Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineFinding alternative sources of income in retirement

Investors in retirement looking for reliable income have been frustrated with large parts of the equity market in 2020 as companies defer, cancel or reduce dividend payments. This could have created a shortfall in their precious income, causing them to look at other asset classes in the search for yield.

An alternative place to equities for income is the debt and loans sector, albeit investors with limited experience may not feel as comfortable looking for opportunities in this space compared to analysing individual company shares.

If that is the case, investors might want to consider actively managed investment trusts and funds as an easier way to gain exposure to the debt and loans sector than trying to invest directly, particularly as they can provide exposure to investments restricted to institutional investors. Fund managers do the hard work selecting assets and managing the portfolio.

To help readers appreciate how fund managers find opportunities in his space, we now look at 5.1%-yielding Henderson Diversified Income Trust (HDIV) as an example of how investment trusts in the debt and loans sector operate, examining its strategy both during the pandemic and over a longer timeframe.

PERFORMANCE RECORD

The trust has a track record of outperforming its category benchmark, delivering annualised net asset value total returns of 6.2% over five years and 7.2% over 10 years (to 1 September 2020), according to Morningstar. This compares to 3.2% annualised returns over five years and 5% over 10 years for the Morningstar investment trusts debt (loans and bonds) category.

The category is used as a measure of performance against peers and Henderson Diversified Income Trust sits second out of 14 funds over three years and fifth out of 13 funds over five years.

The share price performance is slightly behind the NAV with 4.5% annualised returns over five years and 6.8% over 10 years.

