Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazine3i: the investment trust helping good companies become great

London-based 3i (III) is the pre-eminent UK listed direct private equity investment trust, with a portfolio valued at £8.1 billion as of the end of March.

Founded at the end of the Second World War by the Bank of England and major UK banks to provide long-term capital to small and medium businesses, the Industrial and Commercial Finance Corporation as it was once known has been listed on the stock exchange since it floated in 1994 and has been a stalwart of the FTSE 100 ever since.

3i’s name is an abbreviation of Investors in Industry, which it adopted in 1983.

UGLY DUCKLING?

Despite an average daily stock market turnover of £18 million, similar to Scottish Mortgage Investment Trust (SMT), 3i has low profile among retail investors.

Whereas Shares readers are keen followers of fund managers such as James Anderson and Nick Train, and could likely cite word for word their views on stocks ranging from Tesla to Unilever (ULVR) if asked to, it’s a fair bet that only a handful would know many of the companies in the 3i portfolio.

This is intriguing given that Scottish Mortgage has made such a virtue of its unquoted holdings, with its exposure having risen from just 4% of net asset value (NAV) five years ago to over 20% today and with shareholders having recently voted to raise the weighting of unlisted stocks to as much as 30% of the portfolio.

TRANSFORMATION

In fairness, a decade ago 3i’s portfolio was an unfocused hodgepodge stretching from Europe and the US as far as India and China and ranging from large risk reinsurance to power generation and oil services.

That broad exposure meant it performed poorly in the global financial crisis, and the firm had to go cap in hand to shareholders for £730 million in 2009 ‘on the clear understanding that it would be matched by self-help’, as the-then chairman Baroness Hogg put it in the 2010 annual report.

With the appointment of Simon Borrows as chief executive in 2012, change finally came. Parachuted in as chief investment officer a year earlier, he had been head of mergers and acquisitions at Barings Brothers, which advised on 3i’s original float, and chairman of investment bank Greenhill & Co.

His strategic overhaul in 2012 went right back to first principles, examining what 3i was good at and focusing on those areas. ‘It was clinical and analytical, and it transformed our resilience,’ says finance director Julia Wilson.

The portfolio, which had almost 200 investments in 2010, now has just 31 unquoted holdings and one quoted stake. Moreover, it is focused on just four sectors – consumer, business and technology services, industrial and healthcare – in three markets, being the UK, Europe and North America.

TURNING GOOD INTO GREAT

3i’s investment strategy is ‘to take good companies and make them great’ according to Wilson. Typical target companies have an enterprise, or combined debt and equity, value of between €100 million and €500 million, and are sustainable businesses.

‘We aren’t interested in distressed companies, special situations or turnaround stories,’ explains Wilson.

An example of something that does fit the bill for 3i would be a company from the German ‘Mittelstand’, with family ownership, revenues of €50 million or more and a few hundred employees. These firms typically have owners who are passionate about taking their business to the next level but lack the capital and/or the necessary experience to get there, which is where 3i can help.

Alternatively, a target company could be a small subsidiary of a bigger firm, where management have a vision which isn’t shared by the owners. In this case 3i can help with a management buyout, but in each case, it takes a seat on the board and has a hand in the management of companies in which it invests.

The investment committee oversees and approves each new investment, and every holding is reviewed at monthly meetings looking at performance as well as being scrutinised more deeply every six months.

Meanwhile 3i’s own global network of advisers and business leaders assess business opportunities and help drive value in its investments.

JEWELS IN THE CROWN

3i’s biggest investment is in Dutch retailer Action which accounts for 44% of the value of the portfolio. Action is Europe’s biggest non-food discount retailer, selling over €5 billion of everyday essential items each year through more than 1,550 stores.

Its average store size is between 800 and 1,000 square metres, roughly the same size as a B&M Bargains store in the UK. Having won European Retailer of the Year three years running, Action is expanding rapidly south and east in Europe from its Benelux base with 3i’s backing.

3i’s next biggest holding, and the only quoted asset, is a 30% stake in 3i Infrastructure (3IN) investment trust, which was valued at £1.1 billion at the end of March. 3i Group covers its operating costs with the management and performance fees generated by the infrastructure business with a top-up of income from some of its other portfolio holdings, minimising the dilution of returns.

HAVING A GOOD CRISIS

Several of the smaller holdings in the portfolio have benefited from the shift to online consumption seen during the pandemic, such as Danish interior design and furniture firm BoConcept and German specialty online lighting retailer Lampenwelt.

Others have been more direct beneficiaries, such as Benelux personal care firm Royal Sanders, which is a leading producer of own-label and white-label hand wash; and Cirtec, a global provider of outsourced medical device and component design, engineering and manufacturing.

Notwithstanding the blanket travel restrictions, investee company and bespoke holiday firm Audley Travel has seen positive momentum in bookings over the last few weeks as many of its clients are wealthy retirees whose income hasn’t been affected by the crisis.

