Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

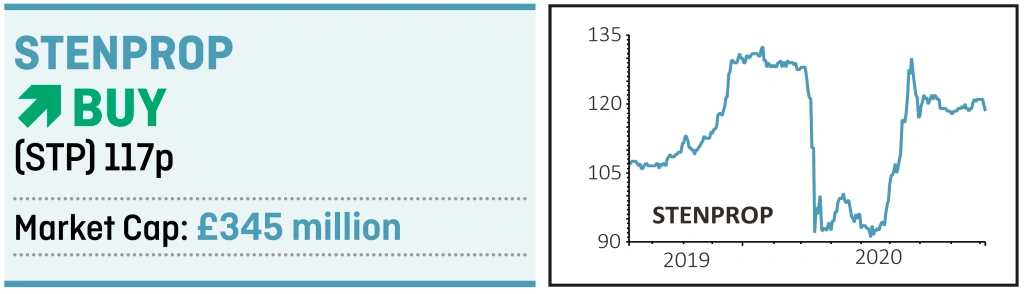

magazineIndustrial property play Stenprop is going cheap

Unlike much of the property market the industrial space has performed strongly of late as it benefits from trends accelerated by Covid-19. The downside for investors is that vehicles owning this type of asset have become increasingly expensive.

However, Shares has spotted an opportunity in Stenprop (STP), a UK industrial property investor which trades at a 10% discount to net asset value (NAV) and yields 5.8%. In comparison, industrial-focused Segro (SGRO) and LondonMetric Property (LMP) trade at 30% and 40% premiums to NAV respectively.

In 2018 Stenprop announced plans to focus almost exclusively on multi-let industrial (MLI) sites. These aren’t the big distribution warehouses owned by the likes of Segro and Tritax Big Box (BBOX); instead they are estates with modern purpose-built and often modest-sized industrial units located in urban areas with strong local transport links. Tenants include a craft brewery and a business which carries out photography for online retailers.

The fundamentals of this market are attractive because hardly any new units are being built. The design of these industrial structures has also not changed in 30 years, so unlike other types of asset there is less risk of them becoming obsolete.

While big boxes are often let to a single tenant the rental income from MLI is diversified. Dealing with such a large number of tenants is a challenge but Stenprop’s in-house asset management platform supports efficient marketing, leasing and enables the company to offer other services to tenants such as insurance and maintenance, and thereby generate ancillary revenue.

The real estate investment trust recently agreed to buy assets in Norwich and Glasgow for £19.6 million and £5.5 million respectively, and is offloading other types of property such as retail and care homes. The goal is to be 100% multi-let industrial by 2022, versus the current 60% level.

Heading into a recession the exposure to smaller businesses is a risk to weigh. Yet rents on these units are relatively low, often representing a modest amount of a tenant’s turnover.

The resilience of the portfolio was reflected in a recent trading update showing improvements in MLI occupancy to 92% (as of 30 June) and with 93% of rent collected for Q2 and 84% for the first three weeks of Q3.

The company has a strong balance sheet with available cash of £40 million as at 22 July and a loan-to-value of 32% once these funds are factored in.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.