Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy the FAANGs are flying high

The best performing stock in the S&P 500 in 2020 to date may be a gold miner, Newmont, but 10 of the top 20 names are tech stocks of various colours and five more are pharmaceutical or biotech plays.

Two – Netflix and Amazon – are part of the FAANG quintet, along with Facebook, Apple and Google’s parent Alphabet. All five names are up on the year, compared to a 13% drop at the time of writing in the S&P 500.

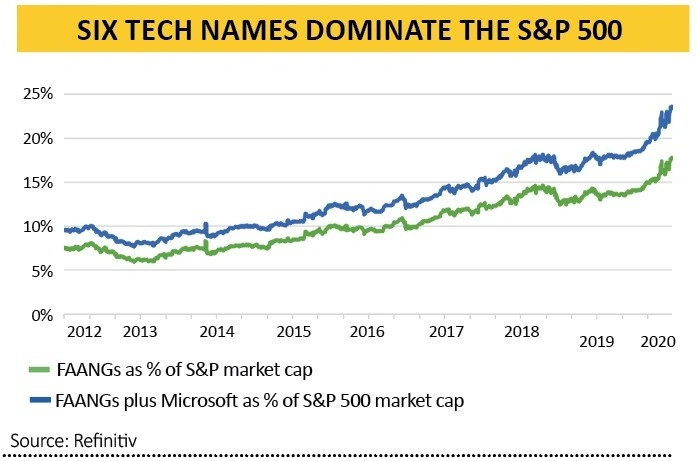

As a result of their stunning long-term performance, these five firms are now worth almost 18% of the S&P 500 on their own (and twice as much as the entire FTSE 100).

A sixth tech name, Microsoft, is the world’s biggest firm by market cap, a fraction ahead of Apple. Throw that into the mix, and this sextet is currently being valued at $4.3trn, or 24.7% of the S&P 500.

Put another way, over the past 12 months, the S&P’s market cap has grown by $187bn. These six stocks have added $1.5trn, which does not say much for the other 494 members of the American benchmark and begs several questions for anyone with exposure to US equities:

– Is such a narrow-looking market as healthy as it seems?

– Do holders of passive, or tracker, products know that their money is so exposed to just six stocks, when what they will really be seeking is diversification?

– Does this help or hinder the active managers whom investors pay to generate outperformance, if six stocks are so dominant?

– Will the FAANG stocks, plus Microsoft, continue to perform so well in both operational and share price terms? Or will margins and valuations revert to the mean over time, permitting stock market or technology new leaders to emerge?

Six of the best

It is easy to see why the FAANGs are still doing so well, including in 2020, even if they are all ultimately very different businesses.

They are essentially digital, flexible, platform businesses that can control costs, maintain service standards and still fulfil customer needs even during these difficult times.

Their value lies in intellectual property, not physical assets (even if how they obtain and use some of the IP, in the form of customer data, remains a bone of contention for some).

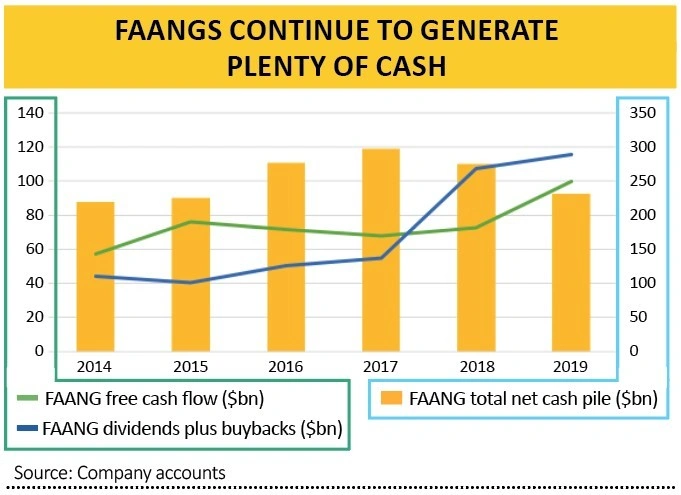

They have strong balance sheets (with Netflix the exception), as evidenced by a combined net cash pile of $212bn, a figure that has barely changed since the end of 2014 despite $290bn in capex and $450bn in dividends and share buybacks.

