Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineSolid income: Earn more than 4%

A lot of people moan about how difficult it is to get a decent income from the market, but is it really that hard?

The FTSE 100 index currently yields 3.86%, so you can buy a low-cost tracker fund and get that level of income with relative ease. Getting a higher level of income is also fairly easy if you do some research.

This article discusses the stocks, ETFs and funds with the potential – but not the guarantee – to pay at least 4% a year; some paying more than 10%.

Plenty of choice

More than 200 companies on the UK stock market have prospective dividend yields in excess of 4%, according to data from SharePad.

We’d only rate a small proportion of these stocks as good investments for a sustained source of decent income. Most either have unsustainable dividends, in our view, or have yields artificially inflated by one-off special dividends.

Some of our favourite income plays include Phoenix Group (PHNX) and Card Factory (CARD) as discussed later in this article.

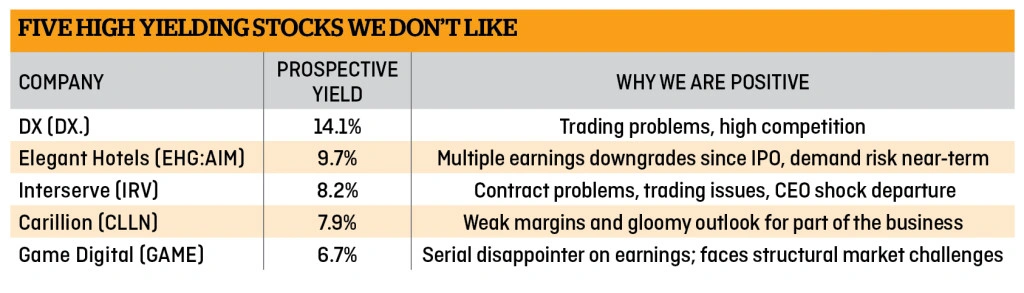

We also comment on companies whose high prospective dividend yields mask fundamental problems within the business. DX (DX.), Interserve (IRV) and Game Digital (GMD) are on our list of stocks which you should not buy for income, in our opinion, despite current forecasts implying yields up to 14.1%.

How to calculate dividend yield

Many financial data providers will publish yields based on the dividends paid in the last financial year.

We always prefer to use forecast dividend information, not historic. As an investor you should always be looking to the future.

Prospective dividend yields are calculated as follows:

Forecast dividend per share for the current financial year ÷ latest share price × 100

Analysts will estimate how much a company might pay out in dividends and the data providers like SharePad will take the average of all forecasts in the market. That’s your forecast dividend per share figure.

The analysts will inevitably get some guidance from the company in question as to what earnings could be in the current year, so they aren’t guessing blindly to produce a dividend forecast.

That said, there are plenty of occasions when a company hasn’t met its earnings guidance and so the dividend has been less than expected. You must always remember that dividends are not guaranteed payments.

Don't be misled by special dividends

The other issue to consider with dividend forecasts is that most financial data providers don’t separate normal dividends from special dividends. For example, you might see a forecast for 5p per share for Company XYZ which equates to a 12% yield.

That would certainly be attractive, yet the yield could have been temporarily inflated by a special dividend component. Special dividends are rewards on top of normal dividends. They tend to be paid when a company sells something and gets a big chunk of cash, or when there is a higher amount of cash generated from operations than normal.

Special dividends are generally a one-off event and so the 12% headline yield in our aforementioned example wouldn’t be representative of the level of income you would normally receive from the shares.

Drinks distributor Stock Spirits (STCK) is a relevant example. It has a 9.4% prospective yield, yet that’s inflated by a special dividend declared in June as it had spare cash after deciding not to make any material acquisitions for the rest of the year. The previous year it only paid 5.8c (4.9p) per share which equates to a normalised yield of 2.8%.

