Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineEarnings forecasts flag FTSE 100’s mixed profit pedigree

The Financial Conduct Authority’s decision to give companies additional time to prepare their financial statements may elongate the process but the imminent reporting season for UK plc could go a long way to shaping how the headline FTSE indices perform for the rest of this year and beyond.

The good news is that few if any companies have made a rod for their own back by giving any specific guidance for revenue, profit or dividends, owing to the uncertain environment created by the pandemic and their inability to predict how customers and clients will respond even as lockdowns are (generally) eased around the globe.

The bad news is that analysts still have to provide forecasts and it is by these estimates that the reporting season for the first six months of calendar 2020 will be judged, especially if companies do feel able to offer some sort of forecast of their own for the second half of the year or 2021, unlikely as this seems right now.

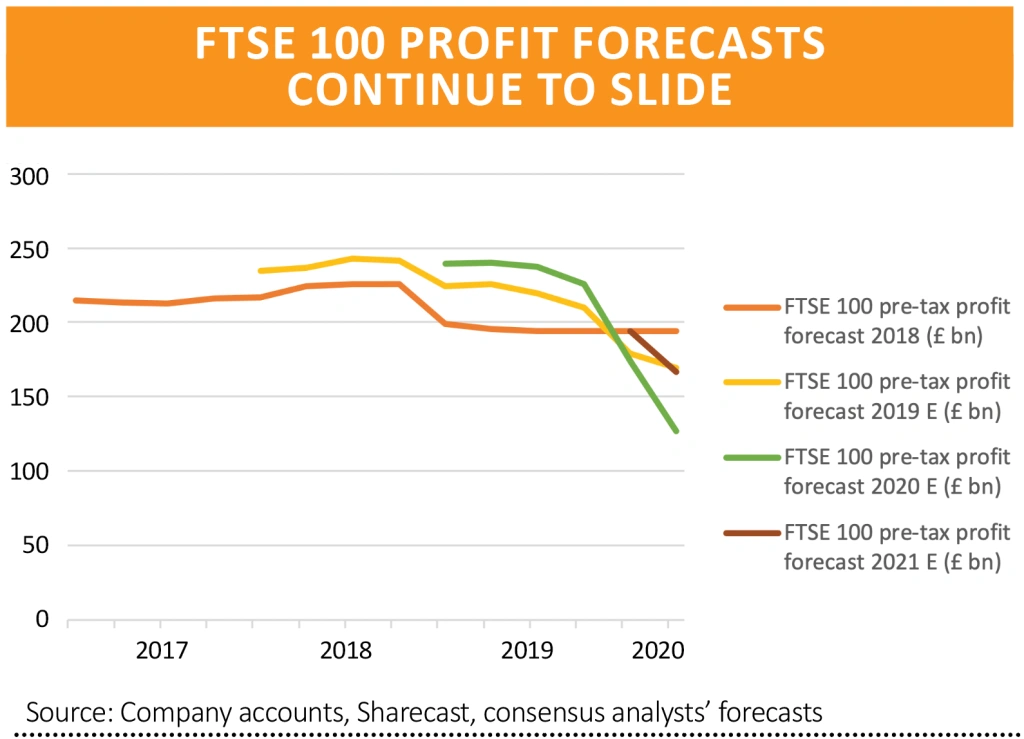

Trend is no friend

Analysts have been busy cutting their estimates for aggregate FTSE 100 profits throughout 2020. Investors will hardly be shocked by this, as at the turn of the year no-one could have forecast the pandemic and the UK stock market was instead preoccupied by the Conservatives’ general election victory in December and what this might mean in terms of policy with regard to the economy and Brexit.

It now looks like the FTSE 100 in aggregate delivered £169 billion in pre-tax profit in 2019, compared to the £240 billion analysts were expecting at the start of that year. Forecasts for 2020 have plunged by 45% to £126 billion since Christmas.

At the moment pre-tax income is seen reaching £166 billion in 2021. That is just less than the members of the FTSE 100 generated between them in 2017, to suggest analysts feel the recovery will be a tepid one, at least initially.

This could be seen as a good thing, as it does not make companies or their shareholders too much of a hostage to fortune relative to lofty expectations.

