Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazinePower up: dividend reinvestment special

If you’re a long-term investor one of the simplest ways to boost your returns is to reinvest dividends. You end up owning more shares or units in a fund without putting your hand in your pocket for more cash beyond the original investment.

Let’s say you own £10,000 worth of shares in Company X. This pays 5% dividend each year, equal to £500 on your £10,000 investment.

If you reinvest that £500 in more Company X shares, you will have an investment worth £10,500. Fast forward one year and your 5% yield on the bigger-sized investment equals dividends worth £525 – so £25 more than you got last time.

If you reinvest that £525 in more Company X shares, your overall pot will be worth £11,025. A 5% yield a year later on that pot equates to £551.25. That’s £51.25 extra money from dividends versus what you received two years earlier.

You can see how your dividend keeps getting bigger each year, so too the size of your overall investment – and that’s without assuming any share price appreciation.

If you keep recycling your dividends into buying more shares or fund units, in time you can really power up the value of your portfolio.

> How do I reinvest?

Historically, the only way for investors to automatically reinvest dividends was to join each individual company’s dividend reinvestment plan, also known as DRIP. These plans, which are operated by the company’s registrar, are usually only provided by the largest companies on the stock exchange.

Sadly the number of companies offering scrip dividend schemes has fallen rapidly over the past decade to around 25 blue-chip stocks.

Thanks to technological advances at investment platforms, it’s now possible to get nearly all your dividends reinvested via a different route – that applies to stocks, exchange-traded funds (ETFs) or investment trusts.

Dividend reinvestment isn’t suitable for everyone so it’s important to assess your individual circumstances before jumping on board.

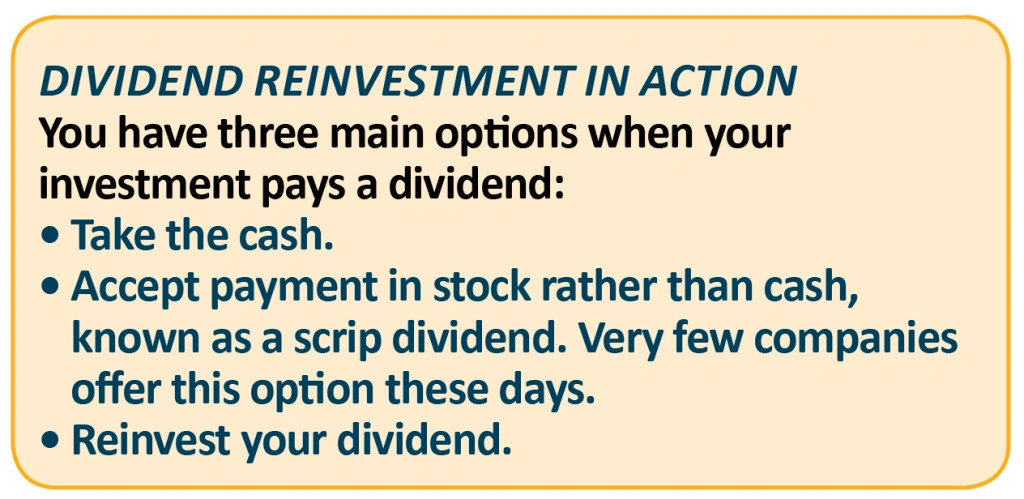

If you want to reinvest, you can set up automatic dividend reinvestment online via your investment platform and they will ensure the monies received are used to acquire more shares in the same quoted company.

> How much does it cost to reinvest?

Dividend reinvestment won’t be free via your ISA or SIPP (self-invested personal pension) provider. You will have to pay a charge, although it is normally much cheaper than the normal fees to buy and sell shares.

On average, platforms charge a flat fee of £1.50 or a percentage-based fee of 1% of the dividend value (subject to a minimum of £1.50 and a maximum of £9.95). The fee will be levied on every reinvestment deal the platform carries out. You will also have to pay stamp duty.

In the vast majority of cases it’s likely the fees levied for dividend reinvestment will be far lower than if you received the dividend and then bought more shares via a standard trade. At AJ Bell Youinvest, for example, the standard dealing charge is £9.95 unless you made 10 or more trades the previous month, in which case it is £4.95. Its dividend reinvestment fees can be as low as £1.50.

‘Dividend reinvestment schemes are more cost-effective and efficient than buying shares through a normal trade at a broker,’ comments Jon Wingent, head of portfolio specialists at Lloyds Wealth Investment Office.

> What's the minimum amount I can reinvest?

