Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineGrowing concerns about renewable energy funds

Renewable energy looks to be one of the areas set to receive the greatest amount of investment over the next 10 to 20 years. However, some market commentators have argued it’s a sector not worth backing.

A hard-hitting research note at the start of the year from JP Morgan claimed renewable energy investment trusts could end up becoming a ‘victim of their own success’, as growth in carbon-free energy slashes the cost of electricity and so reduces the amount of money they can generate.

Cracks are already appearing in the sector with falling power prices putting a question mark about the strength of future dividends from renewable energy investment trusts. There have also been declines in long-term cash flow assumptions resulting in falling net asset values (NAVs).

We fear these factors could weigh on share prices and for the stocks to trade on lower premiums to NAV, thereby suffering a double de-rating.

We attempt to address the key points in this article and would suggest anyone invested in this area should reappraise their holdings and read the latest announcements from relevant trusts to understand what’s going on.

The risk/reward dynamics are changing and so the sector’s reputation as a seemingly safe haven may be tested soon.

HIGH DEMAND FOR RENEWABLES TRUSTS

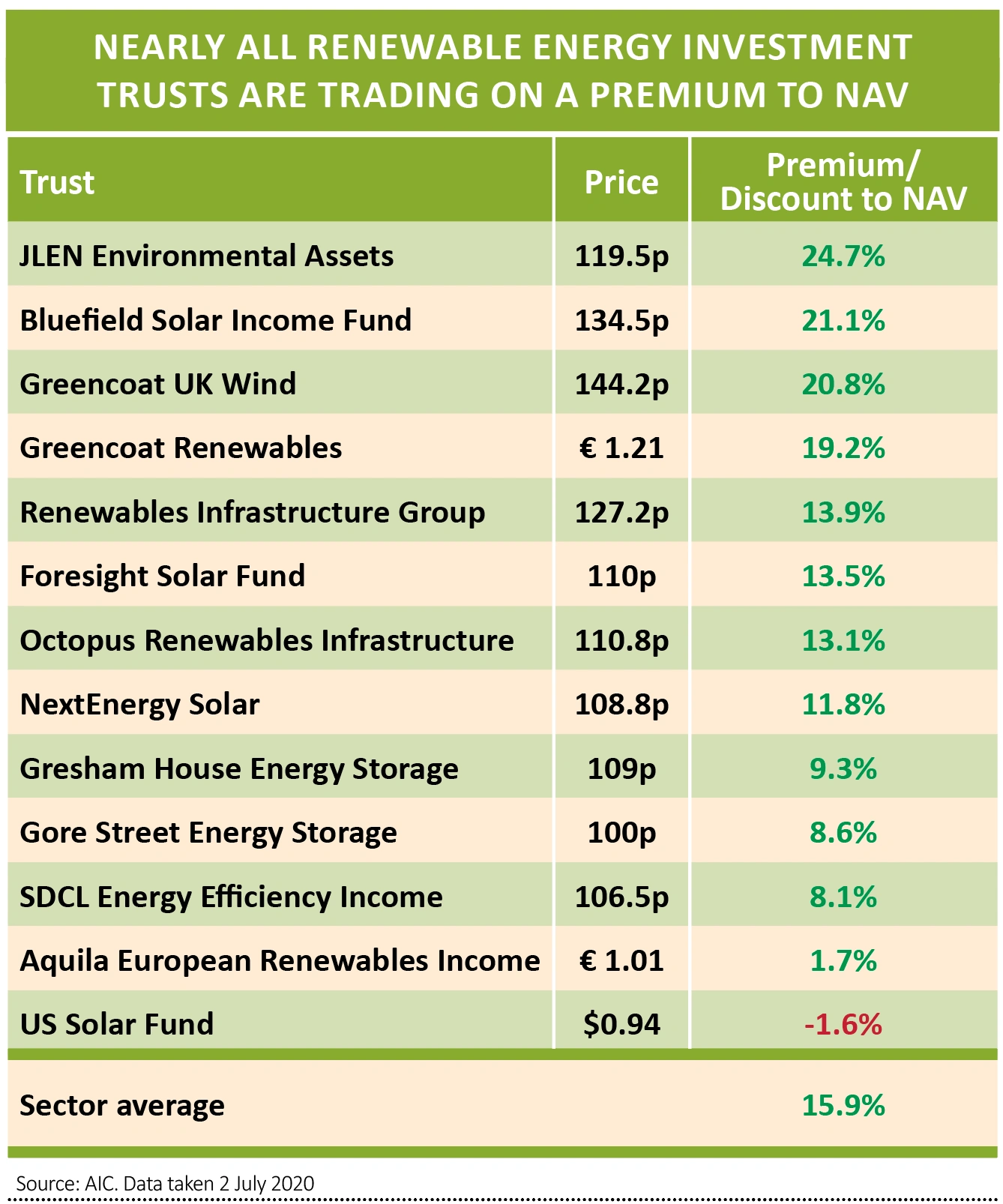

Renewable funds have been in high demand for years due to their reliable dividends, solid yields and environmental friendliness, meaning they often trade at double-digit premiums to their net asset value (NAV).