This is evidence of their powerful profit margins (average 17.7% in 2019) and strong free cash flow, which has come to $485bn in total since 2014 (even though Netflix has contributed only outflows).

Companies generally falter because customers and clients either get fed up with them and seek an alternative or their bounteous margins, cash flow and returns on capital attract competition, which relentlessly chip away at all three. While Netflix probably faces the greatest number of new rivals, the others still look difficult to dislodge.

Price and value

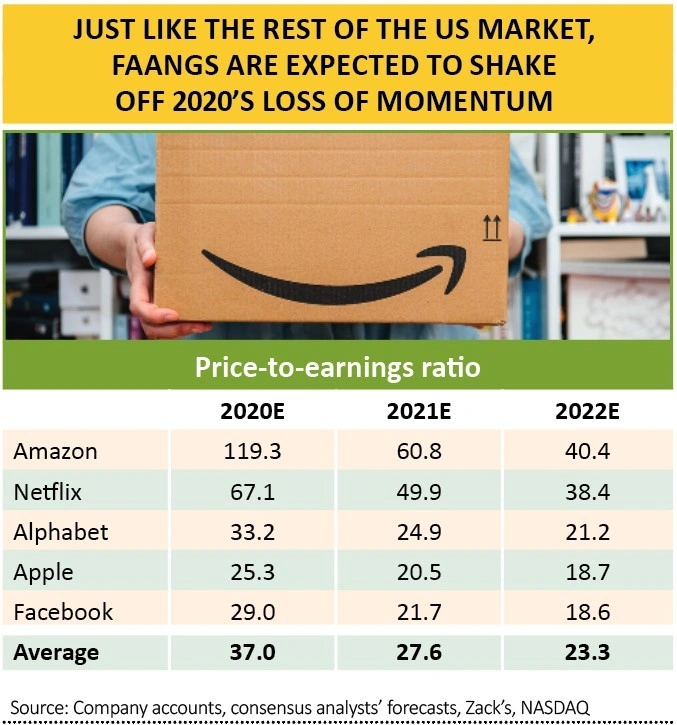

So far so good. But then how much of this is news? Not much, judging by the stellar share price performance and valuations. The FAANGs’ monster market cap means that they trade on 37 times forward earnings for 2020, although forecast rapid earnings growth of 34% for 2021 and 19% for 2022 means that drops to 23 times in two years’ time.

Here is the nub of the issue. If those forecasts prove accurate, the FAANGs could well remain all-conquering. But consider that aggregate net income fell 2% in 2019 and is forecast to drop 4% in 2020, as Amazon piles on the costs and Alphabet and Facebook encounter a squeeze on advertising spending, and those growth estimates may look aggressive. That would leave buybacks and dividends exposed, as they exceeded total free cash flow generated in 2018 and 2019.

That still begs the issue of what could lead to the sort of earnings disappointment that persuades growth-hungry investors to move on, if customers still seem happy to pay for the services on offer (or accept access to their data as payment in kind, in certain cases)?

Regulation is still a possible source of difficulty, with Amazon set to be hauled before Congress to explain how it uses data and Apple, Alphabet and Facebook all still looking over their shoulders from prior disputes with the taxman or anti-trust regulators or privacy campaigners. How politicians react remains as unpredictable as ever.

Perhaps the biggest potential challenge could come from a different source: inflation. Investors warm to growth stocks – and pay high multiples for them – because there is little reliable growth around.

If government and central bank stimulus programmes designed to fight the virus do lead to an unexpected bout of inflation, cyclical growth will be just as easy to find as secular growth, if not easier, and it will come at a fraction of the price. But then many famous names have fallen from favour while waiting for ‘value’ as a style to return to it, have they not?

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.