Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineJoining the kids savings boom

Parents and grandparents have put away more money for their children during the current coronavirus pandemic, as they’ve saved money on their usual outgoings and funnelled that into Junior ISAs.

Lots of people have found they’ve saved money during lockdown, whether that’s not paying for commuting costs, the cost of childcare disappearing, not going on the family holiday or just going out less. While it would be tempting to save this money to splurge once the pandemic is fully over, lots of savvy parents have put the money away for their children’s future.

There’s been a big increase in the number of people putting money into their children’s ISAs during the past three months. From April to June the AJ Bell Youinvest platform has seen a 113% increase in the number of people paying into a Junior ISA when compared to the same period last year, showing that many have used lockdown to organise their finances and put their savings to good use.

There has also been a rise in the total amount people are contributing, up 127% over the three months to the end of June when compared to the same period last year. Average subscriptions per JISA have risen by 26%, from £1,853 to £2,326. However, there was a dramatic increase in the Junior ISA allowance in April, from £4,368 up to £9,000, which some parents may be making full use of and could skew the figures.

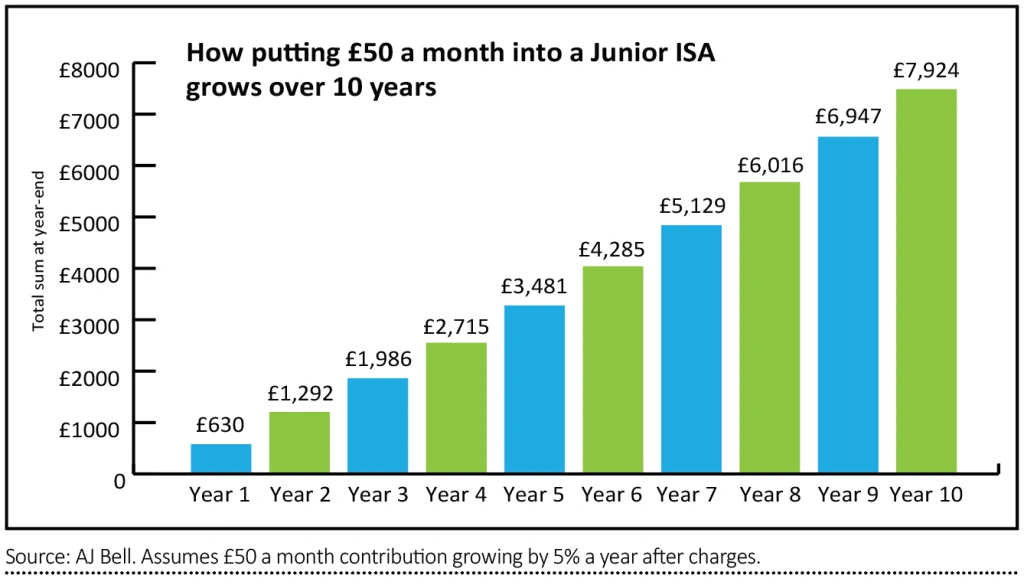

Even putting away an extra £50 a month can really boost your child’s savings pot, as with 5% investment growth a year after charges this would add up to almost £8,000 over 10 years. If you could afford to bump this additional contribution to £100 a month then you’d give your kid an extra £15,850 in their pot after a decade, assuming the same 5% return a year.

Junior ISAs – the basics

You can open a Junior ISA for a child if they’re under 18 and you’re their parent (or in a position of parental responsibility). Only parents or guardians can open a Junior ISA, but anyone can pay into them, such as grandparents or friends.

A Junior ISA shelters your child’s investments from capital gains and income tax. You can put in up to £9,000 a year, either in a lump sum or in regular payments, but the money is locked away until your child turns 18, at which point they become responsible for the money.

If you’ve already set up a Child Trust Fund for your child you can still open a Junior ISA but you’d need to transfer the Child Trust Fund in straight away.

What can your lockdown savings mean for your child’s future wealth?

Cost of commuting = £10,480

According to Llyods Banking the average cost of commuting per month is £66.13 across the UK. During lockdown lots of people have been working from home and many expect to only go back to the office part-time or not go back at all. So if parents saved the cost of one of them commuting each month and put that money into a Junior ISA they would have £10,480 after 10 years, assuming a 5% return each year. Even after five years they’ve have built up almost £4,600 extra.

Cost of childcare = £7,063

It costs £1,084 on average for a child under the age of two to have full-time childcare at a nursery in England, according to the Coram Childcare Survey. Lots of people saw their nursery close during lockdown and stay shut for four months, and while this presented many with a childcare nightmare it definitely saved families lots of money. Obviously nurseries are re-opening and this likely isn’t a lockdown cost you can save forever, but funnelling just those four months of the average childcare cost into your child’s Junior ISA as a lump sum would boost their pot by £7,063 after 10 years, assuming 5% growth a year.

Eating out = £13,735

As restaurants shut in lockdown people couldn’t go out to eat and still many families are reluctant to go out for a meal. Even after the current pandemic is fully over many people may decide to eat out less in order to carry on saving money. If you previously went out for one meal a week costing £40 each time but you now cut that down to one a fortnight, that’s a saving of £1,040 a year. If that’s funnelled into a JISA instead it would amount to £13,735 after a decade, based on 5% return a year after fees.

Cost of a holiday = £4,365

Lockdown has meant that many families have cancelled holidays. While some might be re-booking a UK break or venturing abroad later this summer, many will have cancelled for this year and saved the cash instead. The average spend per person for a holiday abroad is £670, according to figures from the Office for National Statistics. This means that for a family of four it would cost £2,680 per holiday. That same lump sum of money funnelled into a JISA as a one-off would equal £4,365 after 10 years, assuming 5% growth a year.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.