Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineShining a light on Europe

There are some great stocks across the Atlantic but you pay an increasingly high price for them. In this article we will explain why investors on the hunt for growth could look closer to home, casting their gaze across the Channel to Europe.

LITTLE MARGIN FOR ERROR

UK retail investors seeking ‘quality growth’ stocks outside these shores have been avid buyers of US stocks for several years, and even the unexpected rise in volatility which accompanied the collapse in share prices in February and March doesn’t seem to have dampened their enthusiasm.

As well as direct holdings in stocks such as Amazon.com, Apple, Microsoft and Tesla, UK investors have continued to pour money into US-oriented funds and global funds with large a US exposure such as Fundsmith Equity (B41YBW7) and Scottish Mortgage Investment Trust (SMT) during the first half of this year.

However, with the Nasdaq Composite technology index trading at record highs, and the S&P 500 Composite index a hair’s breadth from its all-time highs after its longest winning streak this year, markets look fully valued to put it mildly.

Add in weak consumer confidence due to the administration’s handling of the coronavirus pandemic, a steep drop in company earnings, and uncertainty over the outcome of the US elections in just a few months’ time – where a Biden victory could signal a rise in corporate taxation – and the risks associated with US stocks have unquestionably risen.

While companies like Apple and Amazon are high quality and have great long-term growth prospects, their valuations are stretched to the point where there is little room for error.

Valuations have been driven up by an excess of cheap money as the government tries to reflate the economy and a lack of returns in the bond market, where rather than ‘risk-free return’ many bonds trade at negative yields and could more accurately be described as offering ‘return-free risk’.

GROWTH STOCKS

‘There is a perception that the US stands for quality growth stocks while Europe stands for cheap cyclicals’ says Sam Cosh, manager of the BMO European Assets Trust (EAT). ‘While that may be true in terms of the index make-up due to the heavy weighting of energy and financial stocks, once you delve deeper there is a wealth of growth companies.’