OUR TOP STOCK PICKS FOR INCOME

Phoenix Group (PHNX) 711.5p

Prospective yield: 6.5%

This highly cash-generative company is Britain’s largest owner of life assurance funds closed to new customers. Phoenix says this business model enables it to focus all of its energy and expertise on improving the performance of funds without being distracted by the need to win new customers.

Earlier this year, Phoenix had a target of generating £2bn cash between 2016 and 2020. More recently Phoenix unveiled plans to buy Abbey Life for £935m, a deal that will add £1.6bn in future cash flow.

Card Factory (CARD) 255.2p

Prospective yield: 9.5%

Card Factory could be one of the few stocks to pay special dividends year in, year out. That’s according to Peel Hunt which has analysed the company’s earnings and cash flow capabilities, together with its debt position and trading history in good and bad economic cycles.

‘The cash flow remains extremely robust and we class the special dividend as set in stone. Thus, the 10% yield is not illusory, making the shares terrific value,’ wrote Peel Hunt on 18 November.

Trading was a bit slow earlier this year, hence some share price weakness, but the company says things have improved since October. Card Factory thrived in the last recession and we believe it could do the same again if economic conditions deteriorate in the UK.

HIGH YIELD STOCKS TO AVOID

DX Group (DX.) 17.375p

Prospective yield: 14.1%

The parcel delivery firm hit the stock market with a splash in 2014 with an eye-catching 7% dividend yield. It has not worked out well for anyone tempted by that yield. The share price has crashed from 100p at IPO to a mere 17.375p and the dividend has already been cut back.

Trading is very tough as a result of high competition and rising costs. Not even Numis – which is its broker – can stir up any enthusiasm, having downgraded earnings forecasts last month and saying it was cautious on the investment case.

Further dividend cuts look possible if earnings remain weak. Steer clear.

Interserve (IRV) 310.75p

Prospective yield: 8.2%

Contract delays, contract problems, the recent departure of long-standing chief executive, five consecutive years of supposedly ‘one-off’ items….Interserve is in a mess.

Management reckon profits can grow in 2017; analysts reckon they will fall. The dividend might be sustainable, yet the share price has further to drop in our opinion. You could end up getting 8.2% yield but the shares could easily fall by 10% or more, thus you’d have a negative total return. Avoid.

EARNING A DECENT INCOME FROM EXCHANGE-TRADED FUNDS (ETFS)

Exchange-traded funds, investment trusts and other types of funds can be great ways to access lots of dividend-paying companies through a single product.

The downside of a lot of passive dividend-themed funds – which includes many ETFs – is that they select companies to track based on their headline yield. You need to remember that a falling share price can make a dividend yield look artificially high.

Share price weakness could be a warning sign. The more a share price falls, the higher the dividend yield assuming there is no change to the dividend forecast. You need to ask why the share price is falling – it could be the market worrying about trading prospects. A reduction in earnings could eventually lead to a reduction in the dividend, so the yield will fall.

You also need to consider whether companies are using dividends to lure in investors – when actually the money could be better spent on improving the business.

iShares UK Dividend GBP Distribution (IUKD)

Trailing yield: 5.5%

This is a good example of an ETF which has polarised opinion among experts. The ETF is a good way to get exposure to the more generous dividend payers among mid and large cap stocks on the UK stock market.

The ETF aims to mirror the performance of 50 highest yielding companies in the FTSE 350 index excluding investment trusts, based on forecast one-year dividend yields.

The top holdings include Legal & General (LGEN), Royal Dutch Shell (RDSB), HSBC (HSBA) and BP (BP.).

There is a 0.4% in-built fee which is really cheap compared to many mainstream income funds that might have many of the same stocks in their portfolio.

Dividends are paid every three months, so this could interest someone who needs a regular stream of cash to pay the bills.

Morningstar is not a fan of the ETF. It says the fund has lagged its peers, has a high level of volatility and doesn’t check whether dividends have been maintained or raised every year by the underlying assets. It has awarded the product a ‘negative’ analyst rating, calling it a below-average investment proposition.

