Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineGB Group upbeat

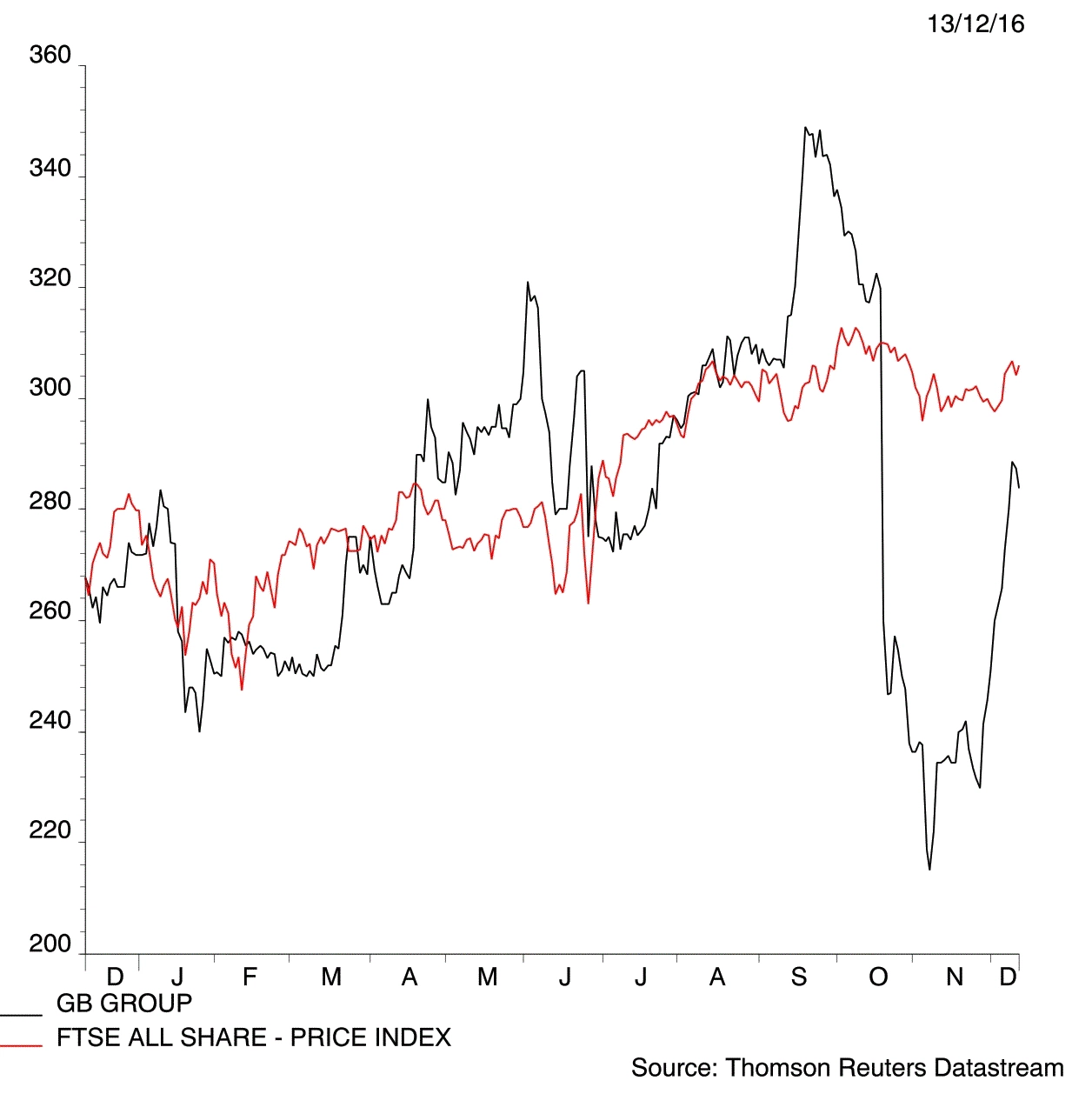

GB Group (GBG:AIM) 284p

Gain to date: 12.3%

Original entry point: Buy at 253p, 27 Oct 2016

Our GB Group (GBG:AIM) idea was always about getting in on a typically high quality company trading at an historically low valuation.

Slowing growth was the reason behind this anomaly and half year results on 29 November reflect that situation. Revenue increased 16% to £37.5m, 9% of that organically, playing through to a 15% rise in adjusted operating profit of £5.2m. You have to wonder how many other companies would be chuffed to bits with 9% organic growth but for GB this is a slow period.

Importantly, management appear very optimistic of a big second half performance recovery backed by recent changes in the US and European political landscape. These present new commercial opportunities in areas such as border control, anti-terrorism, fraud prevention and corporate data security.

It’s worth noting that investment bank Berenberg recently initiated on the stock with a 340p price target, roughly in line with the 350p we originally suggested. ‘We believe GB’s double-digit organic growth outlook remains robust,’ Berenberg’s analysts say, going on to stress their view that the magnitude of the sell-off was unjustified.

This is the very argument we used and the 12% gain since then bears this out. (SF)

Keep buying.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.