Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineSAP is one of the most important stocks in Europe

Germany’s SAP might be the most important company you have never heard of. It is a genuine enterprise technology sector giant, relentlessly generating billions in revenue and profit year after year.

Listed in Frankfurt and Stuttgart and worth €168 billion, it is Germany’s largest listed company, bigger than household names like Adidas, BMW and Volkswagen combined, and the biggest tech firm in Europe, more than 20 times the size of Sage (SGE), the UK’s largest tech company.

CRUCIAL TOOLS FOR BUSINESS

For decades SAP has provided critical applications for businesses of all shapes and sizes, although about 80% are small and medium-sized (SME) operations.

It specialises in key enterprise resource planning (ERP) tools without which businesses simply could not run, such as supply chain management, human resources, customer experience management and analysis, spend intelligence, machine learning-based analytics, and more. There’s also a €4 billion venture capital arm called Sapphire Ventures.

SAP IS A ‘HIDDEN GEM’

Simon McGarry, senior equity analyst at Canaccord Genuity Wealth Management, points out how the technology sector has rewarded investors this year, albeit many of the big US names are now looking expensive.

He suggests looking at European tech stocks where share price performance has generally been more sedate than peers in the US, implying an opportunity to pick up good names in the sector at a discount to highly valued names in North America.

‘These stocks have been mistreated by the market and have fallen victim to the location of their listing as opposed to where they do business,’ he adds.

McGarry says tech stocks in Europe are benefiting from the same structural growth trends as the US and highlights SAP as one of the hidden gems on the market. It appears on a filter of European tech names with strong cash flows and returns, solid balance sheets and businesses able to prioritise the long term by investing in R&D.

At the end of 2019, SAP had more than 101,000 staff helping in excess of 440,000 customers across 180 countries, with more than 200 million cloud platform users. This includes 92% of Forbes Global 2000 companies and 98% of the 100 most valued brands, companies crucial to our daily lives.

According to SAP, its clients distribute 78% of the world’s food and 82% of the world’s medical devices, while 77% of the world’s transaction revenue touches an SAP system at some point.

The sheer scale and breadth of SAP is one of the reasons why the stock appears in all types of funds; Europe-focused, global growth, technology specialists and more.

GATHERING CLOUD

The key to understanding the investment case is to grasp SAP’s own cloud adoption story. Since launching its HANA (High-Performance Analytic Appliance) platform nearly a decade ago, cloud has been its primary focus, designing HANA tools that are industry-specific yet highly customisable.

This ensures value for users through better decision making, improved operating efficiency and cost flexibility needed in an increasingly digital world.

It has had significant success, as its huge growth in subscribers and revenue shows. Yet more than twice 2019’s €7 billion cloud income still comes from traditional licence sales and high margin support, with 86.6% gross margins in 2019.

This represents a challenge for any software business not born in the cloud because switching customers over typically depresses short-term revenue and profit as the support income dries up.

The pay-off down the line should be more sticky subscription revenues from a cheaper, more flexible platform for users, plus lower cost of distributing updates, among other things. Finding the right balance is important.