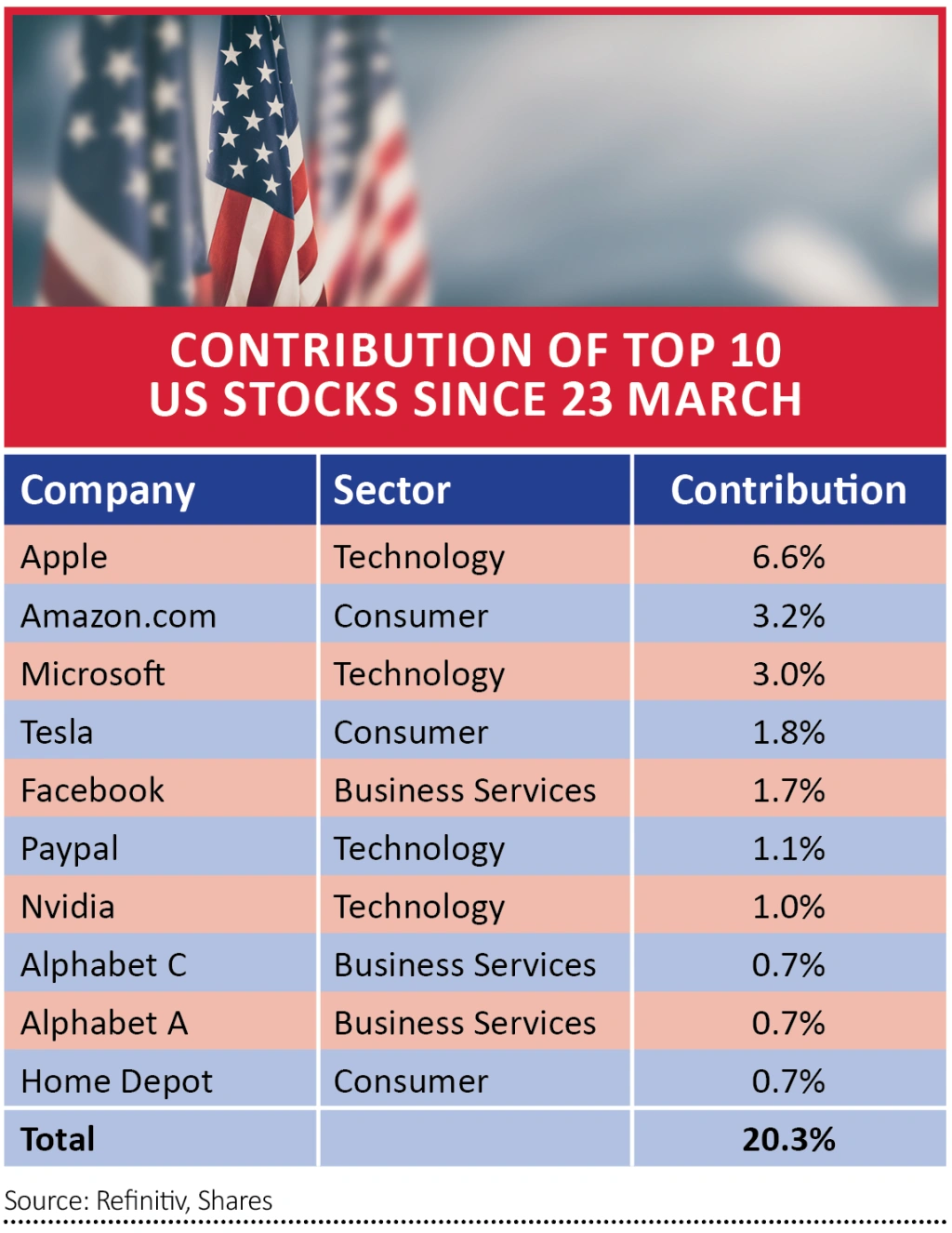

At the same time Europe doesn’t suffer from the ‘concentration risk’ which continues to characterise the US market. Just 10 stocks were responsible for more than 20% of the 50% rebound from the March lows in the US, and Apple now has the highest individual weighting in the S&P 500 of any stock in history.

While it doesn’t have the same weighting as in the US, Europe does have a well-developed technology sector with world-class hardware companies such as semiconductor equipment maker ASML, chipmakers Infineon and STMicroelectronics, and software and IT services firms such as SAP – profiled elsewhere in this week’s magazine – Capgemini and Dassault Systemes.

It’s also home to world-class health care companies such as Bayer, Novartis, Novo Nordisk, Roche and Sanofi, and for those who want ESG exposure there are dozens of high-quality stocks to choose from, many based in Scandinavia, for example wind power operator Orsted, recycling equipment maker Tomra and wind turbine maker Vestas, where environmental issues are very much ‘front of mind’ for consumers and investors.

ATTRACTIVE VALUATIONS

Moreover, growth often comes at a reasonable price in Europe as individual markets tend to be less ‘efficient’ than the homogenised US market and can throw up more bargains.

As AJ Bell’s investment director Russ Mould pointed out a couple of months ago, in sterling terms European stock markets have not just lagged the US market but also Japan and most emerging markets since the euro was introduced in 1999.

‘This poor performance may reflect the lingering effects of the debt crisis that first boiled over a decade ago, as well as the difficulties of providing a solid financial platform with which to support political union, in the absence of fiscal and banking union to support a single currency and unified monetary policy’ says Mould.

ROAD TO RECOVERY

Investors in Germany, Europe’s biggest economy, are upbeat on the outlook for the next 12 months. The latest ZEW economic sentiment survey showed a sharp increase with the ‘future expectations’ reading coming in well above consensus forecasts.

After the Germany economy shrank by 10.1% in the second quarter, the steepest decline on record – although still only half the fall registered by the UK – the latest reading suggests investors see a relatively quick recovery.

‘Hopes for a speedy economic recovery have continued to grow,’ commented ZEW president Professor Achim Wambach. ‘According to the assessments of the individual sectors, experts expect to see a general recovery, especially in the domestic sectors.’ However, investors remain cautious on the outlook for the banking and insurance sectors due to their poor earnings expectations.

Expectations have been helped by the government’s latest €130 billion stimulus package to relaunch the economy. Help includes a reduction in value added tax, support for families and financial aid for local authorities. Germany has already launched €1 trillion of financial support for small and large businesses.

The latest package has a’ green’ angle too, with increased financial incentives for electric and hybrid vehicles and greater investment in environmental businesses such as renewable energy storage.

