Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineMomentum investing: when to buy a winning stock

One of the oldest sayings in the stock market is ‘the trend is your friend’, which means if a share price has been rising for some time, all else being equal, it’s likely to continue rising for the foreseeable future. Likewise, if it’s been falling for some time, it will likely keep falling until the news flow or sentiment changes.

In this article we explain how buying stocks that hit a 12-month high can be a winning strategy. While there are no guarantees of success, history suggests it can work a lot of the time.

It is important to stress this method is different to the normal long-term investment strategy of analysing fundamentals and it won’t suit everyone.

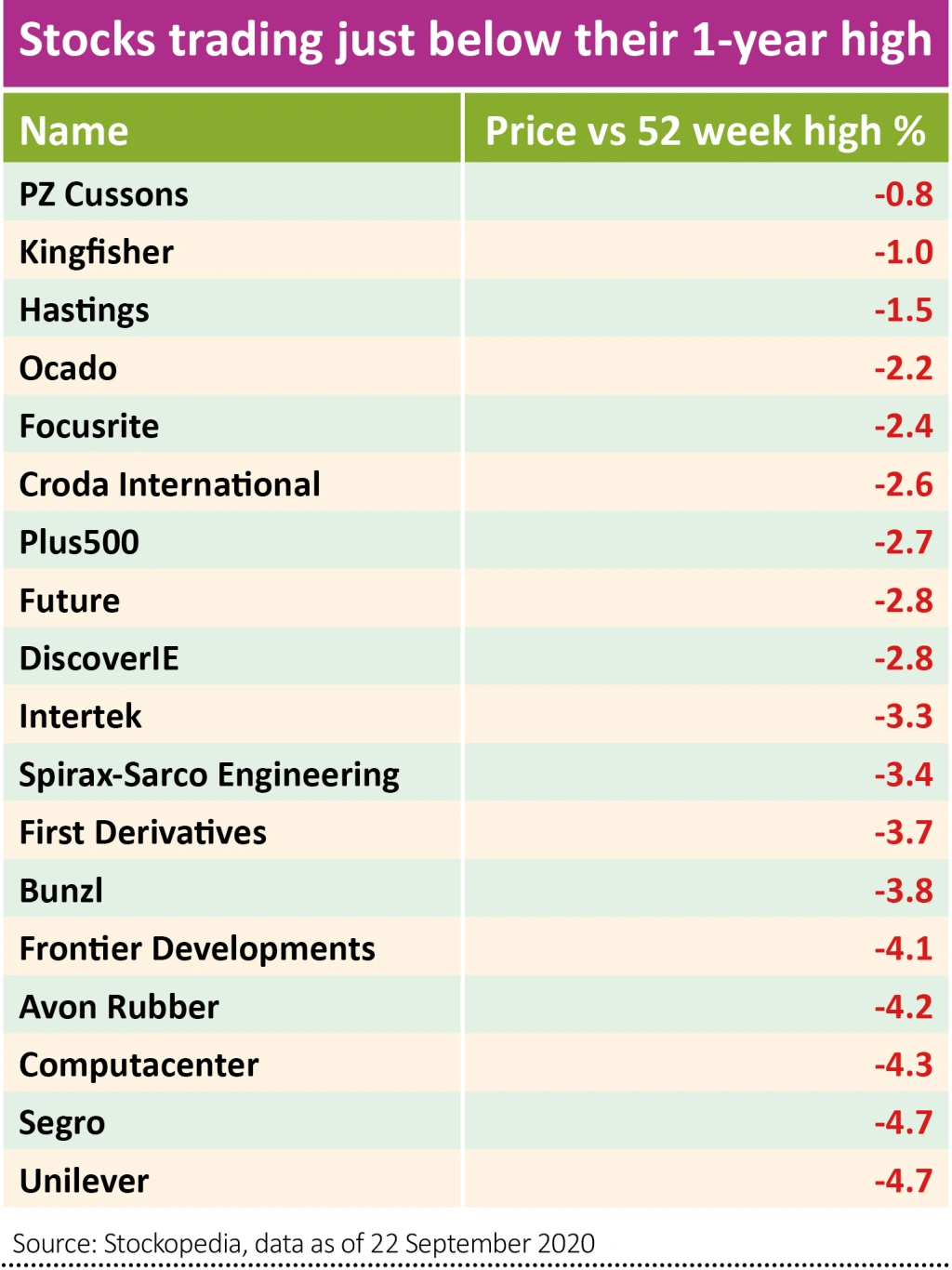

Momentum investing is a proven way of making money from the markets. Read on to learn more about this approach and to find out which stocks are approaching a 12-month high, thereby giving you a head start in finding potential investment opportunities using this strategy.

