Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineDon’t get sucked into the hydrogen hype

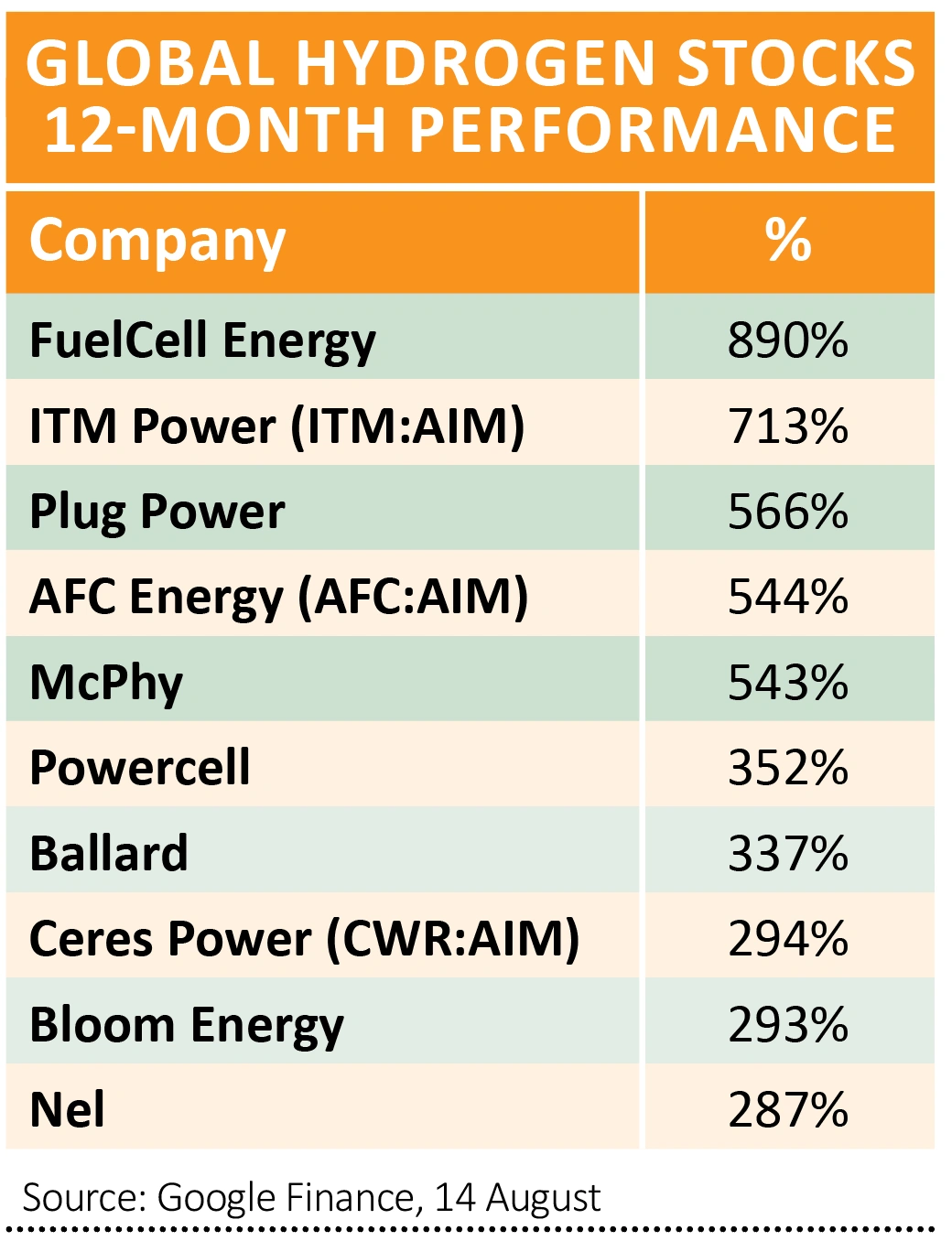

If you were a shareholder in a hydrogen fuel cell company a year ago, right now you could be sitting on a small fortune.

For UK investors, there are three stocks directly involved in the space. Two of them, AFC Energy (AFC:AIM) and Ceres Power (CWR:AIM), make fuel cells, and the other, ITM Power (ITM:AIM), makes electrolysers, a low carbon way to produce hydrogen.

The share prices of all three have soared in the past year. ITM has been increased 10-fold, AFC Energy is up five times and Ceres Power has almost tripled. In our view these businesses are now priced for perfection and we think the risks are too high to invest at these levels.

For more diversified exposure to the hydrogen opportunity through a mature business investors could buy Johnson Matthey (JMAT) which trades on an enticing March 2022 price to earnings ratio of 11.8 times.

