Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineGo east for income

If you want to diversify your portfolio income and access the main bright spot in a sluggish global economy you could consider Henderson Far East Income (HFEL).

The trust looks to provide a high level of dividends and capital appreciation over the long term, from investments traded on the Pacific, Australasian, Japanese and Indian stock markets.

It trades at a modest 1.9% premium to net asset value (NAV), reflecting consistent demand for the shares.

Run by Michael Kerley, he is a bottom-up, cash-flow focused manager with a consistent disciplined approach. Under his stewardship, ‘HFEL’ delivered an NAV total return of 32.1% for the year to 31 August, bolstered by improving Asia Pacific stock markets and sterling weakness post-Brexit vote. ‘It was a year dominated by events and thematics,’ says Kerley, ‘and it helped having overseas assets and a sterling based fund.’

His confidence in Asian dividend sustainability and growth allows HFEL to increase its dividend by a healthy amount each year. In the year to August, the dividend was increased by 4.1% to 20p. HFEL should be able to continue with these progressive payouts as it has revenue reserves equivalent to 67% of that full year distribution.

Structural growth

Differentiating features of the fund include Kerley’s process, which focuses on sustainable income distribution and income growth with a bias towards stocks that have real investment appeal rather than a just a high yield. The trust also has greater exposure to the Asian structural income story and less exposure to Australia than its closest peers.

Attractive valuations are key to the investment case in Asia, where a reform agenda across the region is driving improved corporate governance, shareholder friendly initiatives and record high institutional ownership. Kerley also points out that Asia’s high real interest rates provide monetary flexibility, while its markets are cheap relative to earnings, their own history and ex-Asia markets.

Kerley argues the outlook for Asia is a positive one based on fundamentals, not just the region being under-owned. ‘Asia looks pretty attractive as there’s a degree of stability in China, earnings are improving across the region and valuations are cheap.’ Kerley also believes US President-elect Donald Trump, who has accused China of being a currency manipulator, would be ‘foolish’ to impose trade sanctions on the Asian powerhouse. ‘US companies sell more goods in China than they make in China and export back to the US,’ he explains.

Double digit growth

‘There’s a strong chance of double-digit dividend growth from the portfolio this year,’ stresses Kerley, who flags the fact that Asian companies have gone through change, now exhibiting lower growth but generating strong cash flow and dividends.

‘Debt levels in Asia are very, very low,’ explains Kerley, ‘and free cash flow is going through the roof’. With capital expenditure and payout ratios both low, Kerley has great confidence in Asia’s dividend growth potential.

Furthermore, he says the potential for large amounts of cash held in Asian bank accounts to move into yielding assets as interest rates fall is a very real one, replicating the dynamic that has driven asset prices in the West since the 2007/8 financial crisis.

