Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineDividend delight: the stocks and funds still paying investors a decent income

Income is a big motivating factor for people to invest in the markets. The idea of securing a regular stream of cash which can be used to pay the bills or reinvested to help boost capital returns is an attractive one.

However, this income is not guaranteed and the last two months or so of dividend cuts, suspensions and deferrals have seen billions of pounds worth of payouts from UK stocks taken off the table. This means less cash in the pockets of investors.

There is still hope amid the darkness for income hunters. Not all businesses and asset classes are being affected equally, either by the pandemic or the lockdown measures introduced to contain it. There are still many firms and funds with both the means and intention of continuing to pay a decent dividend.

In this article Shares identifies nine income picks which we think are fairly resilient to the coronavirus crisis, spanning UK and global stocks and funds as well as bonds, property and infrastructure.

RESETTING EXPECTATIONS

On the whole, the level of income on offer from equities is likely to be lower than has been seen in recent years.

In fact with companies building up debt and the possibility of regulator intervention, particularly for those which have been in receipt of state aid, the capacity of some firms to pay dividends at pre-crisis levels may be impaired in the longer term.

The dividend suspensions and cuts introduced by companies as they look to weather the corona-related storm will also feed through to income funds and investment trusts to some degree, including some of our selections in this article.

Most of the time the yields quoted for these products will be historic, and in the majority of cases it would be prudent to assume they will not pay the same level of income for 2020 as they have in previous years.

Janus Henderson’s Jane Shoemake, investment director on the Global Equity Income team, comments: ‘The UK market is currently yielding around 5%, but as all the cuts come through this will prove to be illusionary and the yield could be nearer to 3.5%. However, this still looks attractive when compared to the yield available from bonds and cash and is around the market’s longer term average.’

STOCKS VERSUS BONDS AND CASH

While it might be tempting to turn away from equities after being burned by the unremitting stream of negative news on dividends, with interest rates at record lows the income on offer from cash in the bank or for a lot of bonds is not attractive.

Fidelity’s global chief investment officer Andrew McCaffery comments: ‘Parts of the fixed income markets could see income reduce.

‘As countries borrow heavily to mitigate the impact of the crisis, fiscal deficits balloon and monetary policy remains loose, government bond yields are likely to be even lower and carry higher risk than in the past. This creates an income conundrum for investors that may have to be addressed in other ways.’

These other ways may include turning to infrastructure and certain property assets. McCaffery adds: ‘In the short term, areas such as real estate and infrastructure face challenges around income, tenant viability and counterparty risk. Longer-term, however, high quality real assets should provide both income and elements of diversification away from public markets.’

Even among listed companies, some will see their dividend paying capacity less affected. Pointing to Janus Henderson’s recently published Global Dividend Index, covering 1,200 of the largest global companies, Shoemake says: ‘if we look at the report we estimate 40% of dividends paid globally are in relatively resilient sectors like healthcare, consumer staples and technology; 40% are in highly cyclical areas such as financials and energy and consumer discretionary sectors like retail and travel and leisure which have been badly affected; while the impact for the remaining 20% will be mixed.’

CUTTING DIVIDENDS CAN HELP COMPANIES

Sometimes pausing or cutting dividends is the right thing to do. Preserving cash could help see companies through the crisis and aid the longevity of the business.

The Global Dividend Index report has a best-case scenario which will see a 15% decline in global dividends in 2020 and a worst-case scenario which will see a decline of 35%.

Shoemake sees the likely outcome as being somewhere between those two extremes, noting that in the financial crisis, from peak to trough dividends fell 30% while earnings fell 60%.

The message is clear: you need to pick your investments very carefully and don’t presume historic levels of income will continue into the future.

To help you navigate the space, we now look at different parts of the investment income universe to explain what’s happening and to suggest investments which we believe to be attractive in the current environment. That said, it is important to understand that dividends are not guaranteed payments, even among stocks and funds that seemingly look strong enough to pay.

Why investment trust dividends aren’t bulletproof

The structure of investment trusts means that unlike other types of funds they can put aside up to 15% of the income received in good years in a rainy day pot to help sustain dividends when times are tougher. This trait has helped drive investors towards income-focused investment trusts, some of which have started to trade at a premium to net asset value.