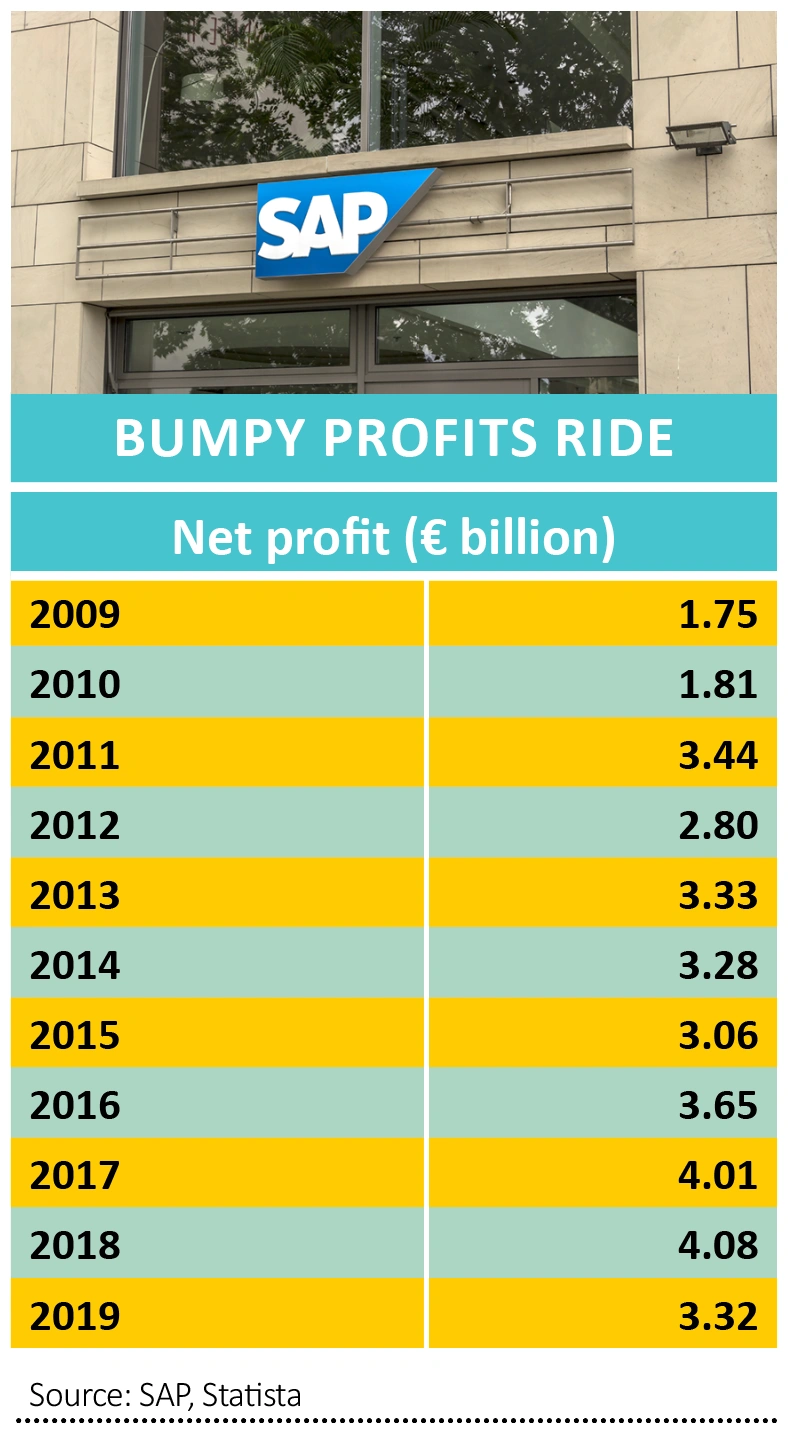

In the last three years, for example, SAP’s revenues increased at an average growth rate of 8%, yet its adjusted operating margin declined from 27% to 23%, according to data from FinLABO Research. This helps explain the volatile nature of its net profit performance which has moved up and down over the past decade rather than show sustained progression year after year.

GROWTH AND QUALITY

That said, the stock scores highly on several quality metrics. For example, return on equity stands at around 20%, more than twice its estimated 8% cost of capital. Return on capital employed is estimated at approximately 18% next year.

SAP has built its business on a sound financial structure. Net debt is estimated at €9.9 billion this year, putting its debt-to-equity ratio at a very comfortable 0.3, and debt-to-EBITDA of 1.03. Earnings per share are forecast to outstrip the mid-single digits growth of revenue over the next couple of years at an average 13% or so.

In the past five years the shares have more than doubled to €135.13, putting the stock on a rolling 12-month price-to-earnings ratio of 25.1, based on Refinitiv data, an 11% premium to the software sector.

We wouldn’t be surprised to see that premium widen over the coming years as SAP leverages its scale advantages to maximise its cloud opportunity, accelerating profits potentially beyond current expectations.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.