ELECTRIFYING ENERGY

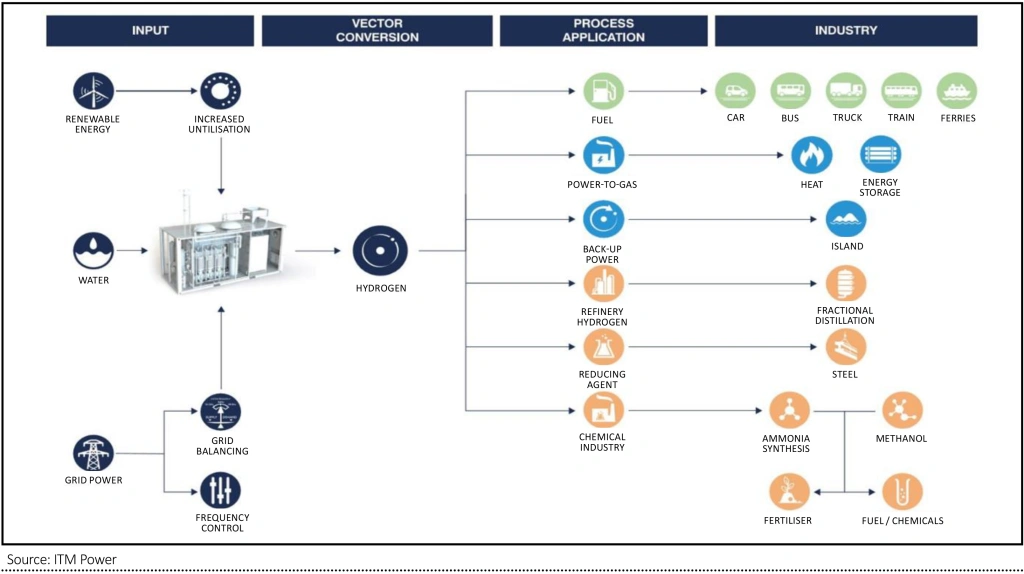

There’s a general consensus that electrification of energy is pretty much central to any solution to combating climate change and protecting the environment, and now more than ever hydrogen is increasingly being recognised as a key part of that process.

Hydrogen is increasingly being seen as central to getting us to a net zero carbon world by 2050. The gas has a wide range of uses, and can be used to store energy, heat homes, decarbonise the heavier, dirtier industries like cement, steel, glass and petrochemicals, and has the ability to generate electricity.

There’s also a realisation that clean hydrogen can play a vital role in balancing the future energy system because it can be created from renewable energy such as wind and solar during periods of oversupply via water electrolysers, but can create energy through fuel cells when that intermittent energy generation is low.

None of all this would matter if the technology to make it happen wasn’t ready, but it is now with companies starting to reach commercialisation of things like fuel cells and electrolysers – two key enablers for using clean hydrogen – while the rapidly rising adoption of renewable energy is also helping companies integrate hydrogen to the way they do things to help them decarbonise their activities.

SITTING UP AND TAKING NOTICE

And there are two main reasons in particularly why people are starting paying attention now. Firstly, major companies like BP (BP.) and Royal Dutch Shell (RDSB) are looking at ways to add clean hydrogen to their business models to help the transition to greener energy.

Secondly, investors are getting excited about clean hydrogen because policymakers are too, particularly when it comes to planning for a net zero carbon future.

What has everyone taking notice is commitments from governments which suggest the hydrogen and fuel cell sector could be a big winner in national industrial recovery programmes currently being planned.

For example, Germany’s finance minister recently indicated €9 billion of the €150 billion recovery package announced a few months ago will be designated for clean hydrogen projects, in particular electrolyser projects.

Reports also indicate the European Commission is working on a big green energy support programme. Full details of the EU Green Deal have yet to be announced but are said to include a proposed €40 billion energy transition fund where hydrogen is set to be heavily featured. EU Commissioner for Energy, Kadri Simson, called hydrogen a potential ‘game changer’.

CHINESE GROWTH OPPORTUNITY

In further good news for the industry, China seemingly wants to show the world how progressive and innovative it is after unveiling its hydrogen strategy in July 2020, in which it wants to compete with the West for clean hydrogen ‘superpower’ status.

The country plans to have 5,000 vehicles powered by fuel cells – which convert hydrogen into electricity to power cars, buses, heating, etc – on the road by the end of the year, and a million by 2030.

According to analysts at Berenberg, industry sources estimate that the fuel cell market will record a 24% compound annual growth rate between 2016 and 2024, with fuel cells an increasingly relevant solution to the intermittency and capacity issues the electricity grid will face in the coming years with electrification and the rise of renewables.