Unfortunately this status has hyped up investment trusts so that some investors now believe they are bulletproof when it comes to paying dividends.

‘Ultimately, in the long term the level of dividends will depend on the underlying income from the market and making estimates of this is an impossible task at the moment,’ says Numis.

‘If underlying companies reduce payouts over the long-term it is going to be increasingly difficult for equity investment trusts to support dividends well in excess of the market, even if they have significant reserves.’

Investment trusts are unlikely to want to run down their reserves to near-zero as it leaves them with no support for future years, so don’t assume that buying a trust with plenty of reserves means they will guarantee historic dividend payouts.

Which areas of the UK market look safe for income investors?

There are areas of the market where companies are generating sufficiently steady cash flows where investors can be confident dividends will continue to be paid.

Healthcare is a prime example, with drug makers AstraZeneca (AZN) and GlaxoSmithKline (GSK) generating billions of dollars of positive cash flow every quarter.

Moreover, both firms are mindful of the need to maintain their dividends, particularly after so many FTSE 100 companies have suspended payouts.

Smaller healthcare stocks such as Bioventix (BVXP:AIM) and medical equipment suppliers ConvaTec (CTEC) and Smith & Nephew (SN.) also generate healthy cash flows and are optimistic about the full year, which bodes well for their ability to keep paying dividends.

A large number of property stocks and real estate investments trusts (REITs) – which are often bought precisely because of their seemingly dependable yields – have also confirmed their dividend plans for this year. However, we must flag that some areas of commercial property look vulnerable longer-term if more people work from home rather than go into an office.

Investors have a choice of exposure to healthcare real estate through firms such as Impact Healthcare (IHR) and Primary Health Properties (PHP), large-format retail real estate through Supermarket Income REIT (SUPR), Tritax Big Box (BBOX) and Warehouse REIT (WHR), or residential property through GCP Student Living (GCP) and Grainger (GRI).

With savers and investors stuck at home poring over their finances, another area of the market paying healthy dividends is firms helping people with their money such as through financial advice or comparison services, with confirmed payouts from Mattioli Woods (MTW:AIM), Moneysupermarket.com (MONY) and Mortgage Advice Bureau (MAB1:AIM) to name a few.

THREE UK STOCKS AND FUNDS TO BUY FOR INCOME

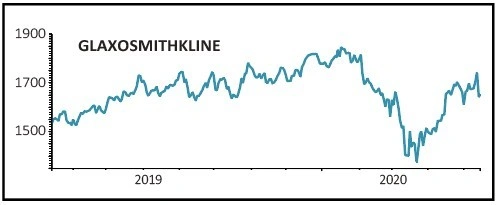

GlaxoSmithKline (GSK) £16.70

Prospective yield: 4.7%

Pharmaceutical giant GlaxoSmithKline has a solid record of progressively increasing its dividend and it also makes quarterly payments.

When it reported first quarter results (29 April) the company kept prior guidance for 2020 earnings per share to decline by between 1% and 4% while maintaining the dividend at 80p.

The company is very active in the fight against coronavirus and aims to develop multiple vaccines using its own technology as well as collaborating with companies across the globe.

A key advantage of GlaxoSmithKline’s technology in the context of the pandemic is that it may reduce the amount of vaccine protein required per dose, allowing more doses to be produced.

Alongside vaccines, the company is exploring therapeutic options and in April announced collaboration with Vir Biotechnology to identify and accelerate new antiviral drug developments.

National Grid (NG.) 910p

Prospective yield: 5.4%

Inflation could become a much tougher challenge for income investors in the future so a measure of dividend inflation-proofing is a major reason to buy shares in this power network operator.

National Grid runs much of the UK’s electricity and gas supply infrastructure, with similarly regulated operations in the US.

It has a long track record of steadily increasing its annual payout to shareholders dating beyond the 2002 merger with Lattice, which formed an electricity and gas transmission national champion.

People need to light and heat their homes whether there is a pandemic or not which means there has been little disruption to the company’s finances, although it did hint at some infrastructure investment delays in an April update.