GROUNDBREAKING DEAL

Germany isn’t alone in using government money to try to rescue its economy. Last month, after days of intense haggling, the European Union inked a landmark €750 billion stimulus package – officially known as the Recovery Fund – which includes unprecedented steps to help its less wealthy members such as issuing debt collectively rather than individually and making over half of the money available as grants which don’t have to be repaid rather than loans.

Admittedly the amount of money involved is minor compared with what national governments themselves are doing, but the deal sent a strong and much-needed message of solidarity given the differing needs and aims of the 27 member states and serious concerns on the part of the so-called ‘Frugal Four’ wealthier nations – Austria, Denmark, Germany and the Netherlands – as well as more moderate members such as Finland over being held liable for the debts of some of the weaker countries.

German chancellor Angela Merkel, who led the discussions with president Macron of France, said ‘Exceptional situations require exceptional measures. Europe has shown it is able to break new ground in a special situation. A very special construct of 27 countries of different backgrounds is actually able to act together, and it has proven it.’

Countries such as France, Italy and Spain – the EU’s second, third and fourth largest economies respectively – could see their economies contract by up to 10% this year, while smaller countries such as Greece – which has barely recovered from its debt crisis during the global financial meltdown of the mid-2000s – simply don’t have the financial resources to fight the Covid-induced slump making them dependent on EU aid.

The fact that the EU was able to pull off a deal, some rancour aside, has given the single currency a major boost against the dollar and sterling which is a crucial first step in attracting investors from outside the euro-zone. During July alone the euro gained more than 4% against the dollar.

Moreover, as BlackRock Greater Europe Trust (BRGE) co-manager Stefan Gries points out, the Recovery Fund ‘can potentially bring greater fiscal coordination, bring in yield spreads for southern economies and bring down the overall risk premium for European equities’.

GREEN PROMISE

With the US locked in its ‘cold war’ trade confrontation with China, European policymakers can see an opportunity to seize the initiative in innovation and technology to deal with climate change and other environmental issues.

The EU has committed €550 billion to climate protection and clean energy technologies over the next seven years, in order to build leading-edge solutions and reduce the zone’s reliance on overseas suppliers.

The timing is also opportune as European consumers have developed a greater awareness of their behaviour during lockdown and have already begun to act more responsibly and sustainably.

According to consultants McKinsey, in a survey of British and German consumers during April more than half said they had ‘significantly’ changed their lifestyles to benefit the environment with more than 60% making an effort to recycle more and actively seek out products with eco-friendly packaging.

Like other habits picked up during lockdown – online shopping being the most obvious example – this behaviour is likely to stick.

EUROPEAN STOCKS TO BUY

Below we present three large-cap ideas, two of which fit the quality growth profile so beloved of investors and one which is more speculative but we believe is undergoing a transformation that could lead to a significant re-rating.

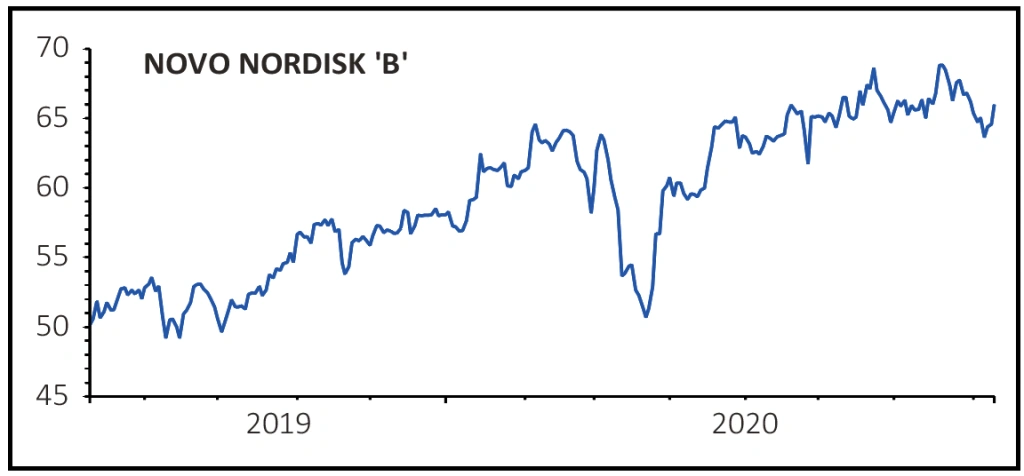

NOVO NORDISK DKK 417.7

Market cap: DKK 995 billion

2020 Sales forecast: DKK 127 billion

Performance year to date: +10.5%

Novo Nordisk is the world leader in diabetes treatments with a market share of almost 30%, meaning it is well placed to meet the needs of an ageing population as well as the alarming spread of the disease not just in developed markets but also in countries like China.