The A-team

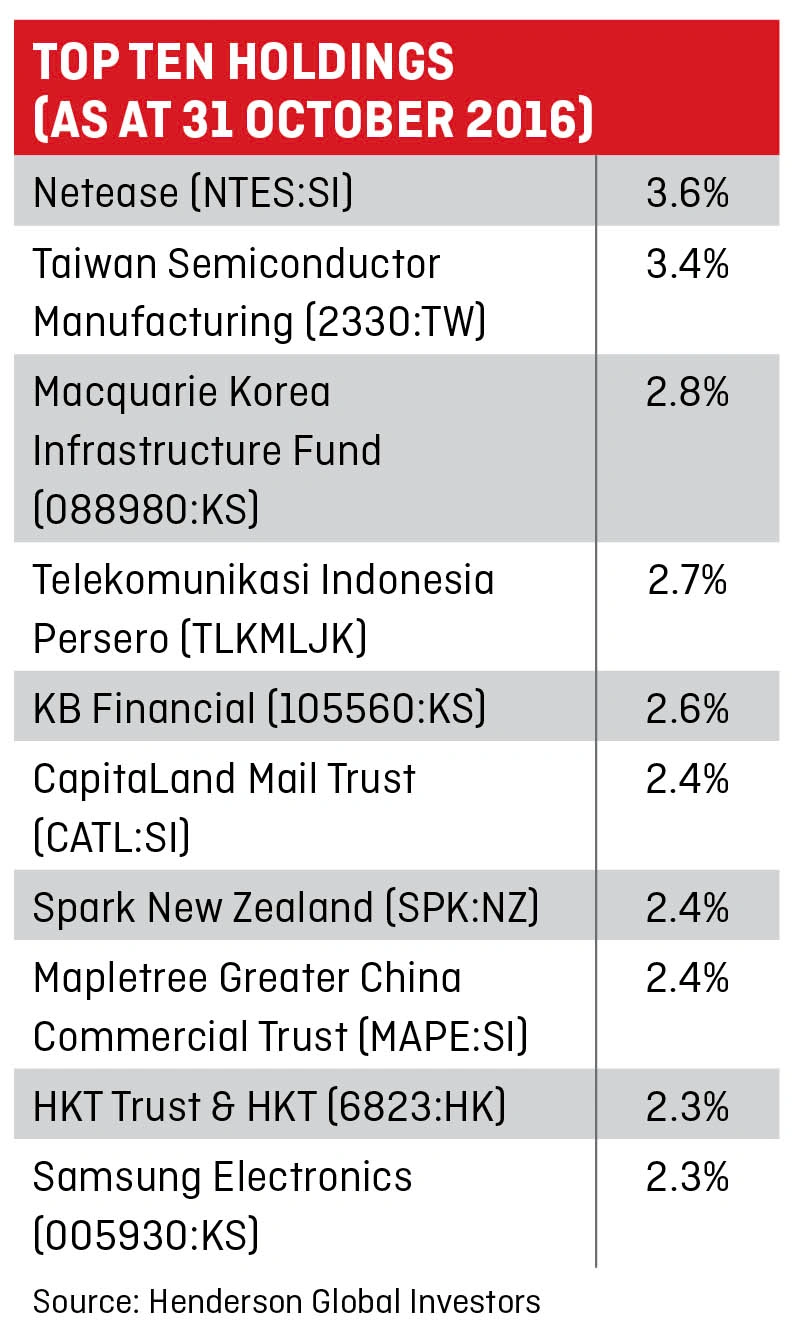

HFEL currently has zero exposure to consumer staples or healthcare as Kerley views these sectors as expensive. The largest country allocation is to China at around 20% and roughly 8% of the HFEL portfolio is invested in four China A-shares, each yielding over 4%. Kerley sees the Chinese A share market as ‘one of the most interesting opportunities in Asia’, being uncorrelated with the stock markets of China, Hong Kong or the rest of the world.

The four include Zhengzhou Yutong Bus, trading on a PE ratio of 12 times and a 6.5% dividend yield. ‘More recently, it has become the largest maker of electric buses in the world, selling into the rest of Asia as well as France’, says Kerley. Other A share positions include China Yangtse Power and Huayu Automotive Systems.

The sector generating the most income for the fund is financials, a big proportion coming from Chinese banks. ‘We like toll roads in China,’ adds Kerley, an investor in toll road operator Jiangsu Expressway.

One high-flying Chinese dividend growth stock that has appreciated strongly since purchase in February 2014 is Netease, an internet technology company which has re-rated due to the strength of its mobile gaming business and solid PC gaming franchise.

Samsung revisited

‘We have had Japan in the portfolio but we gave up,’ continues Kerley. ‘Some 18% of the portfolio is in Korea,’ he explains, having recently added electronics titan Samsung after an eight year portfolio absence. Though not typically a high yielding stock, Kerley believes this may be about to change, as a result of corporate restructuring involving the inclusion of heir apparent Jae Yong Lee to the board, a catalyst for more shareholder-friendly policies.

‘We do have three stocks in India,’ continues Kerley, referring to Infosys, Bharti Infratel and Coal India, ‘but none of them are dependent on the domestic economy.’

HFEL does have just shy of 19% of its portfolio in Australia. While Kerley is not particularly positive on the country, he says ‘in terms of yield you can’t ignore it.’ One Australia-listed holding of note is banking firm Macquarie. Its fund business could benefit from Trump’s anticipated infrastructure spending in the US.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.