Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWill markets race higher after the St. Leger?

It has been a strange year for so many industries and thoroughbred breeding and racing has been no exception.

Spectators have been barred from racecourses and major meetings have been moved from their traditional calendar slots.

Some American punters will be wondering why they bothered with the 146th Run for Roses as hot favourite Tiz the Law lost but British fans can at least look forward to the 224th running of Doncaster’s St. Leger on its usual date, the second Saturday of September (12 Sep).

It will not just be betting shop punters who will be keeping an eye on the event.

The staging of the race traditionally marks an end to the summer lull in financial market trading, at least according to the old adage ‘sell in May, go away and come back again on St. Leger day’.

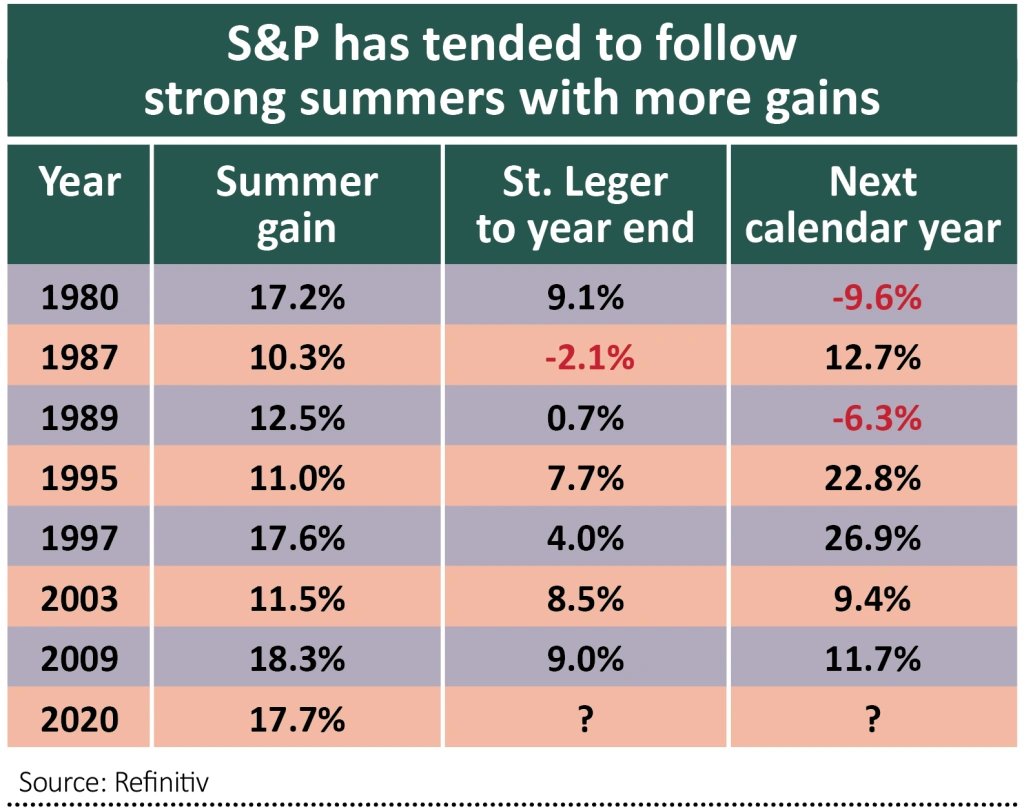

This saying is based upon how, on average, the UK’s FTSE All-Share index has historically done best between January and April and then again after mid-September, with summer being a bit quiet by comparison. A similar, if less pronounced pattern, can be seen in America’s benchmark S&P 500 index.

Despite the overall averages, this pattern is not visible every year (investing would be far less difficult if it were). The FTSE All-Share has risen through to the end of April, dropped through to mid-September and then gained until the end of a year on just 15 occasions since 1965. The S&P 500 has followed this trajectory just eight times over the same period.

In 2020, the FTSE All-Share is pretty much flat since 1 May, in keeping with historic averages, although the S&P 500 has actually gained 17.7%, its second-best showing over 56 years of data. This begs the question of what those respective indices will do for the rest of the year (and then beyond), in the wake of a trends-busting summer on one side of the Atlantic and perfectly normal one on the other.

HISTORY LESSON

The S&P 500 has actually gained ground on 34 occasions and lost it on just 17 between 1 May and Britain’s St. Leger day (an event that is unlikely to resonate Stateside anyway). However, it has made a double-digit percentage gain just seven times.

The good news for investors is – at least if history is any guide – the final third of the year saw further advances six times, against just one drop, and there were five gains against just two declines in the following calendar year.

Bears will point out that those following-year declines came in 1981 and 1990, when a recession hit America.

As such, rather than points in the calendar, much will depend on how the ongoing pandemic develops and its effect upon the wider economy and corporate earnings and cash flow, as well as central banks’ policy response and how that in turn influences investor thinking.

Even after last week’s stumble, caused by the very same technology stocks which did so much to drag the index higher in the first place, many investors will take a little comfort from how well the S&P has done historically after a strong summer.

Sceptics will counter by saying this is too short a time horizon. The compound annual growth rate (CAGR) in the S&P 500 over the past decade is 12.1% and it is 17.7% for the NASDAQ, levels which have historically preceded a decade of poor (or at least diminishing) returns, so perhaps would-be dip-buyers need to tread carefully after all, depending upon their time horizon.

CONTINENTAL SHIFT

The UK has the additional complication of Brexit to address, especially as the UK Government is sticking to its hard line in negotiations with the EU, which perhaps continues to underestimate the Johnson administration’s determination on this topic and its own ability to get 27 members to agree to a plan of their own.

You could argue that the uncertainty over what Brexit may or may not mean – whether you approve of it or not – is one reason why the FTSE All-Share has lagged its global peers so badly since June 2016. Investors just don’t know what will come of it and perhaps they are (still) taking evasive action accordingly.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.