Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineA bidding war looks unlikely for William Hill

Investors went full tilt on 25 September when they pushed William Hill’s (WMH) shares up 44% to 312p after the company confirmed it had received separate takeover interest from private equity group Apollo and gambling business Caesars Entertainment.

The enthusiasm proved short-lived and on 28 September Caesars tabled a 272p all-cash proposal. The shares sank 12% to 272p, adjusting to Caesar’s potential takeout price. A day later William Hill’s board recommended a formal offer.

Even if shareholders were to hold out for a higher price the possibility of a bidding war has been effectively quashed by Caesars saying it would terminate its joint venture with William Hill should it be taken over by Apollo.

William Hill owns 80% of the joint venture, which includes a 25-year partnership and a profit share on Caesars’ retail sports books.

There is much to play for with Caesars estimating that the enlarged US sports and online gaming group could generate between $600 and $700 million of net revenues in the 2021 fiscal year.

Analysts at Shore Capital believe the 272p per share offer low-balls the potential value of William Hill’s share of the US business which they calculate is worth at least 300p based on a long-term market share of 15% with another 100p thrown in for the non-US businesses.

Jefferies analyst James Wheatcroft notes that only the William Hill board have so far given support to the takeover, with no letters of intent from big shareholders which suggest the latter are hoping for a better price.

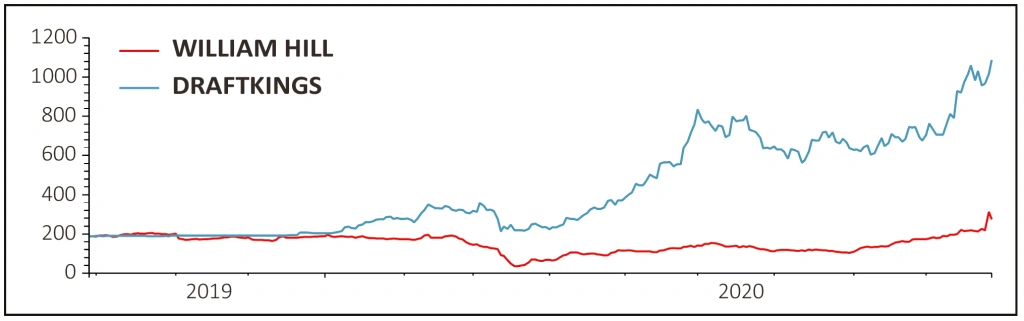

The potential market opportunity in the US which some analysts put at between $30 billion to $35 billion has not been lost on stateside investors whose recent enthusiasm for gambling stocks can be seen in the five-fold increase in the shares of fantasy sports betting group Draftkings since coming to the market last year.

It now sports a market capitalisation of $19 billion despite only having revenues around $520 million while it is still loss making.

UK gambling stocks have so far missed out on the party, but the arbitrage opportunity is clear and might explain the interest of private equity in William Hill, looking to unlock value through buying the group and then floating the US business separately. But William Hill is in the driving seat and could achieve this outcome itself.

As Shore Capital says: ‘For Caesars, a cash purchase, a subsequent merger of US sports and iGaming assets, followed by an eventual demerger of these assets could help unlock significant value.’

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.