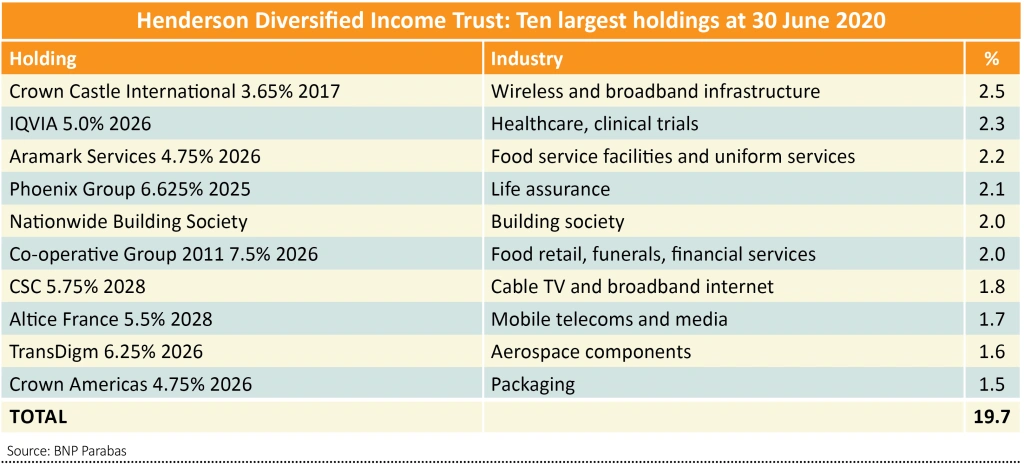

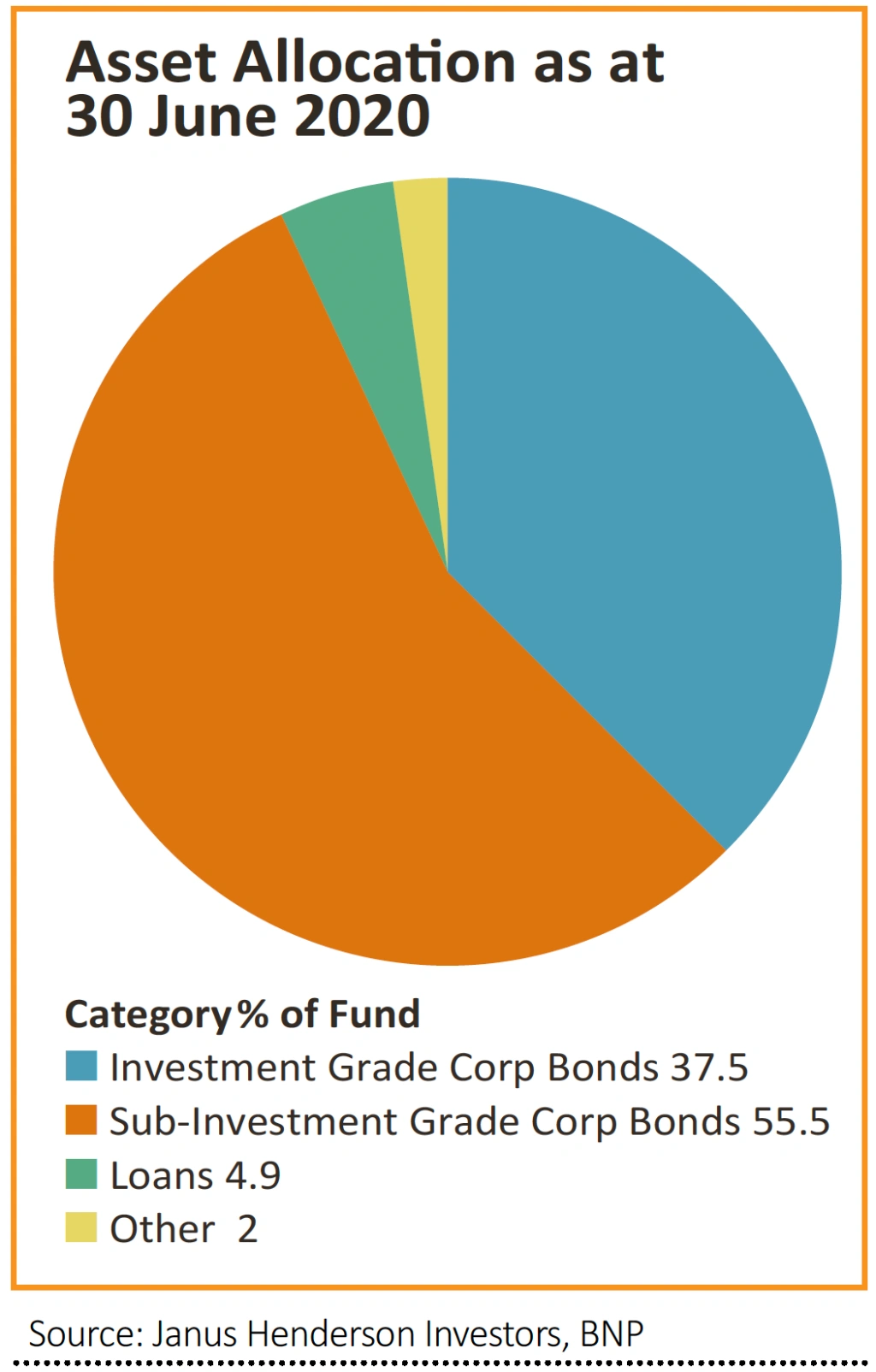

Just over half of the trust’s assets are invested in sub-investment grade corporate bonds with around 38% in investment grade corporate bonds and minimal exposure to loans. The trust is invested in around 170 different positions and the largest 10 have remained relatively stable over time.

THE STRATEGY

Fund managers John Pattullo and Jenna Barnard aim to increase risk and leverage during economic expansions while positioning the fund more defensively during downturns.

In the eye of the Covid-19 storm, risk and leverage was dialled up significantly to take advantage of the unprecedented policy response by the US Federal Reserve and the government’s fiscal backstop measures.

The amount of stimulus unleashed was close to 40% of GDP which historically has only been seen during World Wars. Pattullo and Barnard believe that adopting a war-like approach to the pandemic by the authorities was completely justified under the circumstances. The income gearing of the trust was increased to 35%, from the usual 20% to 25% range. That meant borrowing more money to invest in the markets with the aim of enhancing returns.

The fund purchased a synthetic credit default index called the Itraxx Crossover which is composed of 75 of the most liquid sub-investment grade securities in Europe. Effectively the team purchased extra income as the yield spread between non-investment grade and investment grade widened.

BOND CATEGORIES

Investment grade bonds are issued by companies which the rating agencies such as Moody’s class as relatively safe from default. In other words, lenders are highly likely to receive all the coupons or interest payments in full and crucially get their capital back.

Sub-investment grade bonds on the other hand have a much higher probability of issuers defaulting and need to offer prospective investors higher yields to attract investment. The spread between investment and sub-investment is considered a good proxy for the risk appetite of bond investors.

Pattullo estimates the effect of the portfolio changes made in March has secured Henderson Diversified Income Trust’s dividend target for the next two years.

The ensuing snap back in the yield spread was one of the fastest ever seen, fuelled by the Federal Reserve purchasing sub-investment grade bonds for the first time ever which in Pattullo’s opinion ‘backstopped risk’ thereby increasing risk appetite.

INVESTMENT STYLE

Pattullo believes the trust’s differentiated investment approach helped it steer clear of some of the most impacted sectors such as travel and leisure, shipbuilding and energy. While many equity managers claim they have a differentiated investment approach, it is less common in the bond investing world.

Henderson Diversified Income Trust prefers to lend to good quality businesses that don’t need capital rather than to companies in struggling industries with poor fundamentals. The yields on offer may be higher in such industries but the associated risks are considered too great.

To illustrate, Pattullo references bond hedge fund manager Dan Rasmussen who coined the phrase ‘fool’s yield’. This is the yield above which the losses from default overcome the higher coupon payments and investors end up earning lower total returns than they would have by sticking to lower yielding but higher rated bonds.

The team believe almost half of the high yield universe and a third of the investment grade universe is simply uninvestable to their way of thinking. In this regard their approach is similar to quality growth managers in the equity space.

The trust prefers to lend to large non-cyclical businesses which achieve high returns on capital and have at least $300 million of debt outstanding, ensuring liquidity in the bonds.

Strong free cash flow generation and disciplined management are other important considerations. In short the focus is on providing safe, boring income while also providing sufficient diversification to the riskier parts of investors’ portfolios.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.