Unlike rival pharma giants such as AstraZeneca (AZN) and French firm Sanofi, its big European rival in diabetes treatments, Novo uses its high returns to fund its own research and development rather than spending big money buying other firms.

Also, unlike most big pharma firms, Novo has focussed on its core businesses of diabetes since it was founded in 1923, continually honing and improving its treatments.

Despite fears of regulators imposing price cuts, especially in the US, the world’s biggest market for its drugs, Novo has been able to increase prices fairly steadily over the past few years. Also, it has used its research to develop anti-obesity drugs since diabetes is more prevalent in people who are overweight.

For Jamie Ross, manager of Henderson EuroTrust (HNE), Novo is a top five holding due to its potential to be a market leader in the area of weight-loss as well as its current role as number one in diabetes. ‘Anti-obesity drug sales are growing at 25-30% annually in the US as healthcare insurers realise that treating obesity reduces the odds of patients developing related diseases, so treating people for weight loss makes economic sense,’ Ross says. ‘We think Novo’s treatment could become a blockbuster in its own right.’

Novo is also a top 10 position in the Fundsmith Equity Fund (B41YBW7), which owns 0.98% of the company. Considering Fundsmith’s stringent approach – to only buy high quality businesses that can sustain high returns on operating capital employed, that can reinvest their cash flows at high rates of return with a high degree of certainty, that are resilient to change and that have advantages that are hard to copy – and the limited number of stocks its holds, this is another endorsement.

NESTLE CHF 109.24

Market cap: CHF 304 billion

2020 Sales forecast: CHF 85 billion

Performance year to date: +4%

Nestle hardly needs an introduction as it is one of world’s best-known consumer companies, but it’s probably still worth running through its main product categories.

Its biggest business is beverages, where it owns the Nescafe and Nespresso brands and which makes up 25% of sales. Then comes nutrition, which makes up 16% of sales, petcare (the Purina and Felix brands) which is 15% of sales, dairy products and ice cream at 14% of sales, prepared dishes (Buitoni pasta and Maggi noodles) at 13%, confectionary at 9% and lastly bottled water at 8% of sales.

The appointment of chief executive Ulf Mark Schneider in 2017, and a new focus on growth and margins, marked a major change for the firm and for investors. Schneider cut back investment on non-core ranges or sold them altogether and concentrated the firm’s efforts on its key brands to keep them competitive and attractive to consumers.

He also spearheaded a push towards ‘fast innovation’, developing and rolling out new products – premium coffees and plant-based food and drink ranges for example – at a much quicker pace than in the past and ahead of its rivals.

Coming into 2020 top line growth was strong with accelerating organic growth driven by the US and by PetCare sales. Cash flow was strong while underlying earnings and returns to shareholders hit record levels.

Growth inevitably slowed in the first half, but sales were ahead of forecasts thanks to robust demand in developed markets, and management – who are highly respected by investors – are forecasting organic sales of 2% to 3% for the full year.

Sam Morse, manager of the Fidelity European Values (FEV) investment trust, believes Nestle has ‘good growth prospects given a significant proportion of its business is in categories with both strong growth and high emotional engagement and where there is scope for premiumisation and pricing power arising from sales into more fragmented channels’.

Morse adds: ‘There are also material opportunities to improve operational efficiencies, and organizational changes should drive faster and more relevant innovation, which should allow Nestle to see the benefits of its portfolio’s strong strategic positioning.’