This makes National Grid forecasts reasonably reliable where the near-term is so opaque for so many others. Forecasts imply dividends of about 50p per share for the year to 31 March 2021, implying a 5.5% income yield, with annual payout growth of about 2.5% out to 2022. There is also around £5.5bn of untapped borrowing capacity to draw on if needed.

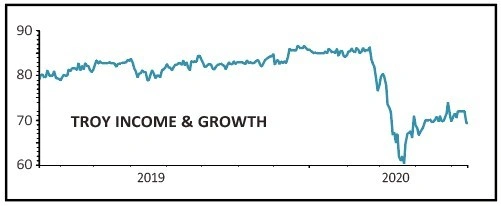

Troy Income & Growth (TIGT) 72p

Historic yield: 3.8%

A shift in the investment trust’s portfolio in 2019, ahead of the coronavirus crisis, was well-timed. The trust sold higher yielding stocks where there were questions marks over the sustainability of dividends and replaced them with firms that had better long-term prospects for dividend growth.

Troy Income & Growth has already indicated that it will maintain the dividend at the current quarterly rate of 0.695p for the current financial year to 30 September 2020 but will rebase it from that point.

Despite this near-term reduction in income, we still think the trust should be a good long-term option for income investors as its new approach should enable it to increase returns to shareholders over time.

Steered by Francis Brooke and Hugo Ure, its top holdings include consumer goods firms Unilever (ULVR) and Reckitt Benckiser (RB.), big pharma stocks GlaxoSmithKline and AstraZeneca as well as utility National Grid.

Going global in the search for income

Readers may be more familiar with UK income stock options but to solely search your own investment backyard is a handicap most of us could do without.

Fund manager Baillie Gifford estimates there are roughly 250 dividend-paying companies in the UK with the scale and liquidity most investors would require, compared to something like 4,500 worldwide.

Going global provides you with the chance to escape from the current risks attached to UK oil companies, banks, high street retailers and other trouble spots.

Less cyclical high-yielding UK sectors such as tobacco and telecoms are where income seekers have traditionally turned yet these are mature sectors and ones that do come with regulatory risk and low long-term growth prospects.

It is not a coincidence that many companies in these supposed low-risk sectors such as BT (BT.A) have failed to deliver profit growth over long periods, and in many cases have had to rebase dividends.

Having a worldwide remit paves the way for income from a far broader range of companies with established or emerging market positions and robust finances.

For example, innovative manufacturing companies with products that genuinely enhance the efficiency of their customers should see their earnings bounce back, such as Taiwan Semiconductor and Bristol-Myers Squibb, the US healthcare firm. Investment firm Blackstone and Pfizer are among the global names you will find with prospective income yields of more than 3.5%.

TWO GLOBAL FUNDS TO BUY FOR INCOME

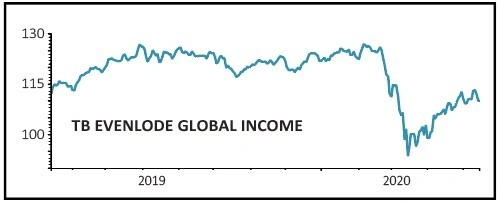

TB Evenlode Global Income Fund (BF1QNC4)

Historic yield: 2.4%

This global income fund was born out of the success of the popular UK-focused TB Evenlode Income Fund. The latter has massively outstripped its Investment Association benchmark over three and five years by buying stakes in largely London-listed companies capable of producing high returns on invested capital long into the future, and grow income to match, including Unilever and Diageo (DGE).

The TB Evenlode Global Income Fund’s strategy is the same, but with a global stocks remit. It focuses on larger companies whose earnings are growing and where strong levels of cash generation should fund a growing stream of dividends.

Its portfolio includes microchip manufacturer Intel. While it only has modest dividend yield of 2.4%, dividends are growing between mid-single and low-double digits each year.

A recent stake purchase in CTS Eventim, a European event ticketing provider, is an example of taking a long view. Talking on the AJ Bell / Shares Money & Markets podcast, Evenlode fund manager Ben Peters says Eventim is challenged right now with major events on hold, but it is in a great position for the future.

