Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineSpice up your portfolio with a VCT

If you want to add some spice to your portfolio and mitigate your tax bill it is worth looking at the current range of venture capital trust (VCT) offers.

Investing in a VCT enables you to get immediate exposure to a portfolio of small businesses which the VCT’s manager reckons have significant growth potential. They might be companies that are disrupting existing sectors or ones offering opportunities in new sectors; often their performance is uncorrelated to the stock market.

VCTs offer 30% income tax relief, as long as you remain invested for at least five years. This essentially means that a £10,000 investment would cost you £7,000. If you sell your investment after five years you can reinvest the money into a different VCT (or the same VCT if a further six months have passed) and get a further 30% tax relief. You can do this as many times as you like.

There is a common belief that VCTs are the preserve of the super-wealthy, but the minimum investment required is usually £3,000 or £5,000. Most experts advise not to allocate more than 10% of your portfolio to VCTs, which means they could be suitable for someone with a £50,000 portfolio.

Pension supplement

In recent times, VCTs have become a popular way to supplement traditional forms of pension planning. Once VCT investments have been held for five years, you can access your money in full without paying tax (assuming there is enough liquidity). This differs to a pension which only lets you take 25% of the pot tax-free, with the balance taxed at your marginal rate.

GOLDEN RULES FOR VCTS

Investors should buy any type of VCT direct from the fund manager or a specialist VCT broker during the offer periods to get all the tax benefits.

You can buy VCTs on the open market (also known as the secondary market) but you would lose the 30% income tax relief.

You will lose significant tax benefits by selling before five years is up, regardless of the type of VCT product originally purchased. Selling a VCT in this first five years should only be done as an action of ‘last resort’.

If you do sell before the first five years is up, you would need to tell the taxman HMRC and reimburse the relevant income tax relief amount.

You can invest up to £200,000 into VCTs each year, which makes them useful vehicles for people who’ve reached their pension annual allowance or lifetime allowance.

‘Unlike other tax-efficient investment schemes like the Enterprise Investment Scheme, the income tax relief associated with the VCT will typically be available within a few weeks of investing, hence investors can mitigate their tax liability immediately and may never need to pay the tax in the first place,’ says Hugi Clarke, director at VCT manager Foresight.

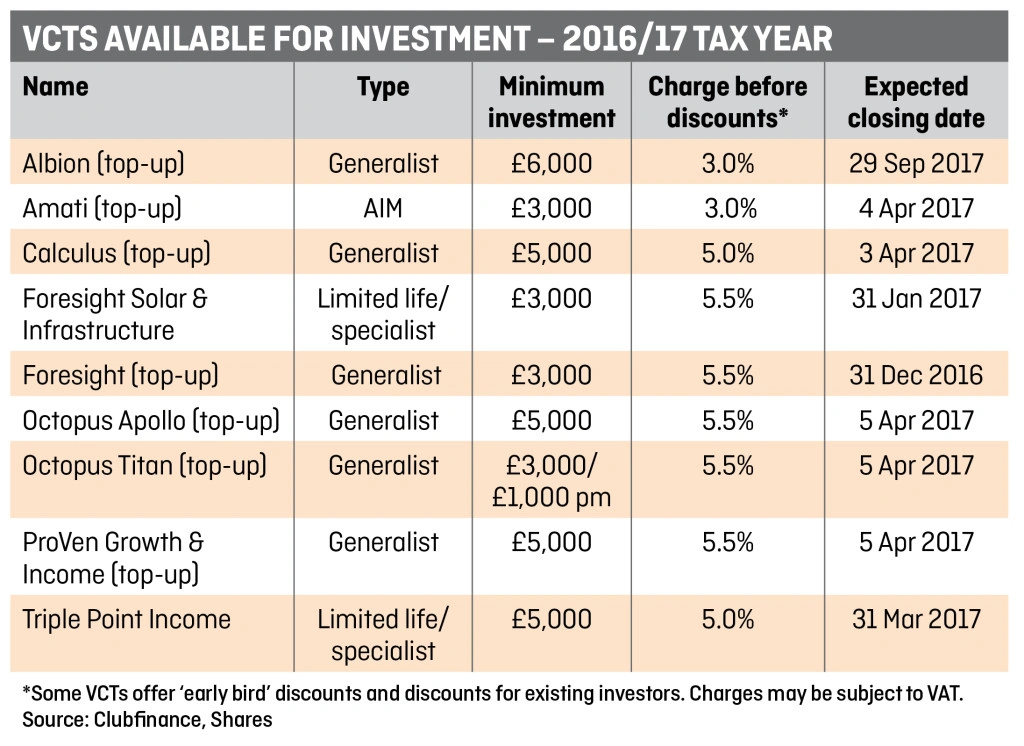

VCTs are also worth considering if you want a decent income stream. Most VCTs target an annual dividend of around 5%. Some dividend targets are even higher – Calculus (CLC) recently launched a VCT top-up offer which aims to deliver a dividend of more than 6%, while Triple Point Income (TPV1) targets a 7% annual dividend.

Types of VCTs

There is a misconception that the riskiness of VCTs is the same across the board, when in reality the risk varies according to the companies they invest in. It’s a good idea to look at which sector(s) the VCT concentrates on and whether the companies are true start-ups or are already generating revenue or profit.

Generalist VCTs invest across a range of sectors, whereas specialist VCTs invest in a specific sector such as biotech. AIM VCTs focus on companies that are quoted on the AIM market.

Jason Rolf, business development manager at Amati Global Investors, says AIM VCTs typically invest in larger, more established companies which have reasonable liquidity.

The Amati VCTs invest in companies with a value of more than £15 million. Recent investments include remote meeting provider LoopUp (LOOP:AIM) and e-learning provider Learning Technologies (LTG:AIM).

The vast majority of VCTs are generalist. Beringea’s ProVen Growth & Income (PGOO) invests in over 40 companies. It predominantly focuses on the digital media industry but holdings also include a costume jewellery manufacturer and a pre-owned watch retailer.

Octopus Titan VCT (OTV2) invests in early-stage businesses, typically around two or three years old. Almost all the investments are equity-based ones. A current holding is Tails.com, a pet food delivery company.

Octopus Apollo VCT (OAP3) invests in companies that are five to seven years old which have longer track records. A current investment is Clifford Thames, which provides support services to the automotive industry. Octopus Apollo uses debt investments where possible, rather than equity.

‘This gives downside protection. There is a much higher chance of getting money back if things go wrong,’ says Stuart Lewis, business line manager at Octopus Investments.

Specialist

Foresight Solar & Infrastructure VCT (FTSD) is a specialist VCT because it focuses on one sector. It invests in ‘smart data equipment’, which sends electricity and gas usage data back to the energy supplier every 30 minutes.

Foresight Solar & Infrastructure VCT is a ‘limited life’ or ‘planned exit’ VCT, which means it’s designed to provide liquidity at some point in the future; in this case, in six years’ time.

‘You don’t get the upside you would with the Foresight VCT, but because there is a planned exit it offers a more stable return. A solar park provides predictable revenue, especially if the VCT buys an existing park which has, say, two years of data. You can be fairly confident your return will be positive and there will be liquidity,’ says Clarke.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.