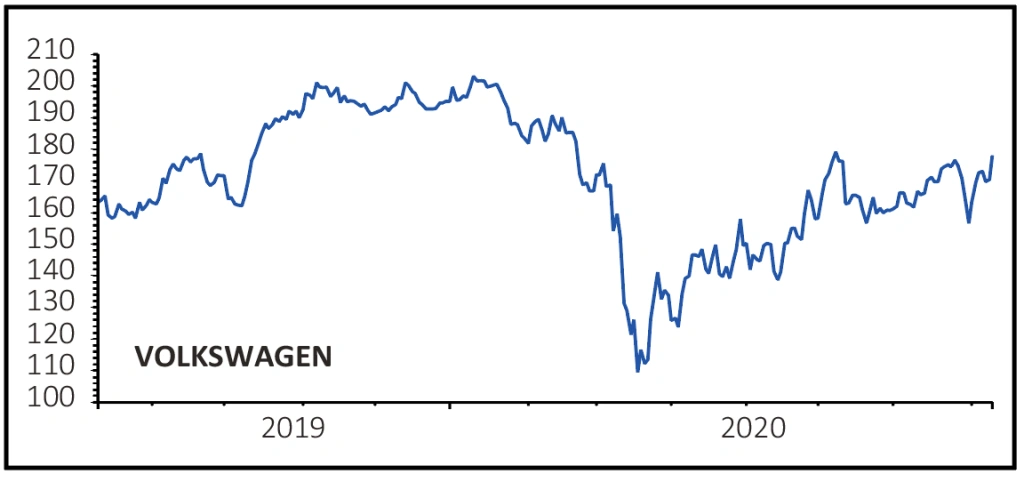

VOLKSWAGEN 139.06

Market cap: €74 billion

2020 Sales forecast: €215 billion

Performance year to date: -20%

Like Nestle, Volkswagen barely needs an introduction, but unlike the premium consumer products firm it is a value/recovery story rather than a growth story.

After its well-documented role in ‘dieselgate’ exhaust emissions scandal – which the firm has provisioned extensively for – VW has gone back to the drawing board and aims to generate close to half of its sales from electric vehicles within 10 years.

On top of the billions it has already spent developing the e-Golf, e-Up and the yet-to-be-released ID.3 full electric car, it is spending €60bn over the next four years on 75 new models using electric and hybrid technologies as well as spending on ‘digitising’ vehicles, betting on its scale as the world’s second-largest car-maker as well as its reputation for quality and reliability.

Mikhail Zverev, head of global equities at Aviva Investors and manager of the Global Equity Unconstrained Fund, believes that Covid has up-ended the consensus view that individually-owned vehicles were a thing of the past.

‘More people will work from home and further afield, and they need a car, while some are thinking about starting families which typically means buying a new car. The affordability of electric vehicles has changed the game and will accelerate the ‘park refresh’ rate.’

Zverev also points to the valuation disparity between VW and Tesla. VW has spent as much on technology as Tesla, yet it trades on 6.6 times next year’s earnings compared with 128 times for Tesla. ‘There’s a Tesla inside VW which isn’t reflected in the price’, he concludes.

VW is also a play on the rising Chinese middle class as it manufactures vehicles in the country both under its own brand and through joint ventures.

FUNDS TO PLAY EUROPE

For investors looking to tap into high-quality European growth companies but who don’t have time to do their own research and want someone else to pick the stocks for them, there is no shortage of UK funds and trusts investing in Europe.

For large-cap quality growth, we like Henderson EuroTrust (HNE), managed by Jamie Ross. The fund focuses on sustainable growth ‘compounders’ which can reinvest their substantial cash flows back into the business and keep growing.

While Nestle and Novo Nordisk are both top ten holdings, Ross also has investments in platform businesses such as Scout 24 – a German equivalent to Rightmove (RMV) – and Delivery Hero, a global rival to Just Eat Takeaway (JET).

Unusually the trust is trading at an 11% discount to net asset value as its holdings have outperformed the benchmark but the share price has yet to catch up.

We also like the five-star rated Comgest Growth Europe (B28PG35), a focused large-cap fund with €3.9bn of assets as of the end of July invested in just 38 stocks.

Like Ross, manager Arnaud Cosserat – who is also chief executive and chief investment officer of Comgest – is a holder of Novo Nordisk, while his other top five holdings include ASML and SAP.

The fund has a heavy weighting in healthcare and technology, which has served it well during the pandemic, and it scores well in terms of its carbon and environmental footprint – details of which are included in its monthly factsheet – making it a sound choice for ESG investors.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.