DISCLAIMER: Editor Daniel Coatsworth has a personal investment in Evenlode Global Income

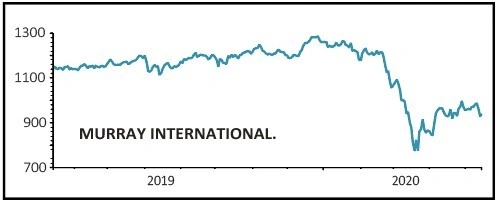

Murray International (MYI) 942p

Historical yield: 5.8%

Managed by seasoned investor Bruce Stout, Murray International aims to generate an above-average dividend yield and long-term income and capital growth from a diversified portfolio of global equities and fixed income securities.

The yield is 5.8% based on what it paid in the last financial year but investors would be wise to expect a slightly lower figure going forward.

Murray has delivered 15 consecutive years of dividend growth and should continue to be a reliable source of income. It has substantial revenue reserves of £76m at last count, equivalent to 1.1 times the £69m total cost of the 2019 dividend.

Last year, a modest 11% of Murray International’s revenue was generated from UK shares, while 63% came from overseas stocks. Stout favours emerging markets over developed markets due to their superior growth prospects and relatively attractive valuations.

Last year, some 26% of revenue arose from Murray’s bond portfolio, enhancing its credentials as an income diversifier. There’s an eclectic mix of equity holdings including the likes of tech leaders Samsung Electronics and Taiwan Semiconductor, consumer product powerhouses PepsiCo and Philip Morris, European industrials Atlas Copco and Bayer, and pharmaceutical firms Novartis and Roche.

Investing in bonds as a source of income

Bonds are an IOU issued by governments and companies which pay a fixed rate of interest, usually twice a year. They are issued with various maturities, from two years all the way out to 30 years. At maturity the debt is repaid and the investor gets their money back, in theory.

Longer-dated bonds have higher yields than shorter-dated bonds to reflect the risk of not getting your money back and the effect of inflation eroding the purchasing power of your invested cash.

However, since the financial crisis of 2008, central banks have engaged in policies which have had the effect of lowering interest rates right across the maturity spectrum, from short-dated two-year to 30-year rates.

For example at the time of writing, two-year UK government bonds yield minus 0.04%, 10-years yield (positive) 0.2% and 30-years yield 0.6%, a very narrow spread in a historical context. Also, note that all those yields are far below the current inflation rate of 1.5%.

UK government bonds are considered very safe as they are backed by the ability to raise taxes as well as print money. However, you can get a greater return through cash accounts at the moment.

Investors can earn even higher rates of interest by investing in emerging market government bonds, which pay around 4.5% a year, but these are more risky.

Looking further afield, corporate bonds are riskier than government bonds and pay a higher rate of interest related to the riskiness of the underlying company and its ability to service interest payments.

Because of the specialised skills needed to assess bonds, for most investors the best course of action is to get exposure through actively-managed funds or exchange-traded products that track major bond indices.

TWO BOND FUNDS TO BUY FOR INCOME

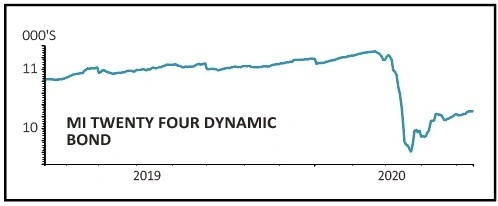

MI TwentyFour Dynamic Bond Fund (B57GX40)

Historic yield: 4.1%

TwentyFour is an independent fixed-income asset management firm, founded in 2008 by a group of leading specialists. TwentyFour Dynamic Bond Fund is highly diversified and has the flexibility and expertise to take advantage of prevailing market conditions as they change through time, rather than being pigeonholed into one part of the market.

The fund has an excellent track record, delivering a better return than its benchmark and peers over the last three and five years with average annual returns of 1.3% and 2.3% respectively.

The managers were very active in April this year as sentiment improved and the bond markets opened up with a raft of new issues indicating healthy investor appetite. The team reduced their allocation to government bonds by 7% to 20%. This allowed the fund to take advantage of some attractive valuations in the corporate credit space.