In order for a dividend to be reinvested it must meet the platform’s specified minimum amount, which is usually £10. It also needs to be sufficient to buy at least one share in the company.

You can choose whether to reinvest individual dividend payments or to reinvest all the dividends for all the investments you have now and will have in the future.

You will need to instruct your broker for each account you hold with them – so if you have an ISA and a SIPP you’ll have to make an election for each one.

Most platforms enable you to reinvest dividends from a wide range of shares, investment trusts, trackers and ETFs. Some restrict their service to FTSE 350 stocks, or at the very least UK-listed companies.

It is possible to apply automatic dividend reinvestment to funds at some brokers, but this isn’t the most cost-effective approach. If you want to reinvest the income received from a unit trust or OEIC fund it’s better to buy the accumulation (‘acc’) version of the fund rather than the income (‘inc’) version.

The ‘acc’ version will automatically reinvest dividends so you don’t even have to use your broker’s reinvestment service to arrange for that trade to be made.

> Show me more evidence that reinvesting is worthwhile

By reinvesting dividends, you have mathematics on your side because you get to harness the power of compounding.

‘With dividend reinvestment you’re building up your capital without having to buy more shares or do much at all,’ says Wingent.

The effects of compounding will be more pronounced the longer you remain invested, which means dividend reinvestment is better for those who have a long-term time horizon.

Russ Mould, investment director at AJ Bell Youinvest, gives the example of an investor who invests the 2016/17 ISA allowance of £15,240 and then makes no further contributions. His working example assumes the FTSE All-Share generates a compound annual growth rate of 6.8% and pays a dividend yield of 3.8%.

After subtracting 1% a year for platform administration and dealing fees, the initial £15,240 will be worth £26,610 after 10 years, £46,464 after 20 years and £81,129 after 30 years. You would have also banked £1,011, £1,765 and £3,082 respectively in cash dividends as well.

These are attractive figures, but they are far lower than those received by an investor who banks the same capital return and reinvests dividends. In this case, the initial £15,240 investment becomes £37,747 over 10 years, £93,496 over 20 years and £231,577 over 30 years.

‘This is a simplistic example, as returns will not come in straight lines. However, it shows the potential offered by compounding and how stock market investing can be a way to get rich slowly.

‘It requires to you to work to a long-term time horizon, be able to identify stocks or funds where the dividend payments are safe and reliable, and withstand the inevitable bear markets that will follow the bull ones along the way,’ says Mould.

> When shouldn't I reinvest dividends?

There are some instances when dividend reinvestment won’t be suitable, so it’s important to think about your overall investment strategy, target returns, time horizon and appetite for risk.

‘If you are in drawdown in retirement, for example, you may wish to start banking dividends. If you are much younger and still building your savings pot then you may prefer to reinvest them and try to get the power of compounding to work in your favour,’ Mould says.

Even if you’re young and have a high risk appetite, you might want to consider keeping a residual portion of your portfolio in cash.

‘The liquidity can help in case of unexpected emergencies, meet any fees and also provide a buffer so that you have some cash around when you need it and are not forced to sell holdings at what could be an inconvenient time, such as during a bear market when prices could be depressed,’ Mould explains.

> Keep an eye on your portfolio

If you have a portfolio comprised of dividend and non-dividend paying stocks, your portfolio could become unbalanced if you opt for dividend reinvestment. This is because reinvesting dividends increases your holding in these stocks.

You might need to adjust your portfolio in order to ensure your exposure to certain stocks, sectors and geographies continues to match your risk profile.

Furthermore, it’s important not to let the availability of dividend reinvestment schemes cloud your judgement when choosing which investments to buy.

Wingent says if a stock has a very high dividend it could be a sign the company is not of a high quality and dividend payouts might not be sustainable.

To help you on your investment journey, we have written two more articles that discuss stocks and investment trusts which might interest anyone seeking ideas to support a dividend reinvestment strategy.

Read those articles now. You can find the stocks one here and the investment trusts one here. (EP)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

Editor's View

Funds

Great Ideas

Great Ideas Update

Investment Trusts

Larger Companies

Main Feature

Smaller Companies

Story In Numbers

- AIM Stocks Ranking

- UK Pharma & Biotech Stocks

- Esure escapes Ogden damage

- 3-month low: Oil slips as US activity ramps up

- 7.9%: Investment trust’s big bet on Sports Direct

- 76%: Percentage of money going into European tech firms by US and Asian investors

- 25%: Ramsdens on the rise

- 500 tonnes: Morrisons is in good shape