Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineTech and gold: is Warren Buffett stepping back at Berkshire Hathaway?

Cloud-based data warehousing technology firm Snowflake listed in the US on 16 September in the biggest ever software initial public offering (IPO), with its shares up 111% on the first day of trading, valuing the company at £96 billion.

Given investor appetite for cloud-based businesses, perhaps this wasn’t too surprising even though the average first-day rise for an IPO has historically been 16% according to a study by University of Florida professor Jay Ritter.

The real surprise is the involvement of Warren Buffett whose Berkshire Hathaway investment vehicle purchased a $570 million stake in Snowflake.

It was surprising for various reasons, not least because only four years ago Buffett said in 54 years, Berkshire has ever bought into an IPO.

His disdain for buying companies when they first list was made clear during the dotcom bubble of the late 1990s when he commented: ‘A bubble market has allowed the creation of bubble companies, entities designed more with an eye to making money off investors rather than for them.’

NOT KNOWN FOR TECH

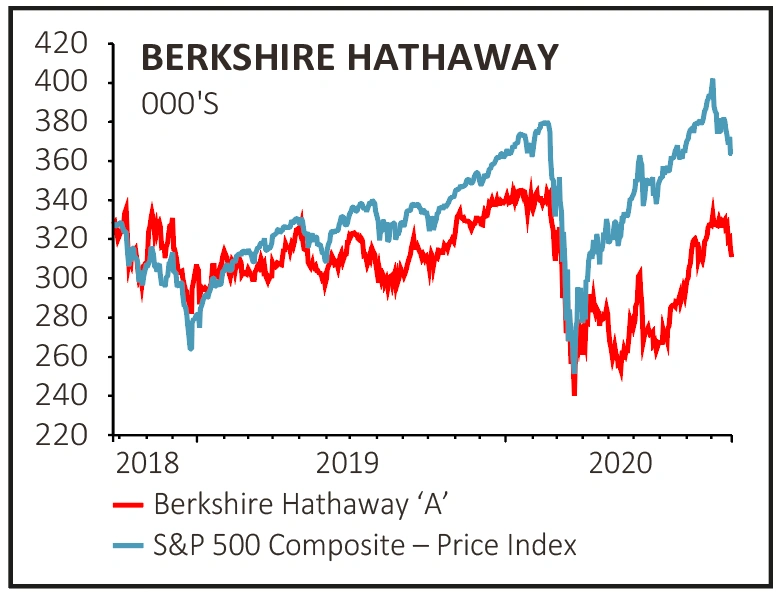

Observers have previously called into question Buffett’s investing acumen, citing his refusal to buy technology stocks, and instead sticking with old economy firms, which last year caused Berkshire to underperform the S&P 500.

Despite being a close friend of Microsoft founder Bill Gates, who sat on the Berkshire board for 16 years, Buffett has until recently resisted the temptation to own technology businesses.

Buffett’s rationale is simple; he claims he doesn’t understand technology as well as his beloved insurance businesses and one of his core investing principles is to stick to areas of known expertise, or what he calls a ‘circle of competence’.

He once quipped: ‘If you don’t know who the patsy is at the poker table after observing a few hands, the chances are, you are the patsy.’

BREAKING THE RULES

Snowflake is less than a decade old and has made cumulative losses of over $870 million since it was founded, in stark contrast to some of Berkshire’s long-term holdings such as Coca-Cola which has 122 years of pedigree and has cumulatively made billions of profits.

Maybe Buffett was swayed to some degree by the huge success of Berkshire’s investment in the IPO of Brazilian e-commerce and digital payments firm StoneCo two years ago.

Berkshire spent $340 million to purchase an 11% stake despite the company being unprofitable at the time. Today that stake is worth close to $700 million and last year StoneCo reported profits of $150 million. Still, priced at over 100 times this year’s expected earnings, it is hardly a value proposition one would associate with Buffett.

Another un-Buffett-like characteristic is the fact his latest investment, Snowflake, operates in highly competitive markets with large established rivals such as Amazon’s web services division AWS which has deep pockets. Snowflake certainly doesn’t appear to easily fit with Buffett’s preference for businesses with strong economic moats.

INVESTORS MIGHT BE LOOKING IN THE WRONG PLACE

Perhaps observers are attributing the two technology investments to Buffett when in fact they originated from his two investment lieutenants Todd Combs and Ted Weschler, the former hedge fund managers that Buffett hired to look after parts of Berkshire’s portfolios.

In addition to managing money both Combs and Weschler sit on company boards where Berkshire holds significant stakes. Over the last decade they have increasingly influenced Buffett’s investments.

For example, Buffett credits Combs with Berkshire’s $32 billion acquisition of Precision Castparts admitting he had never heard of the company before Combs brought it to his attention.

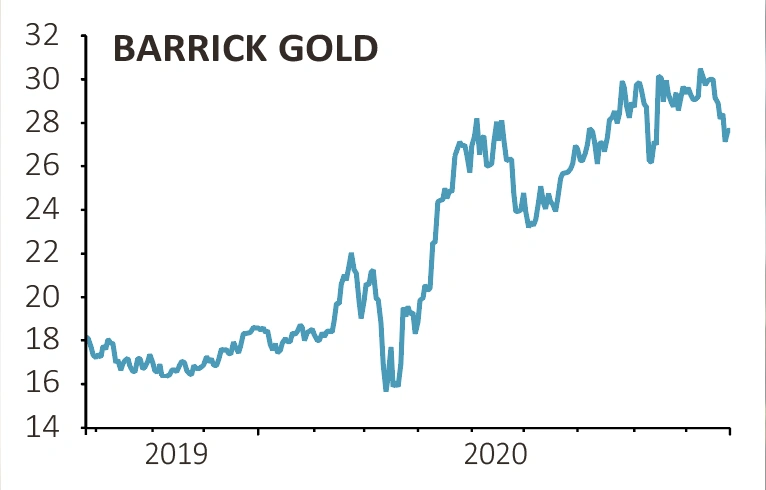

BANKS OUT, GOLD MINING IN

It could be the same story with the news that Berkshire had sold its holding in Goldman Sachs and trimmed back most of other its bank holdings, albeit adding to its Bank of America position. It has recycled some of the proceeds into buying shares in precious metals miner Barrick Gold.

