Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineHistory shows US stocks do well in the third year of a presidential term

The rapturous response offered by equity and bond markets to a lower-than-expected US inflation print last week (10 Nov) only served to reinforce the importance of the debate over whether or when the Federal Reserve and other central banks will pause or pivot on monetary policy.

The mere whiff of an easing in the rate of inflation is prompting speculation that central banks will swiftly take the opportunity to stop hiking rates and start cutting them again, so they can stave off (and do not get any blame for causing) a recession.

After a dismal 2022, when share prices have struggled and bond prices have been hammered, it is easy to see why markets are keen to latch on to any good news they can find. Investors with exposure to US assets will be particularly relieved as, at the time of writing, the price of the benchmark US 10-year Treasury is down by 19% in 2022 and the S&P 500 is down by 17%.

But investors will also be assessing the US political situation, for two reasons. First, the results of the mid-term elections may not be known until December, once the run-off for the Senate seat for Georgia takes place. Second, the US stock market has an uncanny habit of performing strongly in the third year of a presidential term – and in this electoral cycle, that means 2023.

POLLING POWER

Using the Dow Jones Industrials as a benchmark, the US stock market has risen by an average of 16.2% in the third calendar year of a presidential term across 18 presidencies going back to Harry Truman in 1948-1951.

This compares to the average single-digit percentage gains generated during the first, second and fourth and final years of a presidency.

The only year when the 30-stock Dow fell during the third year of a presidency was in 2015, during Barack Obama’s second stint in the White House.

The theory seems to be the incumbent president starts to pull out the economic stops and get the economy firing on all cylinders before they go for a second term, or at least try to lay the foundations for their successor’s campaign for the White House.

The Republicans are still hoping the mid-term elections give them control of both the House of Representatives and the Senate, but even then, history does not suggest such an impasse is seen as a negative outcome by investors in US equities.

Four of the six best third years for capital returns from the Dow came when the president, in the form of Richard Nixon, Bill Clinton (twice), Dwight Eisenhower and George W Bush, had to confront both a House of Representatives and a Senate that were under control of the opposition party.

Indeed, financial markets may welcome such checks and balances, in the view that any rash or egregiously foolish policies will be blocked by a logjam on Capitol Hill.

PAUSE OR PIVOT

However, politics alone is unlikely to shape the fortunes of the Dow Jones and America’s other leading equity indices, as the backdrop to the best (and worst) returns from the third year of a presidency suggests.

The 1975 bonanza under Nixon’s successor, Gerald Ford, came after the market collapse of 1973-74, while the surge under Bill Clinton in 1995 followed the Greenspan interest rates shock and mid-cycle growth pause of 1994.

In 2003 under George W Bush, the US was emerging from the wreckage of the technology bubble bust of 2000-2002 while in 1999 that bubble was expanding rapidly during the final half of Clinton’s second stint in office.

On the downside, Jimmy Carter’s third year was dogged by a fresh oil shock and another surge in inflation after the fall of the Shah of Iran, while the Black Monday crash of 1987 took the wind out of the sails of Ronald Reagan’s second term. US stocks fell for the only time during a third year of a presidency under Barack Obama in 2015. Global growth worries, after the bursting of a bubble in Chinese equities, Greece’s debt default and what proved to be a temporary halt in quantitative easing in the US combined to hold back the Dow and buck history at the same time.

Investors will therefore have to keep a close eye on events in Washington, but an even closer one on inflation, interest rates and corporate earnings growth, as well as valuation, which remains the ultimate arbiter of investment return. After the 1973-74 collapse and 1994’s stumble, US equities looked good value, at least with the benefit of hindsight, and unfortunately that may not necessarily be the case right now, even after 2022’s US stock market falls.

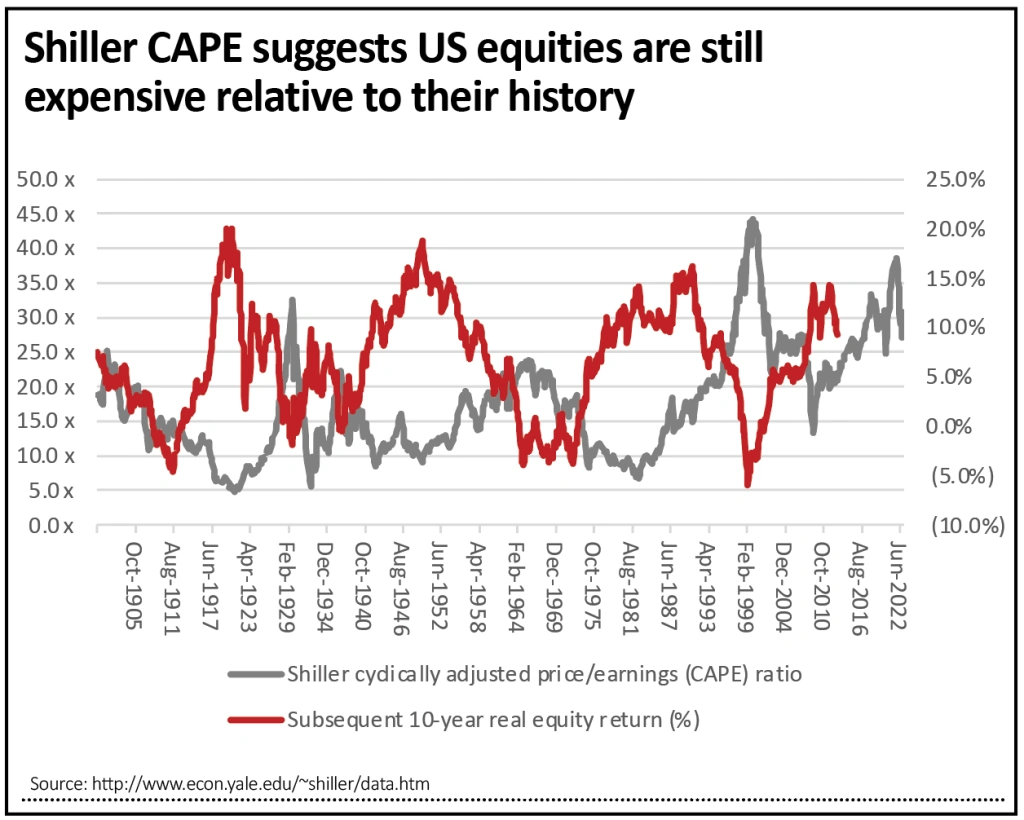

According to Robert Shiller’s cyclically adjusted price/earnings CAPE ratio, another major US index, the S&P 500, is still trading on more than 27 times earnings, a valuation multiple that has been historically commensurate with market tops and not market bottoms.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Feature

- Brighter outlook for chip equipment giant ASML triggers share price rebound

- Why convertible bonds can be an attractive alternative to shares

- US small caps: a savvy way to invest in a robust American economy

- What’s the latest for UK investors holding Russian stocks and funds?

- Slump in net asset value at Scottish Mortgage raises some big questions

- Six UK stocks to buy now: markets are starting to recover

Great Ideas

News

- Walmart beats forecasts and raises guidance on market share gains

- Warren Buffett ditches Procter & Gamble for Asian tech group TSMC

- Agricultural sector suppliers continue to harvest tasty gains

- FTX collapse hurts shares in Microstrategy and Argo Blockchain

- Black Friday sales expected to fall as consumers cut back on spending

- Bill Ackman: why we might see a stock market recovery in late 2023

- How Energean has been fired up by first gas from Israel and strong prices

- Why Tesla’s big share price fall isn’t just about Twitter