Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineDiversified Gas & Oil is the real deal for dividends

Newly promoted from AIM to London’s Main Market, Diversified Gas & Oil (DGOC) could provide a beacon of income stability at a time when many listed companies have been cutting their dividends.

A dividend yield of 12% is underpinned by the company’s low-cost model, strong balance sheet and robust cash generation.

Chief executive Rusty Hustson tells Shares he is ‘adamant’ the dividend will not be cut.

On 4 May the company announced a quarterly dividend payment of 3.5c per share, in line with the level from the fourth quarter.

A potential inclusion in the FTSE 250 index later this year is a catalyst for the stock as index funds would be required to buy it.

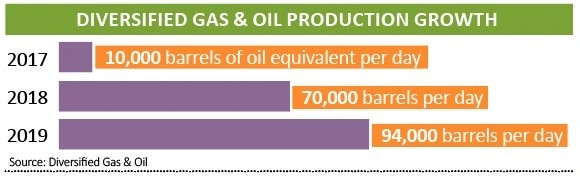

The company’s strategy is to buy conventional assets, often from larger operators which are not set up to run them as efficiently and, in the past at least, which have been chasing the higher volumes associated with unconventional assets.

Diversified Gas & Oil’s wells, most of which are located in the Appalachian region, often have long lives and low rates of decline with minimal maintenance costs. Its output is heavily weighted towards natural gas.

The US Henry Hub natural gas benchmark is currently approaching $2 per thousand cubic feet (mcf), having been pulled lower amid the dive in oil prices. Diversified Gas & Oil has hedged 90% of its 2021 production at $2.60 per mcf and has a unit cost of just $1.16 per mcf – enabling it to generate strong margins.

As oil producers shut in production in response to lower prices and dwindling demand, this reduces the amount of associated natural gas produced alongside this oil and could boost the price for Diversified Gas & Oil’s unhedged output.

The company remains committed to acquisitions and it announced two separate deals in recent weeks, worth a combined $235m, funded in part by an oversubscribed $87m share placing.

Hutson says there is a one to two year window to take advantage of opportunities created by the current dislocation in the market as other operators look to reduce their levels of debt.

As the business builds its production through further M&A it should in theory generate more cash to return to shareholders.

Risks include the company’s borrowings which stand at just over two times earnings, although this is mitigated by strong cash generation, as well as weak sentiment towards the wider oil and gas sector. However, overall we think this looks an attractive income play.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.