A simple momentum strategy

This technique means you latch onto winners and the exit strategy means you’ve exhausted the full extent of the uptrend without selling out early. The downside is that this strategy can involve high turnover and trading costs.

IT’S BEEN DONE FOR YEARS

The idea riding a rising trend isn’t new. In his book on behavioural finance, Daniel Crosby cites an 1838 account of the successful trading strategy of economist David Ricardo: ‘Mr Ricardo amassed his immense fortune by a scrupulous attention to what he called his three golden rules. Never refuse an option when you can get it, cut short your losses, and let your profits run on… By letting profits run on he meant that when prices were rising, he ought not to sell until prices had reached their highest and were beginning to fall.’

Letting winners run is sound advice but the temptation to sell is strong and knowing when a share price has reached its peak and is about to fall is fiendishly difficult, if not impossible.

MOMO OR FOMO?

Private investors are repeatedly told not to chase performance, and few professional managers would admit to using a momentum strategy, yet it’s a fact that price trends – both up and down – can continue for much longer than most of us expect.

Watching other people getting rich as prices go up while you sit on your hands waiting for a pullback in the market is one of the most frustrating aspects of investing and one of the biggest drivers of price momentum.

The fear of missing out means that each time a stock or an index makes a new high, more investors buckle and are pulled in from the sidelines, creating more demand, which leads to higher prices and so on.

Whereas growth investing needs little explanation, and value investing is buying with a ‘margin of safety’ in the hope of mean reversion, momentum investing is counter-intuitive because it means buying shares as they make new highs, or at least running your winners way past your comfort zone, in the hope of exploiting the delay before mean reversion occurs.

At its most extreme, momentum investing can turn into a mania as it did during the South Sea Bubble in 1719-20, on Wall Street in the late 1920s and in the tech bubble of the late 1990s, all of which were ultimately the result of momentum investing. Collective fear of missing out, combined with greed, pushed stock valuations to levels that were unsustainable.

‘MAKING MORE ON THE STRAIGHTS’

Given that picking precise inflection points is almost impossible, many momentum investors are happy to jump aboard a trend well after it has become established and ride it beyond its peak because they know that by sticking with the trend for longer and not selling out early they will capture more of the upside and outperform their peers.

As one momentum manager explained, by staying invested for the full duration of the trend and not selling until prices have started to fall, ‘we make more on the straights than we lose on the curves’.

Of the five classic factors used in investing – value, size, profitability, beta and momentum – momentum has the best long-term track record, even if there is no fundamental basis for it to work so consistently.

As the fathers of the efficient market hypothesis, Eugene Fama and Ken French, put it: ‘The premier market anomaly is momentum. Stocks with low returns over the past year tend to have low returns for the next few months, and stocks with high past returns tend to have high future returns.’

EXPERT OPINION

Given this anomaly, it’s no surprise that there has been a great deal of academic research into exactly why investing with a momentum strategy is so successful.

In a paper written in 1967 called Relative strength as a criterion for investment selection, Robert A. Levy showed that buying stocks with prices which were substantially higher than their average price over the previous six months produced ‘significant abnormal returns’.

In their paper of 1993, Returns to buying winners and selling losers: implications for stock market efficiency, authors Narasimhan Jegadeesh and Sheridan Titman analysed the performance of US stock returns between 1965 and 1989. Their study found that momentum was indeed a significant factor, capable of generating outperformance of as much as 1% per month, but it wasn’t a permanent driver of share prices.

A portfolio constructed on the basis of returns realised over the previous six months, as per Levy’s suggestion, generated an average cumulative return of 9.5% over the next 12 months, but lost more than half of this return in the following 24 months.

A 2008 paper by Elroy Dimson, Paul Marsh and Mike Staunton called 108 Years of Momentum Profits looked at stock returns in the UK market from 1900 to the end of 2007 and found that the premium or outperformance of momentum was substantial, not just across the whole market but even more so within certain sub-sets of the market.

‘Momentum, or the tendency for stock returns to trend in the same direction, is a major puzzle,’ they admitted. ‘In well-functioning markets, it should not be possible to make money from the naïve strategy of simply buying winners and selling losers. Yet there is extensive evidence, across time and markets, that momentum profits have been large and pervasive.’

Moreover, Dimson, Marsh and Staunton showed that a portfolio of momentum winners, comprising of stocks within a top given percentage of returns, consistently beat a portfolio of losers when held over a period of anywhere between one month and 12 months, meaning buying winners and selling losers was a profitable and self-financing strategy.