The rocketing valuations of ITM, AFC and Ceres however have raised eyebrows, especially given none of these companies are making a great deal of money right now, with all of them still in the early stages of development.

ITM Power for example only recorded £3 million of sales in the year to 30 April, yet it has a market value of £1.3 billion, trading on a price-to-book valuation of 16.8 times, according to Stockopedia. Most companies have a P/B ratio of between one and three.

AFC Energy hasn’t generated any revenue and trades on a P/B ratio of 29.2 times. Ceres Power on the other hand has annual revenues of £23.5 million and trades on a lower valuation, but isn’t close to turning a profit and still trades at a demanding P/B ratio of 10.4 times according to Stockopedia.

WE’VE BEEN HERE BEFORE

If you look back at the all-time share price chart for the three companies, you’ll see their valuations soared in the middle of the noughties before spiralling down as quickly as they rose, and spending the subsequent decade firmly in small and micro-cap territory.

This begs the question of whether or not this is simply another hype stage. All those involved in the industry insist this time it’s different. Though, as a reminder, these were once described by investment guru Sir John Templeton as the most dangerous words in investing.

‘This is very real’, says Phil Caldwell, chief executive of Ceres Power. ‘When I started in fuel cells 20 years ago, none of the big companies really needed this technology.

‘But now there is the need for electrification, there is the need to meet climate change targets, and these companies need fuel cells to enable that shift.

‘Also, don’t forget the ESG angle is very strong now, you even see it on the agendas of companies like BP (BP.) and (Royal Dutch) Shell (RDSB). Whereas 20 years ago it was about the technology, now it’s essential to hitting climate change targets. There wasn’t that commercial imperative back then, but there is now.’

That commercial imperative is starting to show in the partnerships companies like Ceres are announcing. The firm has cut deals with the likes of Bosch and Chinese giant Weichai Power, who both own significant stakes in Ceres.

While ITM Power is working in a joint venture with industrial gas giant Linde, and counts Shell among its customers, and AFC Energy has announced a partnership with Spanish construction giant Acciona.

This is also part of what has driven investor interest, according to Investec analyst Marc Elliott. He says, ‘We believe companies such as Ceres, ITM Power, Ballard and Plug Power have become more prominent within the investment community at least partly as a result of the deals and alliances they have formed with major multinationals.

‘The inference is that these major companies have ascertained that they need access to this IP. They have extensive R&D capabilities and resources, and consequently their involvement is also seen as key to de-risking the commercial development of the technology.’

WHEN WILL POTENTIAL BECOME REALITY?

But going forward, the question people really want to know is, when will all this potential become reality?

Ceres, which licenses its technology rather than manufactures the fuel cells itself, sees its partners mass manufacturing its products in the next three to four years.

ITM Power is set to move into a factory in Sheffield in November, which will be the world’s largest electrolyser factory when finished, and according to a research note from Investec the company should ramp up to capacity after three years, with annual turnover eventually reaching £500 million.

But according to current forecasts compiled by Refinitiv, not much is expected in the next year or two. ITM’s revenue is slated to reach £15.8 million in it 2021 financial year and £37.9 million in 2022, with its losses narrowing from £16.2 million in 2020 to £5.5 million

in 2022.

Ceres Power’s revenue is forecast to rise 14% in 2021 to £26.8 million and 30% in 2022 to £34.9 million, according to Refinitiv, while AFC energy is forecast to starting generating around £2.5 million in revenue next year.

One of the questions investors have also been asking is whether or not, given their small size compared to the might of the firms they’re partnering with, these companies could become takeover targets and simply be bought by some multinational.

ITM Power’s chief executive Dr Graham Cooley says there will be a ‘wave of consolidation’ in the industry going forwards, but insists ITM Power for example is ‘in this for the long-term’, and that its intention is to be ‘world leaders’ in the industry.

On the surge in interest in the sector, Cooley says with conviction, ‘Listen, I could see what was coming a year ago. The demand that’s coming is incredibly large. ITM Power is in the right place at the right time.’

AN ALTERNATIVE WAY TO PLAY THE HYDROGEN THEME

There are other companies starting to get involved in the space, which unlike the ones above are much larger and/or earnings positive.

They include FTSE 100 industrial giant Johnson Matthey. In our view this is a lower risk way to play the growth in hydrogen.

The company doesn’t appear to derive much revenue from hydrogen technologies at the moment, but it sees hydrogen as a key part of its longer term growth and spending on R&D development for hydrogen fuel cells and low carbon hydrogen projects.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.