While all the UK-listed renewable energy trusts have a substantial part of their revenues backed by subsidies and long-term agreements to sell the electricity they generate at a fixed price, they also have a smaller but not insignificant exposure to the wholesale market price for electricity.

The recent hit to electricity demand from the coronavirus pandemic coupled with increased supply has shown the impact lower market prices can have on these funds, with the current power price dropping to around £32 per MWh (megawatt hour) as a result of lockdown and warm weather.

In a presentation accompanying its 2019 results The Renewables Infrastructure Group (TRIG) wrote down its net asset value (NAV) by £101.3m as a result of lower near-term gas prices and an acceleration of new renewable energy projects being built.

Gas prices are used to determine wholesale electricity prices because gas-fired power stations are often what’s called the ‘marginal source of generation’.

When electricity demand is low, it is met by cheap sources of power. This has traditionally included coal-fired and nuclear plants, but when demand increases gas-fired generation (which is more expensive) is added to the mix as the marginal source of generation and therefore sets the wholesale power price.

POWER PRICE ASSUMPTIONS

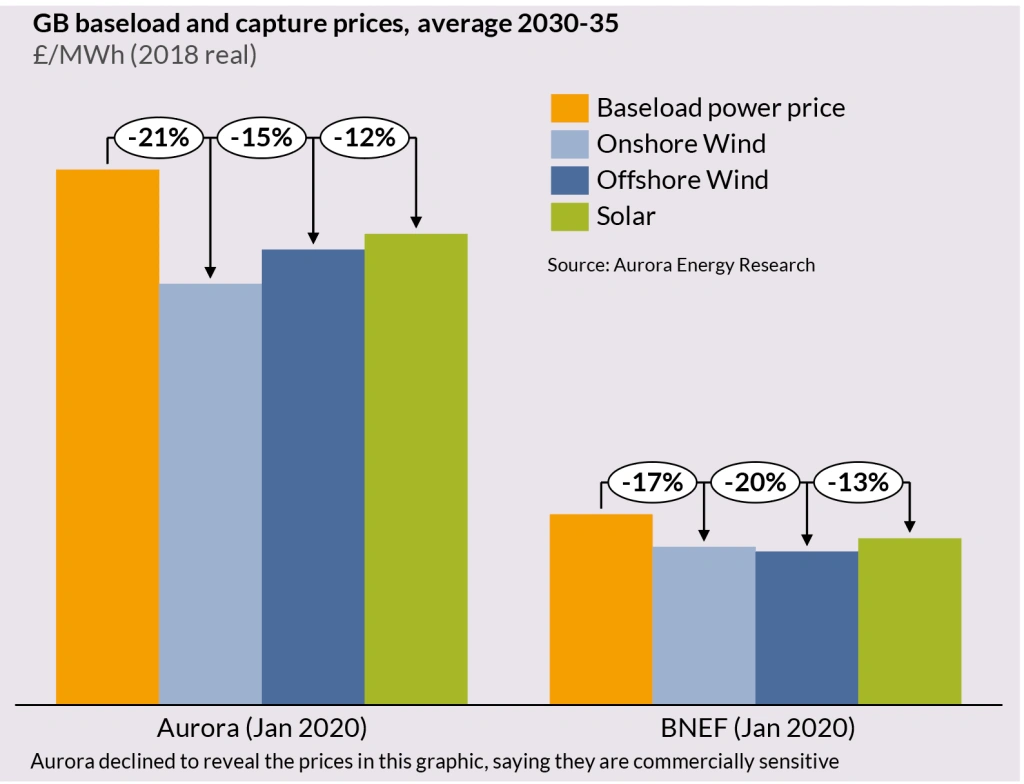

Similar to other renewable trusts, The Renewables Infrastructure Group’s new 2040 power price assumption is about £44 per MWh, down from the £52 per MWh it was forecasting previously.

