s now look at seven stocks that appear in Stockopedia’s screener alongside an exchange-traded fund which may interest someone who wants a more diversified investment.

Brooks Macdonald (BRK:AIM) £19.85

The wealth manager specialises in a profitable niche, serving clients with investable assets between £100,000 and £1m. It continues to benefit from industry changes designed to rid the finance industry of controversial practices which have historically seen investors receive bad advice and poor value for money.

Among the first to structure its service around fee-based advice rather than commissions, Brooks was well positioned before new regulations tightened up the industry in 2013.

ECO Animal Health (EAH:AIM) 510p

Veterinary drugmaker Eco Animal Health (EAH:AIM) is enjoying strong demand for its pig and poultry antibiotic Aivlosin. Early in 2017 the company received approval for the use of water soluble Aivlosin in chickens laying eggs for human consumption in Mexico. This was an important step as Mexico is one of the five largest egg producing countries in the world.

The company is in the process of submitting regulatory filings in other key egg producing markets. House broker N+1 Singer comments: ‘We continue to expect Aivlosin to generate strong growth in multiple geographies, with additional formulations, indications, geographies and species providing further growth potential.’

4imprint (FOUR) £16.52

Promotional products business 4imprint (FOUR) is the market leader, although there is still plenty of room to grow as it only has a 2% share of a $24bn addressable market in the US.

The company is inherently cash generative with limited requirements for working capital or capital expenditure. Now that action has been taken to address the company’s pension liabilities (76% of which are now insured), the company should be able to deliver more generous dividends to shareholders.

Howden Joinery (HWDN) 426.1p

Kitchens seller Howden Joinery (HWDN) has a strong balance sheet and a good track record of managing costs during downturns to preserve profitability. It sells to trade customers through a network of more than 600 depots in the UK.

In 2015 it supplied in excess of 400,000 kitchens, 2.4m doors and 750,000 appliances to UK homes. If it delivers the forecast 11.2p per share payout in 2017, Howden will have served up a 30.1% compound annual dividend growth over five years.

James Latham (LTHM:AIM) 897p

The timber merchant was founded at the dawn of the 20th century and has been profitable through any number of stock market cycles.

Improving revenue and prudent cost control is having a positive impact on operating results for the business. The company has net cash on the balance sheet and the first half dividend was covered 6.9 times by earnings. That implies plenty of scope for further dividend increases.

Nichols (NICL:AIM) £18.56

The company owns a range of highly profitable niche soft drink brands which are sold across the globe. Key brands Vimto, Levi Roots, Sunkist and Panda are consumer favourites in some key geographies.

Recent additions to the portfolio include the purchase of premium juices outfit Feel Good and iced drinks specialist the Noisy Drinks Co. Its long standing position as a reliable dividend payer is underpined by a strong balance sheet.

Photo-Me International (PHTM) 167p

Photobooth and laundry machine operator Photo-Me International (PHTM) has been beset by one-off setbacks in the last 12 months including delays to a Japanese ID programme last summer and the UK Home Office considering if photos taken on mobile phones can be used for passports.

Long-term growth is likely to come from the introduction of 3D photo and e-signature technology in photo booths and the roll-out of Photo-Me’s laundry machine division. The company is highly cash generative and this has supported double-digit growth in the ordinary dividend alongside a number of special payouts.

Source FTSE RAFI UK Equity Income Physical (DVUK) £10.23

Launched in March 2016, this exchange-traded fund tracks UK-listed stocks that have the potential to offer a high, sustainable income. It has a total expense ratio of 0.35%.

A large chunk of the fund (22.8%) is in the financial sector. Top holdings include bank Standard Chartered (STAN), miner Rio Tinto (RIO), oil major BP and pharmaceuticals business GlaxoSmithKline (GSK). (TS)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

Editor's View

Funds

Great Ideas

Great Ideas Update

Investment Trusts

Larger Companies

Main Feature

Smaller Companies

Story In Numbers

- AIM Stocks Ranking

- UK Pharma & Biotech Stocks

- Esure escapes Ogden damage

- 3-month low: Oil slips as US activity ramps up

- 7.9%: Investment trust’s big bet on Sports Direct

- 76%: Percentage of money going into European tech firms by US and Asian investors

- 25%: Ramsdens on the rise

- 500 tonnes: Morrisons is in good shape