MOMENTUM WORKS BOTH WAYS

Just as positive momentum begets more positive momentum, pulling in buyers from the sidelines desperate not to miss out on gains, so negative momentum has the same effect as investors scurry to avoid losses.

Just as we tend to sell our winners too early, we tend to hold onto our losers too long in the hope that they will get back to where we bought them and we can exit scot-free.

However, simple mathematics means that if a stock has fallen 25% it needs to rally 33% to get back to break-even. If it falls 50%, it needs to double to get back to break even, which is highly unlikely. Yet plenty of stocks which have lost 25% go on to lose 50%, inflicting heavy losses on shareholders. We just don’t seem to learn from the experience.

At this stage it’s worth remembering one of the oldest market adages, ‘the first cut is the cheapest’. Investors who cut their losses early typically outperform those that don’t. As the stock price keeps falling, more investors end up throwing in the towel and selling, which can have the effect of depressing the share price, prompting more selling and creating a downward spiral.

It’s precisely this type of behaviour which leads to panics and crashes as investors – aware that their gains are only paper profits until they try to sell their shares – rush for the exit when markets get the jitters as they did in late 2018 and earlier this year.

MOMENTUM IS EVERYWHERE

As Dimson, Marsh and Staunton point out, almost all investors – wittingly or unwittingly – employ momentum in their investment style. Those who window-dress their portfolios at the end of the financial year, clearing out losers for example, ‘are de facto momentum traders’.

Whether they like it or not, institutional investors are also momentum traders. They are evaluated relative to a size-based benchmark, such as the FTSE 100. In this example, they tend to buy stocks as they drift above the size threshold for large cap index membership, and to sell those that drift below the size threshold; they unwittingly benefit when there are momentum effects in the market.

The effect of momentum in the S&P 500 index is obvious for all to see. As a handful of the biggest stocks keep outperforming and become a bigger proportion of the index, so investors who are benchmarked against the index have to keep increasing their position sizes or risk falling behind in performance terms. This creates concentration risk, which in turn creates volatility as we have witnessed this year.

IDENTIFYING UK MOMENTUM STOCKS

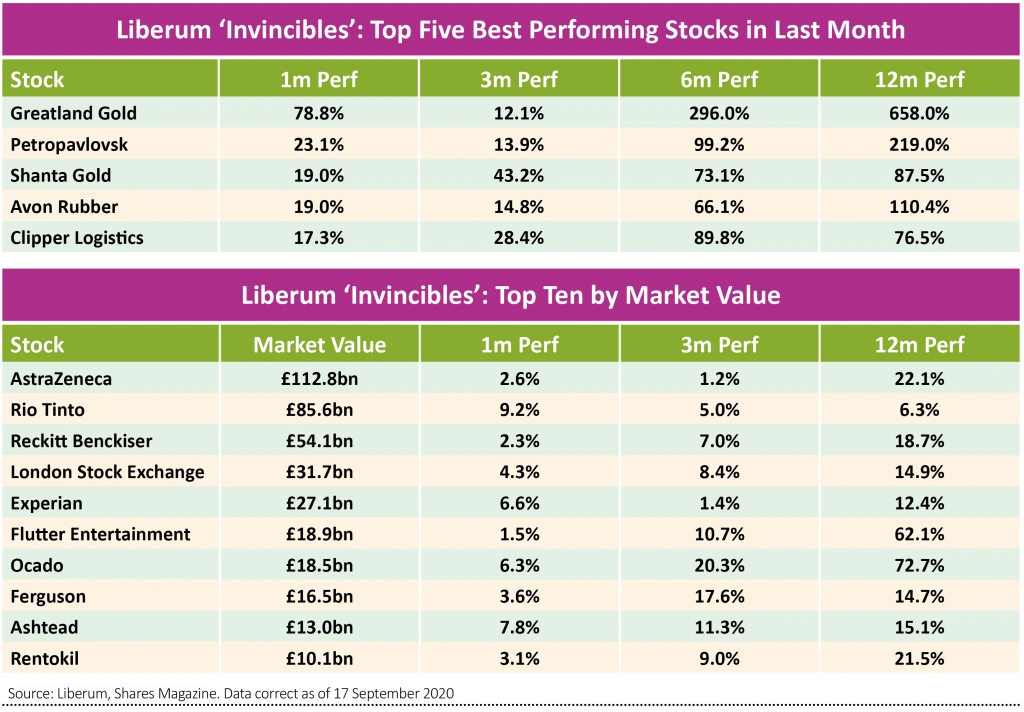

In May of this year, analysts at investment bank Liberum created two baskets of UK and European stocks with positive price momentum over the previous one, three, six and 12 months.