However, the big concern among some investors is whether or not these price assumptions, which are roughly similar to the average baseload price of £46 per MWh over the past five years, are still too optimistic and that the negative impact on their NAVs could be far more dramatic than the market is currently expecting.

One power price forecast that has caused a lot of discussion is Bloomberg New Energy Finance’s, which estimates baseload power prices will be around £19 per MWh in 2040, far below the figure the renewable funds are currently forecasting.

JP Morgan referenced the Bloomberg forecast in its negative note on the sector at the start of the year, and said that ‘as a result, we take a very cautious view [on the sector] given the risks’.

BLENDED FORECASTS

Trusts tend not to forecast prices themselves and instead use a ‘blended curve’ by taking projections from two or three of the main established forecasters. Bloomberg New Energy Finance is a relatively new entrant to the space and so its forecasts tend not be considered by the investment trusts. Instead they use the likes of Afry, Baringa and Aurora Energy Research.

Stephen Lilley, partner at Greencoat Capital and co-manager of Greencoat UK Wind (UKW), tells Shares ‘we don’t forecast power prices ourselves’.

He says: ‘Given that the future power price is a significant component of the present value of our assets, it wouldn’t be appropriate for us to dictate the numbers that we use in our models and valuations.

‘Instead, we take the central case of a leading independent power price forecaster and this process and provider have remained unchanged since our listing in 2013.

‘We may on occasion make more conservative assumptions than the forecaster, but we never adjust their figures upwards.’

This is echoed by Christine Brockwell of Aquila Capital, investment adviser to Aquila European Renewables Income (AERS), who says forecasting accurate power price curves can be ‘notoriously difficult’.

She explains: ‘While none of us has a crystal ball, we do look to factor in as much information as we can, to try to create as reliable a picture as possible.

‘To this end, the fund builds its forecast of future power pricing by combining forward pricing in the market with independently sourced market power price projections, specific to both the country and technology of the asset we are looking at.’

QUESTIONS BEING ASKED

Key questions Aurora Energy Research has received from its clients include whether prices will ‘crash’ to £25 per MWh by 2030, and whether they could even go below £10 per MWh by 2040.

When looking at past evidence they’re fair questions, given that for example solar prices have fallen far faster than anyone predicted.

A report by clean energy investor Ramez Naam showed the price of solar power now in 2020 is 30 to 40 years ahead of what the International Energy Agency (IEA) predicted in 2014, and even cheaper than what the IEA ever thought it would be back in 2010.

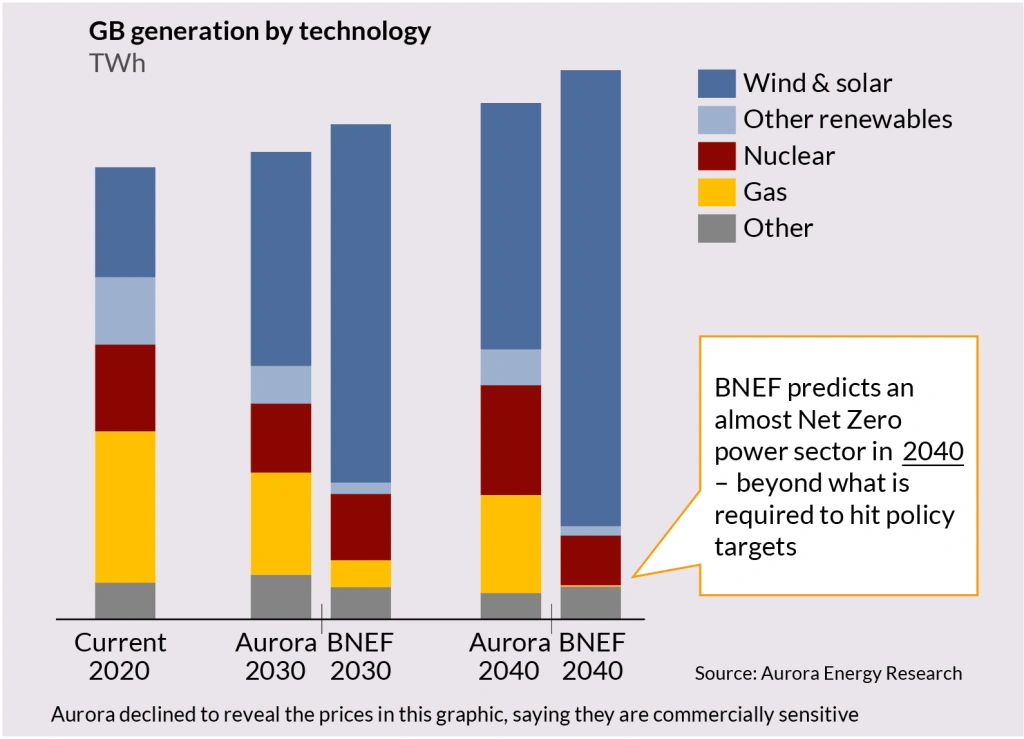

But Aurora sees prices remaining broadly flat in the period to 2030 to 2035, with an increase in supply being offset by a rise in demand due to higher economic growth in the long-term, increased usage of electric vehicles and the electrification of heat.