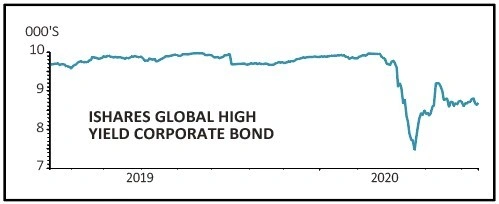

iShares Global High Yield Corporate Bond (GHYS) £86.75

Historic yield: 5.4%

This highly diversified fund, managed by exchange-traded fund provider BlackRock, aims to track a global developed markets liquid high yield index.

High yield corporate bonds are debts issued by companies with lower credit ratings than investment grade corporate and government bonds. The yields are higher to reflect the greater risk.

Investors in this product get exposure to the debts of over 1,300 companies, across all sectors of the global economy. Spreading risk in this way helps to cushion the impact on the portfolio if one or more of the companies goes bust.

High yield bonds are more sensitive than investment grade or government bonds to economic expansions and downturns, leading to greater potential for capital gains and losses.

Other types of investments that provide income

Alternative asset classes like infrastructure and property have always been a way for investors to access stable income streams.

While businesses cut dividends as their revenue dries up and certain bond yields plummet alongside interest rates, alternative assets are becoming one of the few places where income remains relatively intact.

Infrastructure can be a good source of income. In the current environment, investors might want to look for funds that invest in essential, government-backed assets like schools, hospitals, critical gasworks and energy transmission, rather than demand-led infrastructure like rail, roads and airports.

For property, the areas of the sector seemingly most secure in terms of income are social housing and healthcare real estate assets that remain vital in the current crisis with rental income largely intact unlike areas such as retail or offices.

Arguably the best way to invest in infrastructure is through investment trusts because they are not subject to the whims of daily dealing like open-ended funds. This is important because a lot of infrastructure and property trusts will most often hold real assets that are hard to buy and sell quickly.

These assets do carry risks which are different than if you were investing in shares of companies, and these risks could potentially impact the dividend yield.

In terms of infrastructure, the biggest risk is that the government breaks or renegotiates contracts or nationalises assets. A more likely risk is that the operators of assets encounter financial difficulties. For property, tenants being able to pay rent is still a risk, while the social housing sector in general has been criticised by its regulator for various issues including health and safety.

TWO ALTERNATIVE ASSET INVESTMENTS TO BUY FOR INCOME

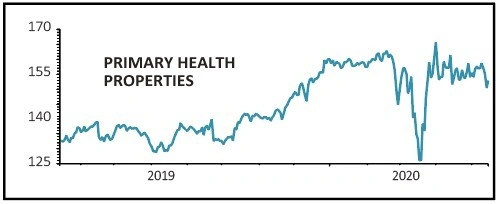

Primary Health Properties (PHP) 155.2p

Historic yield: 3.4%

The group is invested in nearly 500 primary healthcare facilities in the UK, let on long-term leases. It recently agreed to buy 20 purpose-built medical centres, located throughout England and Wales, for £47m with the company also conditionally contracted to buy a further two centres for approximately £7m.

These assets are rented to GP practices, the NHS and pharmacies with 91% of rental income being Government-backed.

Given the need to reduce the pressure on the NHS these types of facilities are likely to be a priority for governments of whatever stripe in the UK.

Across the existing holdings, 98% of rents for the second quarter have been collected which speaks to the resilience of the rental income and underpins the company’s commitment to a progressive dividend policy. This makes a yield of nearly 3.5% attractive even if the shares trade at a 54% premium to net asset value.

International Public Partnerships (INPP) 161.6p

Prospective yield: 4.6%

Core infrastructure investment trusts look to be trading on attractive yields given their long-term, government-backed income streams and high degree of inflation linkage.

One product that should offer reliable income in this space is International Public Partnerships (INPP), which looks better placed than some other trusts in the sector as most of the assets in its portfolio are essential and not demand-led, and so the income from them should in theory be more secure.

The portfolio is also well-diversified and the FTSE 250 trust recently reiterated its 2020 dividend target of 7.36p, putting it on a 4.6% prospective yield.

Investing in over 100 projects across the UK, Europe, North America and Australia, its portfolio includes public private partnerships for schools, hospitals and even police stations, as well as energy transmission cables and megaprojects like the Thames Tideway Tunnel.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.