Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineFTSE 100 dividend health check

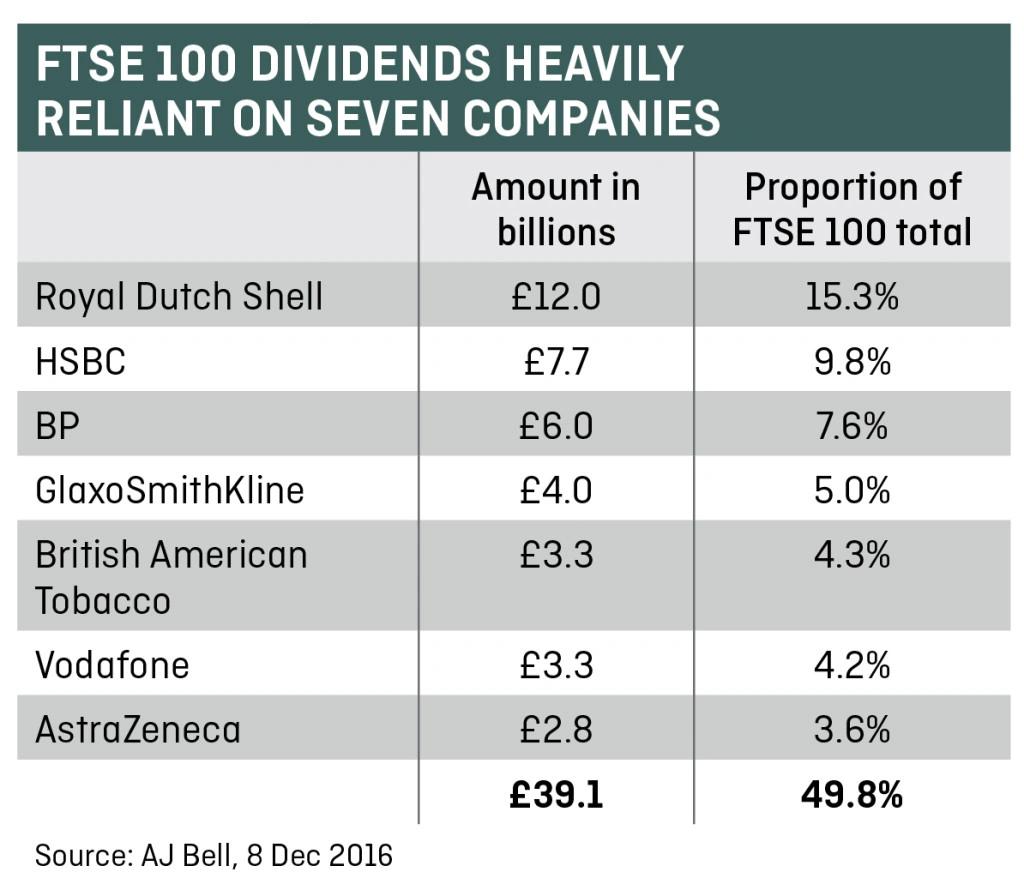

AJ Bell’s latest Dividend Dashboard report shows half the dividends from the FTSE 100 are forecast to be paid out by just seven companies in the coming 12 months.

The reliance on just a handful of big dividend payers to generate the yield from UK shares means investors need to remain watchful in 2017 to ensure they are not caught out by a cut or cancelled payout.

High yield

The constituents of the index are forecast to pay total dividends of £78.4bn in 2017, which equates to a yield of 4.2%. This looks highly attractive in light of the modest returns available from cash on deposit but there are risks attached.

The 10 highest yielding FTSE 100 stocks all have dividends covered less than two times by earnings and just one has cover of more than 1.5 times. As a rule of thumb, cover below this threshold could suggest a dividend is under threat.

The correlation between high dividend yield and low dividend cover makes sense. A high yield is often an indication the market does not believe the dividend is sustainable. For this reason, Shares has consistently argued investors should focus on dividend growth not yield.

Growth beats yield

Strong share price performance means the yields offered by dividend growth companies may not be the most eye-catching but over time they could still prove excellent investments. The ability to consistently grow a dividend implies a stock is cash generative and shareholder-friendly.

Encouragingly AJ Bell’s data shows the FTSE 100 is set to grow dividend payouts by £4.6bn in 2017.

Drilling down to the individual high yielders, Oil majors BP (BP.) and Royal Dutch Shell (RDSB) have struggled to cover their generous dividend payments from earnings or cash flow for some time. Yet Shell has a proud track record to defend, having not cut its dividend since the Second World War.