SPDR S&P UK Dividend Aristocrat ETF (UKDV)

Trailing yield: 4.5%

The ETF provides access to the 30 highest yielding UK companies that have managed to either maintain or grow dividends for at least 10 years in a row.

This screening method means you don’t get exposure to companies that have irregular dividends. The index also provides some level of futureproof protection in that it will remove any companies should they break the sustained/growing dividend rule.

Dividends are paid once every six months. The in-built fee is 0.3% each year.

The top 10 contains quite a few stocks we don’t like at present including Pearson (PSON) and Carillion (CLLN). However, we do like BAE Systems (BA.), GlaxoSmithKline (GSK) and Burberry (BRBY) which also feature in the biggest

holdings list.

Source FTSE RAFI UK Equity Income Physical UCITS ETF (DVUK)

Trailing yield: 4.3%

This is our pick of the UK dividend ETFs. Source’s product is relatively new on the market, having only launched in March this year. It takes into account four areas of a business: book value, value cash flow, sales and dividends. Like the other ETFs we discuss in this article, Source’s ETF focuses on the UK stock market.

While its approach does partially pick stocks based on headline yield, we like the additional financial sustainability screening – looking at profitability, lack of distress and accounting quality.

We have favourable views towards 18 of the top 20 stocks in the underlying ETF portfolio. The biggest is copper and coal miner Rio Tinto (RIO), representing 7.3% of the fund by weighting. Miners have been reducing debt over the past few years, streamlining operations and are now reaping the benefits of higher commodity prices – all boding well for cash generation and thus dividend capacity.

Other good names in the portfolio, in our view, include National Grid (NG.), Imperial Brands (IMB) and Aviva (AV.). The management fee is 0.35%.

TRAILING YIELDS vs PROSPECTIVE YIELDS

It is virtually impossible for retail investors to get dividend forecasts for funds, investment trusts and ETFs as the main financial websites don’t publish them.

Theoretically you could look at the underlying holdings – if they were all equities – and build a spreadsheet yourself using stock forecasts and weightings in the fund. But that’s a real faff and underlying weightings can change without you knowing, particularly with actively-managed funds.

As such, funds and ETF data will inevitably refer to trailing yields. You take the total amount of dividends (per share) paid over the past

12 months and compare it to the current share price.

For example, let’s say a fund paid 15p in two quarters and 30p in the other two quarters. That adds up to 90p per share in dividends for the whole year. The current share price is £19.60. (90/1960)*100 = 4.6% trailing yield.

Dividend forecasts are widely available for individual stocks. Prospective yields are an indication of the potential dividend income you could earn in the future.

The maths is the same as the previous example, albeit you substitute the 12 months’ worth of dividends that have ALREADY been paid with the amount of dividends that are FORECAST to be paid in the next year.

EARNING A DECENT INCOME FROM INVESTMENT FUNDS

MFM Slater Income Fund P (GB00B905XJ71)

Yield: 5%

Fund manager Mark Slater says his portfolio is roughly split equally into one third FTSE 100, one third mid FTSE 250 and the rest across the small cap and AIM market space. He only invests in companies with decent dividends yields, only dipping below the 4% yield when there is a high level of dividend growth on offer.

The fund screens companies on the basis of six areas: above-average yield; reliable and growing dividend stream; earnings growth prospects; cash flow; business quality; and balance sheet strength.

MFM Slater Income Fund is currently yielding circa 5% and the underlying portfolio has 6% to 7% prospective divided growth. The assets are a mix of growth style businesses, cyclical stocks and dividend stalwarts.

‘We have mitigated a lot of risk with the diversified approach re: the nature of the companies we invest in,’ says Mark Slater. ‘We are not overly concerned with the prospect of rising interest rates as we are not particularly exposed to “bond proxies” and the yield gap offered by the fund is very significant.’

Top holdings include life insurer Chesnara (CSN), shopping centre owner NewRiver REIT (NRR) and broadcaster ITV (ITV).