DOUBLE YOUR MONEY

3i’s goal with every company in which it invests is to double its shareholders’ money over five years, meaning it aims to generate mid-to-high teens percentage returns for shareholders across the cycle.

Typically, it would target between four and seven new investments a year, as well as one or two disposals, but Wilson says it is currently more focused on existing investments.

‘Since quantitative easing started the private equity industry has amassed a lot of fire power, so we are extremely selective. Our priority is to support the companies already in our portfolio with their growth plans.’

This includes ‘buy and build’, where 3i can help its investee companies operating in fragmented industries to scale up by buying smaller rivals.

When an investment has grown to the extent that 3i achieves its target return, the typical buyers are larger private equity firms or companies looking to expand.

AN INVESTOR’S VIEW

Sam Morse, manager of Fidelity European Values (FEV), is a long-time supporter of 3i and the stock is one of his very few UK holdings.

He says: ‘Simon Borrows and the 3i team have honed the portfolio into a focused collection of high-quality private equity and infrastructure assets.

‘The group’s balance sheet is strong and 3i has plenty of dry powder to take advantage of upcoming investment opportunities while continuing to pay shareholders an attractive 4%-plus dividend yield.’

SHOULD YOU BUY THE SHARES?

While on paper 3i’s portfolio may be less exciting than Scottish Mortgage, which is more focused on highly rated technology stocks, it does include well-run businesses with steady cash flows and plenty of potential for growth.

As well as providing exposure to unlisted companies, almost all the firm’s revenues are generated outside the UK making it a useful tool for investors seeking diversification.

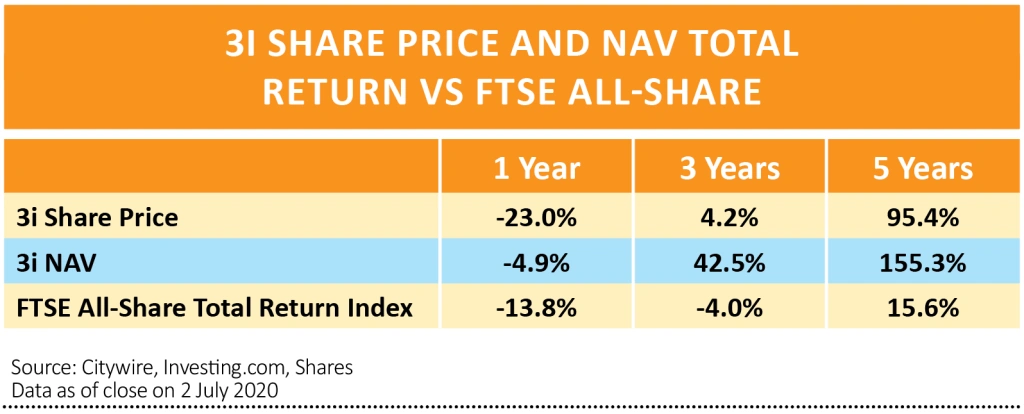

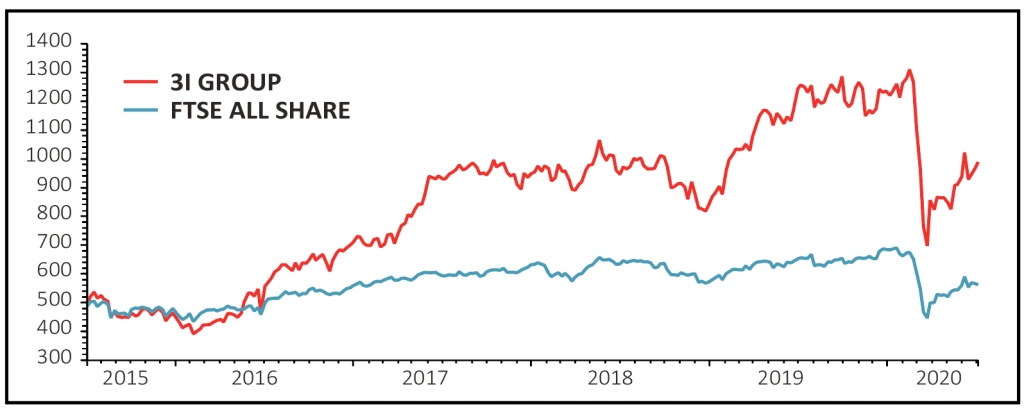

The premium to net asset value has narrowed dramatically from more than 50% in 2017 to 7.8% at the start of July 2020. This narrowing helps to explain why the share price gains have lagged the NAV growth over the past three years.

Anyone investing now should assume that the pace of NAV growth slows because 3i isn’t making many new acquisitions. However, the valuation has become more favourable which makes the stock considerably more attractive. This is a solid ‘buy’ for anyone who is patient and happy to tuck their money away for a long time.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.