Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThis defensive growth fund is very appealing

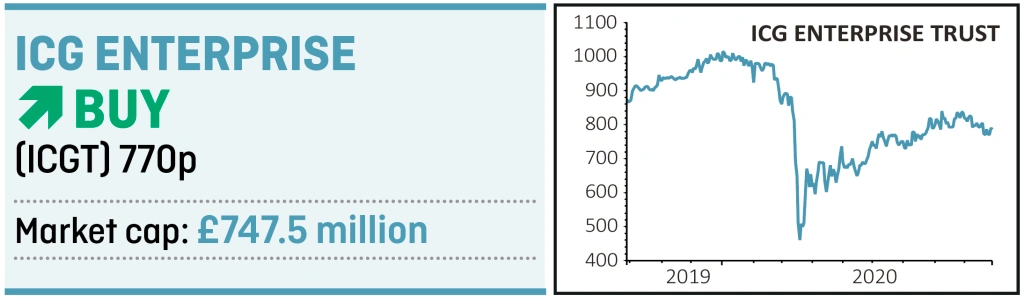

The 29.2% discount to net asset value at ICG Enterprise (ICGT) represents an excellent opportunity to gain targeted exposure to the private equity space.

The trust has typically traded at a discount to reflect its exposure to unlisted assets which do not have a daily market value. However, given its long-term track record and a compelling strategy the current gap between the NAV and share price looks anomalous.

In early 2017 the running of the fund was handed to specialist asset manager Intermediate Capital Group (ICP) which has more than €34 billion in assets under management and a footprint in more than 14 countries.

While the overall returns from private equity have been strong, as Intermediate’s head of private equity fund investments Oliver Gardey explains, there is quite a big difference in the showing of top tier funds and bottom tier funds.

To reduce levels of risk ICG focuses on buyouts, where an underperforming or undervalued company is bought to be turned around, rather than areas like venture capital or distressed debt where the risk of loss is higher.

There is also an emphasis on mid-market and larger deals in developed markets and, applying the experience gathered over its near 40-year existence, the really top managers.

Nearly a quarter of ICG’s portfolio is in the healthcare and education space, with a further 16% in consumer goods and services, and 15% equally in industrials and TMT (tech, media and telecoms).

The trust’s ‘secret sauce’, as Gardey describes it, is that it invests directly in some high conviction ideas alongside the private equity managers with whom it places its money.

To qualify for investments, companies must be profitable, have a strong competitive position, growth drivers unlinked to the economy, high recurring revenue, high margins, strong cash flow and low customer concentration.

Gardey sums this up as ‘defensive growth’ and says it encompasses areas like healthcare, business services and software as a service.

In the 12 months to 31 January 2020 the investment portfolio saw returns of 14.6% in sterling terms, with £149 million worth of realisations or sales from the portfolio at an average uplift of 37% to book value.

Covid had an impact but first quarter performance was resilient with net asset value down 4.1% compared with an 18.8% decline in the FTSE All-Share over the same period.

Gardey says the trust has sufficient liquidity to go two years without any realisations from the portfolio, a scenario he suggests is extremely unlikely. The ongoing charge of 1.37% is not exceptionally high given the extra costs and complexity involved in managing a private equity portfolio.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.