JOHCM UK Dynamic Y Inc (GB00BDZRJ218)

Yield: 4.1%

JOHCM UK Dynamic is not marketed or designed to be an income fund, yet it offers 4.1% yield thanks in part to the way the product is run.

‘Our strict discipline of only holding a stock if it pays a dividend, or is expected to do so within the next 12 months, does give the portfolio attractive yield characteristics,’ says fund manager Alex Savvides.

‘The companies we own in the portfolio are widely delivering on their strategies and improving their cash generation. This gives us confidence in the sustainability of the yield.’

The fund aims to profit from understanding and backing positive corporate change. It says the biggest risk to the fund’s performance typically occurs from these changes taking longer than expected and poor management of the underlying companies.

Top holdings include Vodafone (VOD), private equity investor 3i (III) and WM Morrison Supermarkets (MRW).

Premier Optimum Income Fund C (GB00B3DDDX03)

Yield: 7.8%

Approximately three quarters of the fund’s income comes from equity investments, claims fund manager Chris Wright. The remainder is generated by derivatives, namely selling call options. These give the right for a counterparty to buy a particular company share from Premier at a certain price within a certain period.

Despite being able to enhance the fund’s income, this strategy can act as a drag on capital growth in a strong rising market.

The fund is predominantly made up of UK equities including Royal Dutch Shell and housebuilder Berkeley (BKG), although it does have a few overseas-listed stocks including Italian utility Enel (ENEL:BIT) and French bank BNP Paribas (BNP:EPA).

Tritax Big Box REIT (BBOX)

Yield: 4.6%

Real estate investment trusts (REITs) must distribute at least 90% of their taxable income to shareholders as dividends each year. They can be a good source of income for investors yet you still have to think about the source of the earnings.

Anyone concerned about a Brexit-induced downturn in office block property prices may wish to avoid much of the sector at present. Tritax Big Box looks a bit different to most of its peer group and potentially fairly resilient.

It is the only listed REIT giving pure exposure to the pre-let development of very large logistics facilities in the UK. Its portfolio is filled by gigantic warehouses used by well-known companies including Amazon (AMZN:NDQ), Kellogg (K:NYSE), Tesco (TSCO), Rolls Royce Motor Cars and DHL.

‘Occupational demand continues to outweigh the supply of quality logistics buildings in the UK, particularly “Big Boxes”, and we expect rental growth to remain strong,’ says Colin Godfrey, fund manager of Tritax Big Box REIT.

‘Our assets deliver long-term income from institutional tenants, typically on long leases which have regular upward only rent reviews providing opportunities for income growth.

‘We seek to create value at acquisition through identification and negotiation of off-market deals (80% of assets acquired off-market). We also seek to deliver capital appreciation from active asset management to improve our assets and our leases.

‘Supply levels of UK logistics assets are at historically low levels. There are no new or high quality Big Box assets greater than 500,000 sq ft currently available in the UK. Contrastingly, demand remains strong.’

He adds: ‘Tenants typically make significant levels of investment into the bespoke fit-out and automation of these mega warehouses which, together with the long lease terms, underpins the importance of such assets to their ongoing operations.’

Threadneedle UK Equity Alpha (GB0B88P6D76)

Yield: 4.4%

The portfolio combines higher yielding investments with growth opportunities and special situations which tend to be companies trying to recover from specific setbacks or market challenges.

A good chunk of the underlying investments could see a share price re-rating if the trading recovery predicted by Threadneedle is achieved. As such, this fund could provide shareholders with a nice mix of both capital appreciation and income.

‘We believe in active management and our fund is driven by stock specific fundamentals,’ says fund manager Richard Colwell.

‘Examples of recent successes for the portfolio include Electrocomponents (ECM) and WM Morrison Supermarkets, both of which have gone through management change which we engaged with. These companies have their own levers to pull and are starting from low bases, which should allow them to improve results even in an uncertain macroeconomic environment.’

Top holdings include RSA Insurance (RSA) and British Gas owner Centrica (CNA).(DC)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.