Martin Anderson, who heads up its GB Renewables team, says power prices are all about supply and demand. He doesn’t subscribe to the view that supply will rise exponentially.

For example, the Bloomberg forecast projects there will be 40GW (gigawatts) of wind capacity added to the grid by 2030, but Anderson points out that this is a ‘very high level’ and not feasible.

He says: ‘Our estimate is much, much lower. You’d need a higher level of build rate than the current level. And remember, one of the key requirements of the deployment of renewables is project economics. At the end of the day they need to make money. There needs to be an equilibrium.’

CANNIBALISATION THREAT

One of the main arguments against renewable funds is the long-term ‘cannibalisation threat’, whereby so many projects get built that supply goes up rapidly, demand doesn’t catch up and these funds ‘cannibalise’ their own revenue base.

But Ricardo Pineiro, who runs FTSE 250 investment trust Foresight Solar (FSFL), says this argument is flawed, and that new projects won’t get built if the right level of return isn’t there.

Pineiro says: ‘The Bloomberg forecast takes a very aggressive view of how much can be deployed and takes the approach that there will be no ceiling, which is incorrect. Capacity will not be added if it’s not economically viable to install.’

Pineiro adds that the main issue is establishing the pace of renewables deployment and believes it will happen over time. He also points out there are many ageing powerplants that will soon need to be taken off the grid and their capacity replaced.

AN OUTSIDE VIEW

What should someone looking to invest in one of these renewable trusts make of it all?

Fund manager James Smith, who runs Premier Global Infrastructure Trust (PGIT), says having a positive or negative view on these trusts ‘depends on what you think is going to happen to power prices in the future’.

He adds in the renewables space in general there are three main types of stocks – ‘some will develop a wind farm for example then sell it to others (such as utility giant SSE (SEE)), some will develop and own an asset, and some – like the UK renewable funds – will not develop assets but will own them.’

Most of the value from an asset is crystallised in the first year after it’s built, Smith adds, and highlights Spanish construction giant Acciona as a type of company that builds and then owns renewable energy assets, and so captures this upside.

He says: ‘The UK renewables sector is low risk but then they don’t necessarily capture as much of the upside. Their rate of return tends to be 7% to 8% rather than the 12% to 13% you’d get from stocks that build and own assets.’

WARNINGS SIGNS

A lot of bad news is coming out of the renewable energy investment trust sector which means it is now less attractive from an investment perspective.

In April, analysts at investment bank Stifel said it thought many funds would be vulnerable to revenue shortfalls and reduced dividend cover when they come to renew price agreements, unless there is a substantial recovery in power prices.

Dividend policies are now changing in parts of the market. Bluefield Solar Income (BSIF), Foresight Solar, JLEN Environmental Assets (JLEN) and The Renewables Infrastructure Group have all dropped their RPI inflation-linked dividend strategy and switched to a progressive policy.

Bluefield has announced plans to radically change its portfolio, moving from only having UK solar projects to now having up to 25% of gross assets in other renewable energy types such as wind and energy storage, together with the ability to invest up to 10% outside of the UK.

NextEnergy Solar (NESF) is also pursuing a similar diversification strategy and its dividend policy is under review, suggesting it too could move away from inflation-linked payouts.

Spreading risks across a broader range of asset types is fine from an investment perspective but this move does highlight the issues in the industry, such as increased competition and lower returns from UK solar assets.

Foresight Solar has seen the amount of fixed price arrangements for its UK assets fall from 53% of the UK portfolio in December 2018 to 32% a year later and they will decrease to just 8% by the end of 2020.

It says: ‘Fixed price arrangements provide greater visibility over future cash flows and limit potential price volatility in the short and medium term.’

There is a real risk of much lower revenue from Foresight’s UK portfolio from 2021 which leads us to reassess our view on the stock. We previously said to buy at 117p in October 2019 and the stock now trades slightly lower at 110p. Amid growing concerns over the sector, we think it is time to sell.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.