Mobile telecoms play Vodafone (VOD) is emerging from a period of heavy capital investment which has constrained earnings and made its cover look particularly skinny. We are more comfortable about its ability to pay dividends in the future, assuming capital expenditure starts to fall.

Academic publisher Pearson (PSON) could be vulnerable to a dividend cut as it faces a structural downturn in the US higher education market which has led to several profit warnings.

Danger zone

There are 25 FTSE 100 dividend payers with cover of 1.5 times or less. Some of these names, including Pearson, could be considered in the ‘danger zone’ but the dividends from utilities can probably be considered safe.

These companies have excellent earnings visibility as their returns are largely regulated and therefore it is not unusual for them to have dividend cover of close to one times.

Similarly, real estate investment trusts (REITS) such as Hammerson (HMSO), British Land (BLND) and Land Securities (LAND) are structured to pay out at least 90% of their taxable income to shareholders as dividends so you would expect their cover to be low.

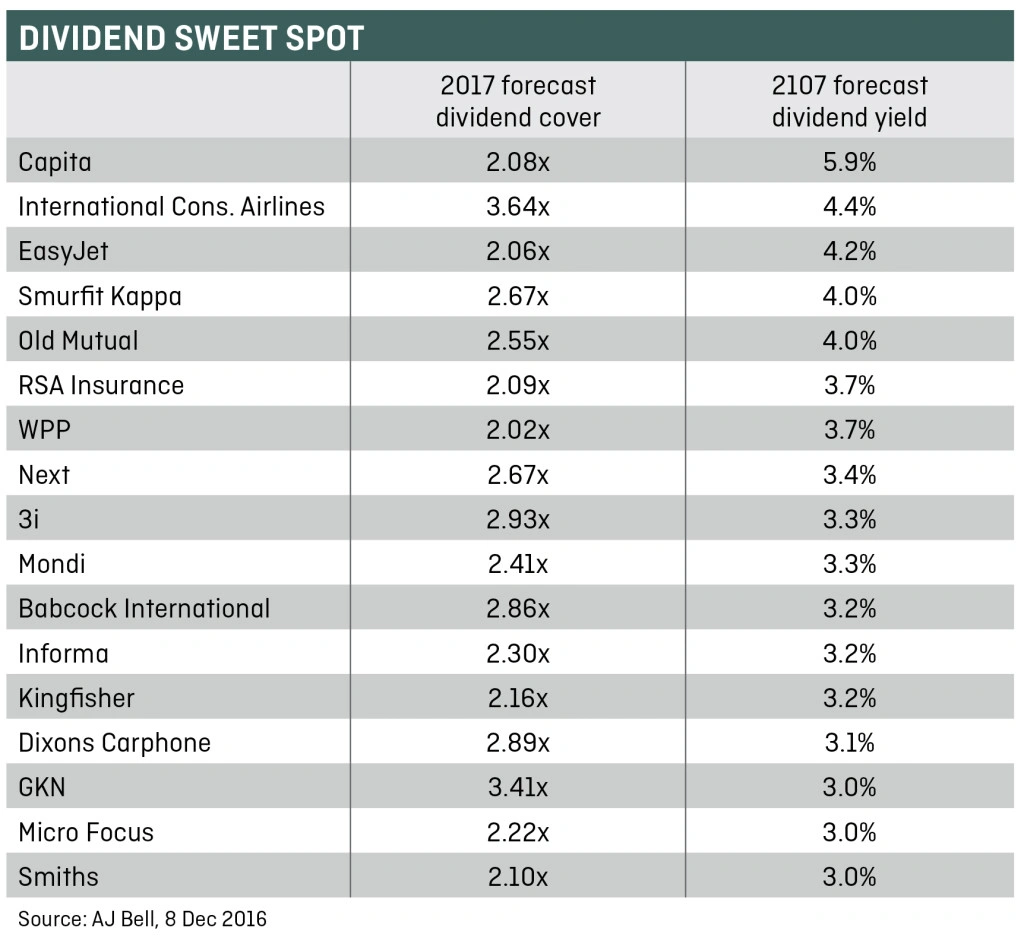

Sweet spot

AJ Bell has identified 17 FTSE 100 companies which are forecast to yield more than 3% in 2017 that also have cover of two or more.

Outsourcer Capita (CPI) should be dismissed by any prospective income investor having this year warned on profits twice in the space of three months thanks to contract delays and trading issues.

However, names such as advertising giant WPP (WPP), retailer Next (NXT) and software firm Micro Focus (MCRO) stand out thanks to their excellent track records of cash generation and dividend growth.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.