In the mix

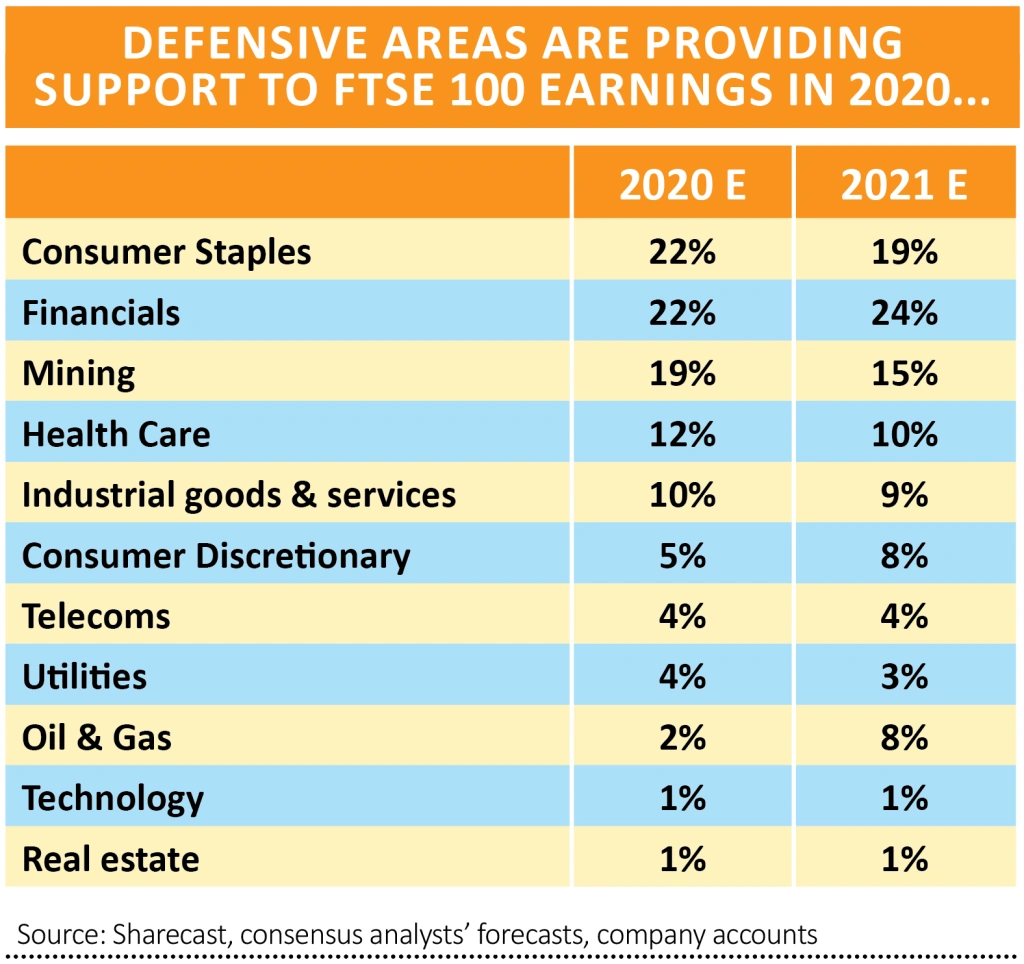

Investors may decide it is impossible to second-guess Covid-19’s impact whether there is a second wave or not, especially as central banks and governments still seem determined to throw everything they can at the economy. But analysis of the profit mix within the FTSE 100 may at least help portfolio-builders develop an awareness of the key sensitivities.

For example, it may be a source of relief to some investors, either on ethical or purely financial grounds, that oil stocks are no longer expected to be big profit contributors to the FTSE 100, at just 2% of the total in 2020. Looking at that, they may not be able to do much more damage either and could be a source of potential upside if oil and gas prices forge a sustained and unexpected recovery.

Instead, consumer staples – food producers, food retailers, alcohol and tobacco stocks – are providing the bedrock to profits in 2020. Note also how health care, consumer staples, telecoms (Vodafone (VOD)) and utilities are expected to generate earnings growth, albeit not enough to offset the collapse at consumer plays, miners, banks and oils. It could be argued that this may give the FTSE 100 some defensive qualities.

However, more than 40% of pre-tax income is still expected to come from financials and miners so it may not pay to overplay that theory, as a sluggish recovery (or a downturn) and interest rates staying lower for longer are not likely to help here. The same concerns apply to 2021, where forecasts of a rebound in overall earnings rest heavily upon oils, financials and consumer plays like retailers and media stocks.

Any investor, and especially one looking for passive exposure through an index tracker, now knows exactly what they are getting with UK stocks: some downside protection but a lot of gearing into any economic upturn, through commodity prices, consumer plays and banks.

It could be argued that is not an especially high-quality earnings mix, not least as those areas are fiendishly difficult to forecast. Investors must now decide whether forecasts of a 3.6% dividend yield in 2020 and 4.3% in 2021 are sufficient compensation for them while they wait to find out what is coming next.

Admittedly, an argument in favour of portfolio diversification is hardly new but in its defence this column will reach for a quote from Ed Murrow, by way of conclusion:

‘The obscure we see eventually. The completely obvious, it seems, takes longer.’

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.