The baskets, made up of stocks the bank nicknamed ‘Invincibles’, were dominated by cyclical companies including miners, business services, capital goods and software.

In the four months from their inception, the baskets have outperformed their respective benchmarks for three months running as of 17 September and more importantly generated positive absolute returns every month, including June and July when the market posted negative returns.

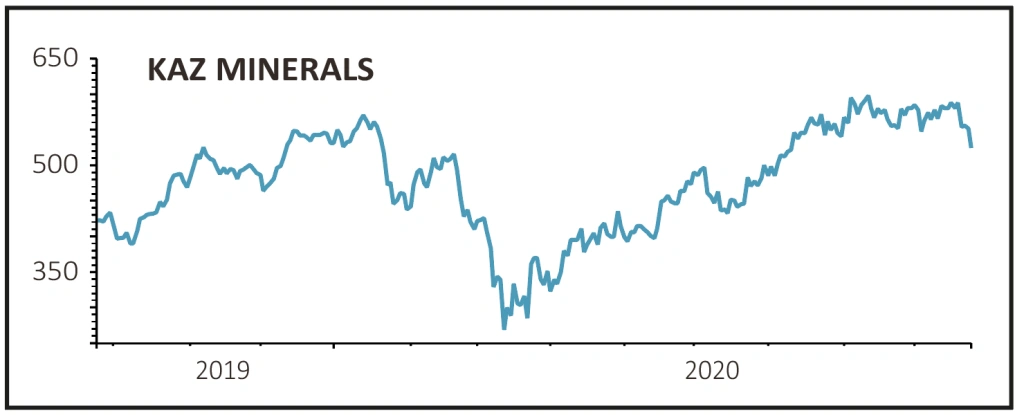

Drilling down into the constituents of the UK basket, miners Shanta Gold (SHG:AIM) and KAZ Minerals (KAZ) have been top performers for a while.

Two thirds of the stocks in the UK basket are miners: half are platinum or gold miners while the other half are mostly copper miners, which suggests that copper and gold are driving the rally in materials.

A second group of stocks with strong momentum are software companies such as Keywords Studios (KWS:AIM).

A third group consists of capital goods stocks, which suggests investors are betting the current cyclical recovery lasts – backed up by Liberum’s ‘Early Cycle Indicator’ – and we don’t get a repeat of the global shutdown which impacted both output and demand for industrial goods in the second quarter.

Re-running the screen in September produced a sharp increase in the number of UK stocks qualifying for inclusion, from 56 in August to exactly double that number. Liberum put the spike down to ’the sideways movement of stock markets in June and July’ meaning many companies posted slightly negative returns, while the upward momentum of September meant performance turned positive and stocks re-entered the list.

This exercise throws up one of the biggest drawbacks of momentum investing – turnover. Typically, building a momentum portfolio involves high turnover over short periods of time which can lead to higher costs and lower profits.

BEWARE MEAN REVERSION

Besides the high concentration of cyclical stocks, there was no obvious size bias in the Liberum screen towards large cap, mid cap or small cap companies, nor was there a statistically significant ‘quality’ bias in terms of trailing 12-month return on equity.

In fact, several stocks had double-digit negative returns on equity, including familiar names such as online grocery retailer Ocado (OCDO).

Instead there was a marked bias towards highly priced stocks, with only a handful of companies trading on trailing 12-month price to earnings (PE) ratios of less than 10, and the average PE of the basket was somewhere between 20 and 30.

This is because positive momentum forces prices upwards even when earnings are static, a phenomenon known as PE expansion.

However, in stock markets as in business, the ultimate cure for high prices is high prices. As Jegadeesh and Titman suggest: ‘Investors who buy past winners and sell past losers move prices away from their long-run values temporarily and thereby cause prices to overreact.’

The further prices deviate from their long-run values, and the more stretched PE ratios become, the greater the risk of disappointment and sudden losses as share prices – and therefore valuations – revert to their long-run mean.

As Dimson, Marsh and Staunton conclude, momentum portfolios tend to have ‘a marked exposure to outperforming and underperforming sectors and involve taking positions in companies that have been in the news for their deviant performance. They buy (belatedly) into appreciated stocks, and avoid the losers that are sought by contrarian investors hoping for a reversal. The momentum portfolio would be unsuitable for individuals of a nervous disposition.’

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.