In the past Buffett has been dismissive of the idea of holding the yellow metal saying: ‘Gold gets dug out of the ground in Africa… Then we melt it down, dig another hole, bury it again and pay people to stand around guarding it. It has no utility. Anyone watching from Mars would be scratching their head.’

While Berkshire hasn’t purchased gold explicitly, the fortunes of Barrick are intimately tied to the price of gold and how much profit it can turn by digging the stuff out of the ground.

Some observers have noted an increase in the number of small portfolio changes for Berkshire in recent months, something more akin to traditional portfolio management actions rather

than Buffett’s ‘buy and hold’ style of investing.

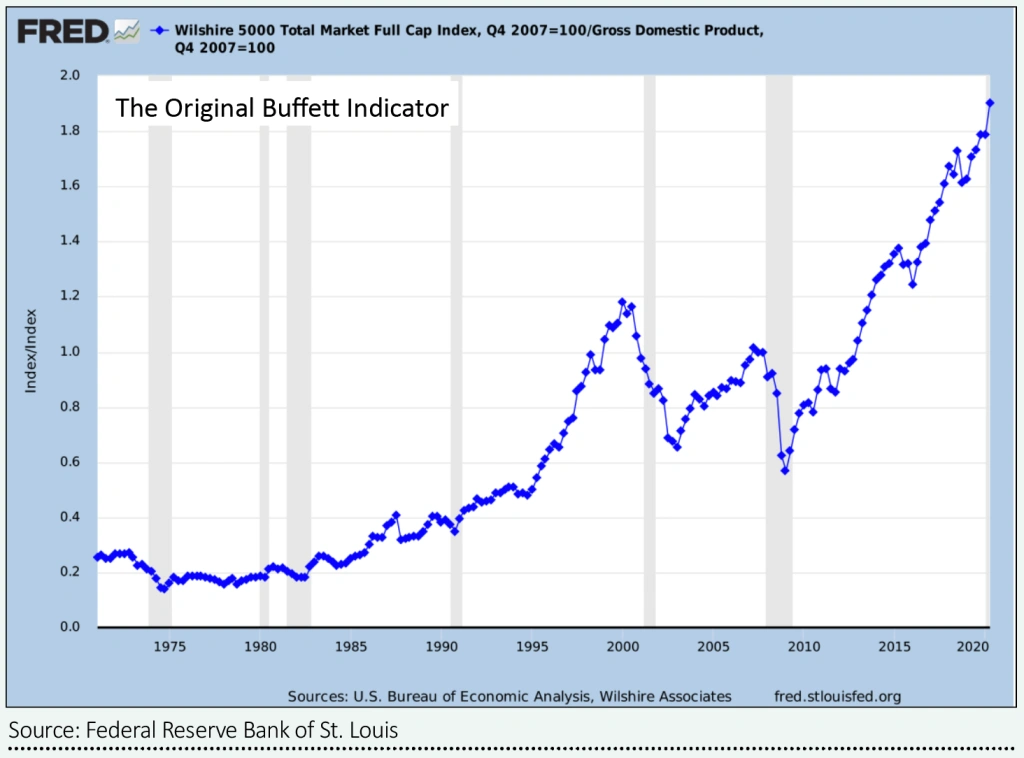

THE BUFFETT INDICATOR

Buffett doesn’t often make comments of the US stock market or talk about valuations at the macro level, but 1999 was one such time when he warned investors that the market was looking expensive.

He said stock returns would struggle to keep providing double-digit returns as they had in the prior decade. He referenced a ratio that has since become known as the Buffet indicator.

The investor caveated his analysis by saying that valuing the market was not the same thing as predicting it. Buffett described a measure which he thought was the best single measure of where valuations stand at any given time.

| The Buffett indicator = The total market value of all US stocks as a ratio of gross domestic product (GDP). |

In 2000 the ratio reached 1.2 times, way above the 0.85 times historical average. Today the same ratio sits at 1.8 times, 50% higher than the 2000 level.

The premise behind the ratio is that over time corporations in aggregate cannot grow faster than the economy, so the higher the market goes relative to the size of the economy, the more expensive stocks become.

CLASSIC BUFFETT

Berkshire recently invested $5 billion into five of Japan’s large quoted trading houses, taking a 5% stake in each of Mitsubishi, Marubeni, Sumitomo, Mitsui & Co and Itochu.

Nick Schmitz, analyst at hedge fund Verdad, has calculated that collectively Buffett’s Japanese investments trade at a 30% discount to the broader Japanese Topix index and a 79% discount to the S&P 500, on a price to book basis.

The dividend yield on these companies is around three times higher than the US market and double the Japanese market.

In addition to trading below book value, Bloomberg analysts reckon the combined group produce annual free cash flow yields of around 10%. With interest rates stuck close to zero that looks like a bargain. Having taken around a year to build the stakes, Berkshire has indicated that it is in it for the long haul.

What the recent flurry of activity at Berkshire shows is that it is becoming more difficult to separate the investment decisions of Buffett from those of Combs and Weschler.

Investors may have to get used Berkshire making different types of investments to the past as the pair take on even more responsibility. After all, last month Buffett turned 90, becoming a nonagenarian along with his long-time business partner Charlie Munger.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.